Answered step by step

Verified Expert Solution

Question

1 Approved Answer

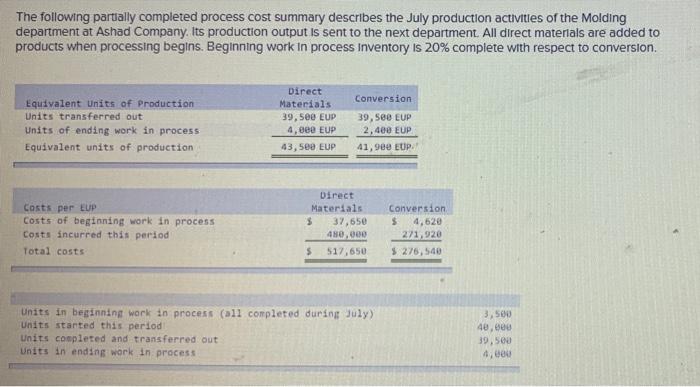

20 The following parually completed process cost summary describes the July production activities of the Molding department at Ashad Company. Its production output is sent

20

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting For Undergraduates

Authors: James Wallace, Scott Hobson, Theodore Christensen

2nd Edition

1618533096, 9781618533098