Question

2) Use the semi-annually compounded yield curve below, price the following securities: a) Plot the zero/spot/yield curve. b) 5-year zero coupon bond c) 7-year coupon

2) Use the semi-annually compounded yield curve below, price the following securities:

a) Plot the zero/spot/yield curve. b) 5-year zero coupon bond c) 7-year coupon bond paying 15% semiannually d) 4-year coupon bond paying 7% quarterly e) 3 14-year coupon bond paying 9% semiannually

3) Use the same yield curve in 2). Consider two bonds, both with 7 years to maturity, but with different coupon rates. Let the two coupon rates be 15% and 3%.

a) Compute the prices and the yields to maturity of these coupon bonds. b) How do the yields to maturity compare to each other? If they are different, why are they different? Would the difference in yields imply that one is a better buy than the other?

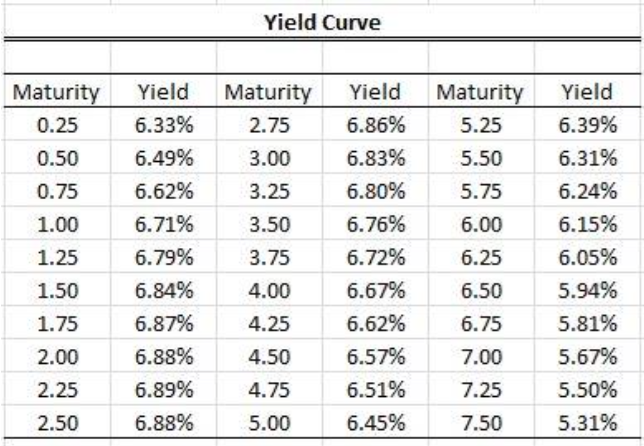

Yield Curve MaturityYieldMaturity Yield Maturity Yield 0.25 6.33% 275 6.86% 525 6.39% 0.50 6.49% 3.00 6.83% 5.50 6.31% 0.75 6.62% 3.25 6.80% 5.75 6.24% 1.00 6.71% 3.50 6.76% 6.00 6.15% 1.25 6.79% 3.75 6.72% 6.25 6.05% 1.50 6.84% 4.00 6.67% 6.50 5.94% 1.75 6.87% 4.25 6.62% 6.75 5.81% 2.00 6.88% 4.50 6.57% 7.00 5.67% 225 6.89% 475 6.51% 725 5.50% 2.50 6.88% 5.00 6.45% 7.50 5.31%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Routledge Handbook Of State Owned Enterprises

Authors: Luc Bernier, Massimo Florio, Philippe Bance

1st Edition

1138487694, 978-1138487697