Answered step by step

Verified Expert Solution

Question

1 Approved Answer

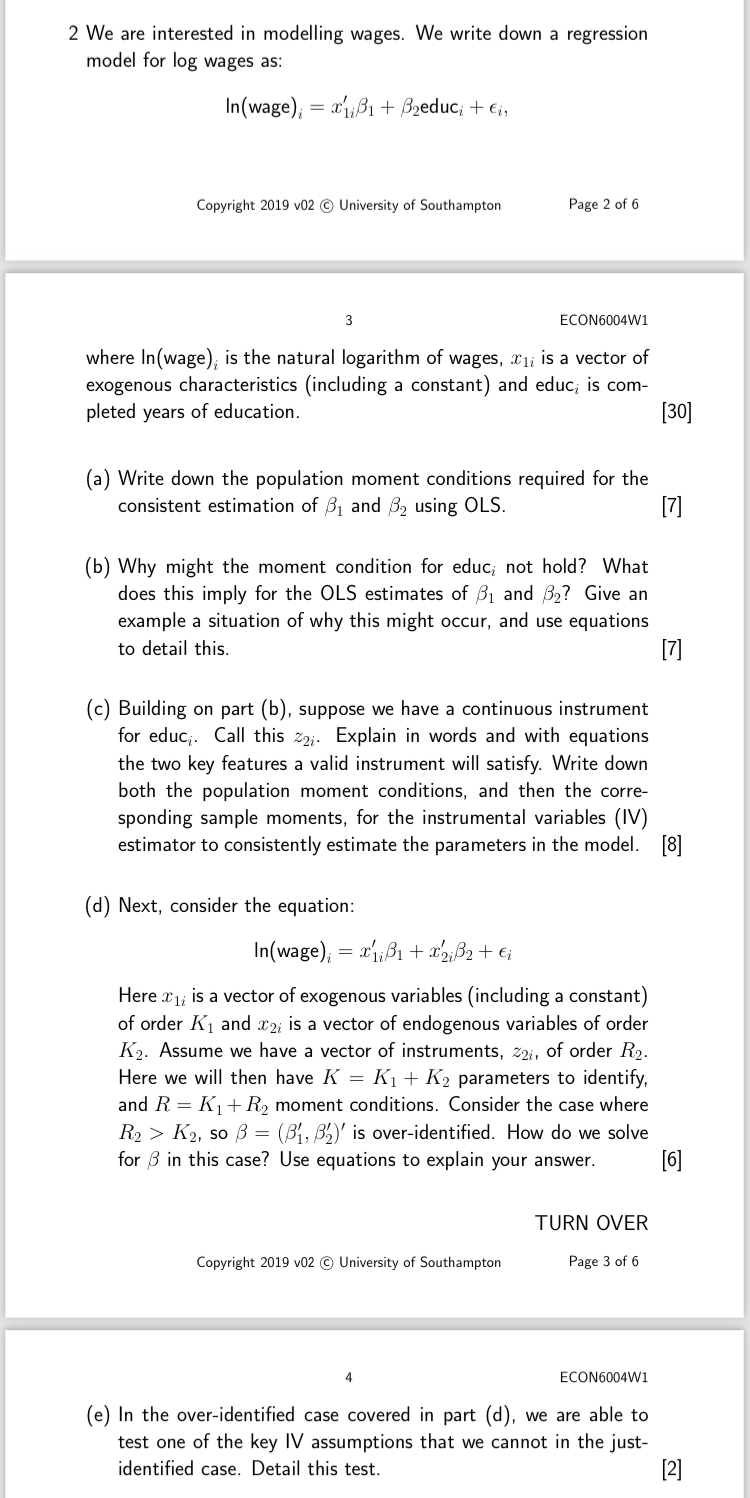

2 We are interested in modelling wages. We write down a regression model for log wages as: In (wage), = xB1 + Beduci +

2 We are interested in modelling wages. We write down a regression model for log wages as: In (wage), = xB1 + Beduci + , Copyright 2019 v02 University of Southampton ECON6004W1 where In (wage), is the natural logarithm of wages, is a vector of exogenous characteristics (including a constant) and educ; is com- pleted years of education. [30] Page 2 of 6 (a) Write down the population moment conditions required for the consistent estimation of 3 and 32 using OLS. [7] (b) Why might the moment condition for educ, not hold? What does this imply for the OLS estimates of 3 and 3? Give an example a situation of why this might occur, and use equations to detail this. (d) Next, consider the equation: (c) Building on part (b), suppose we have a continuous instrument for educ. Call this 22. Explain in words and with equations the two key features a valid instrument will satisfy. Write down both the population moment conditions, and then the corre- sponding sample moments, for the instrumental variables (IV) estimator to consistently estimate the parameters in the model. [8] Copyright 2019 v02 University of Southampton In(wage), = x + x2i + i Here is a vector of exogenous variables (including a constant) of order K and 2 is a vector of endogenous variables of order K. Assume we have a vector of instruments, 221, of order R2. Here we will then have K = K + K parameters to identify, and R = K + R moment conditions. Consider the case where R > K, so B = (B, B)' is over-identified. How do we solve for 3 in this case? Use equations to explain your answer. [6] [7] TURN OVER Page 3 of 6 ECON6004W1 (e) In the over-identified case covered in part (d), we are able to test one of the key IV assumptions that we cannot in the just- identified case. Detail this test. [2]

Step by Step Solution

★★★★★

3.40 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Introduction to the Mathematics of Financial Derivatives

Authors: Ali Hirsa, Salih N. Neftci

3rd edition

012384682X, 978-0123846822