Answered step by step

Verified Expert Solution

Question

1 Approved Answer

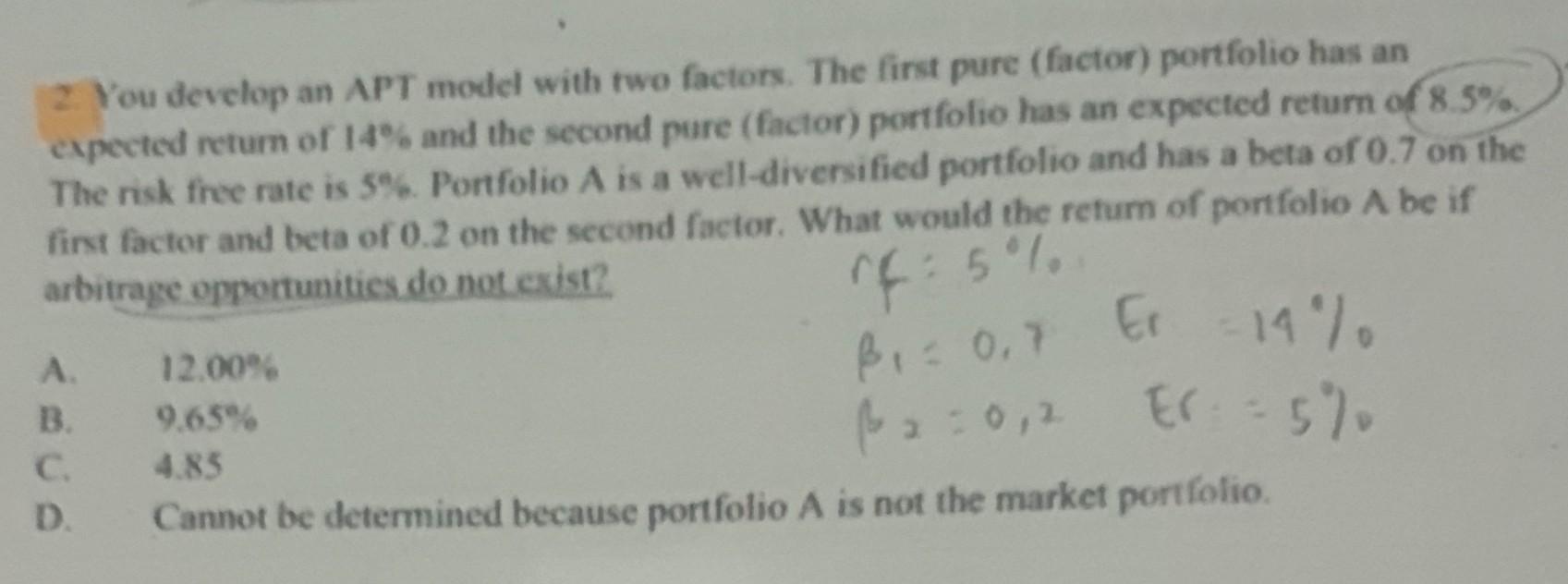

2. You develop an APT model with two factors. The first pure (factor) portfolio has an expected retum of 14% and the second pure (factor)

2. You develop an APT model with two factors. The first pure (factor) portfolio has an expected retum of 14% and the second pure (factor) portfolio has an expected return of 8.5% The risk free rate is 5%. Portfolio A is a well-diversified portfolio and has a beta of 0.7 on the first factor and beta of 0.2 on the second factor. What would the retum of portfolio A be if arbitrage opportunities do not exist? A. 12.00% B. 9.65% C. 4.85 rf=51=0,7Er=14)0(2=0,2Er=5)0 D. Cannot be determined because portfolio A is not the market portfolio

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Grow The Pie How Great Companies Deliver Both Purpose And Profit

Authors: Alex Edmans

1st Edition

1108494854,1108849482