Answered step by step

Verified Expert Solution

Question

1 Approved Answer

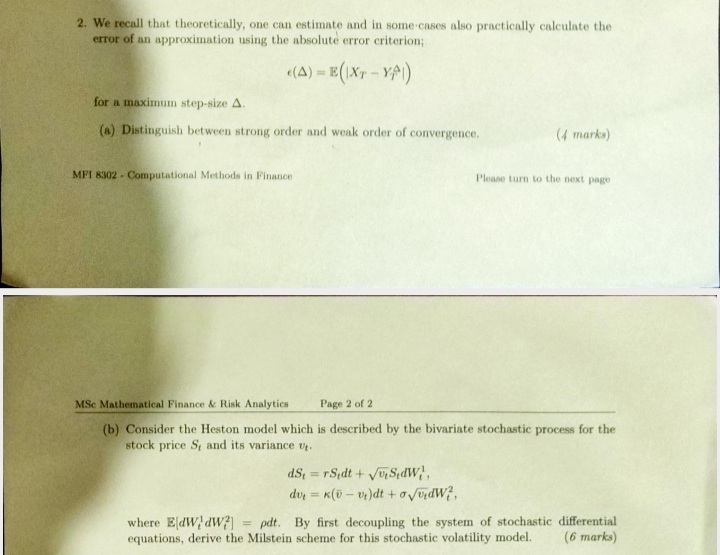

2. We recall that theoretically, one can estimate and in some'cases also practically calculate the error of an approximation using the absolute error criterion; ()=E(XTYT)

2. We recall that theoretically, one can estimate and in some'cases also practically calculate the error of an approximation using the absolute error criterion; ()=E(XTYT) for a maximum step-size . (a) Distinguish between strong order and weak order of convergence. (4 marks) MFI 8302. Computational Methods in Finance Please turn to the next page MSc Mathematical Finance \& Risk Analytics Page 2 of 2 (b) Consider the Heston model which is described by the bivariate stochastic process for the stock price St and its variance vt. dSt=rStdt+vtStdWt1,dvt=(vvt)dt+vtdWt2, where E[dWt1dWt2]=dt. By first decoupling the system of stochastic differential equations, derive the Milstein scheme for this stochastic volatility model. (6 marks)

2. We recall that theoretically, one can estimate and in some'cases also practically calculate the error of an approximation using the absolute error criterion; ()=E(XTYT) for a maximum step-size . (a) Distinguish between strong order and weak order of convergence. (4 marks) MFI 8302. Computational Methods in Finance Please turn to the next page MSc Mathematical Finance \& Risk Analytics Page 2 of 2 (b) Consider the Heston model which is described by the bivariate stochastic process for the stock price St and its variance vt. dSt=rStdt+vtStdWt1,dvt=(vvt)dt+vtdWt2, where E[dWt1dWt2]=dt. By first decoupling the system of stochastic differential equations, derive the Milstein scheme for this stochastic volatility model. (6 marks) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Developments In Entrepreneurial Finance And Technology

Authors: David B. Audretsch, Maksim Belitski, Nada Rejeb, Rosa Caiazza

1st Edition

1800884338,1800884346