Answered step by step

Verified Expert Solution

Question

1 Approved Answer

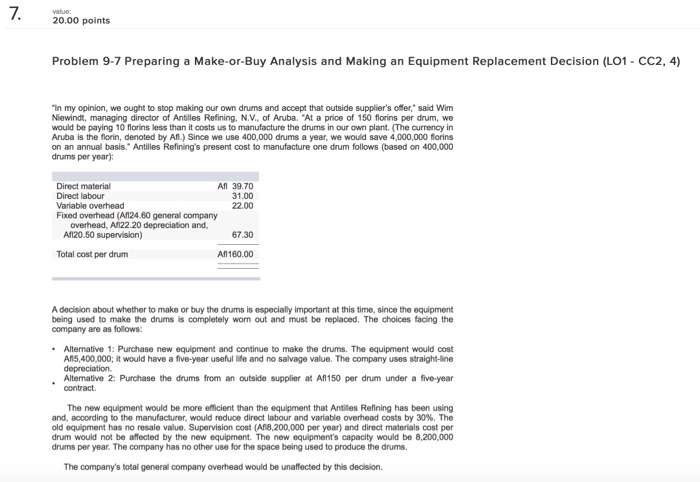

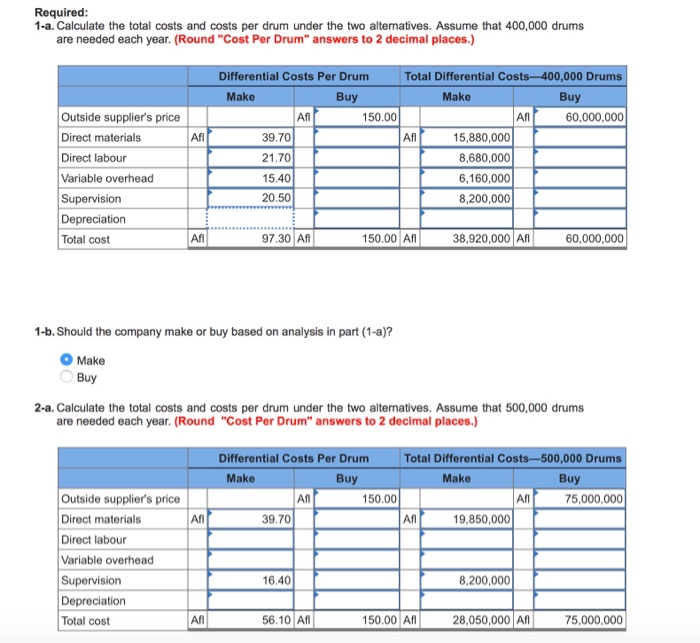

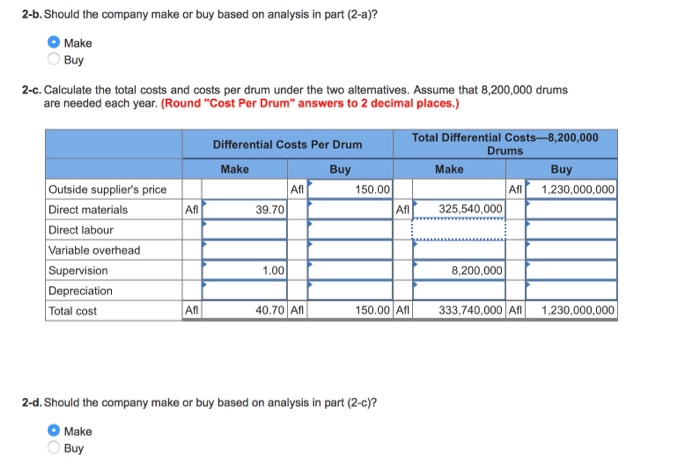

20.00 points Problem 9.7 Preparing a Make-or-Buy Analysis and Making an Equipment Replacement Decision (LOI . CC2.4) In my opinion, we ought to stop making

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Wiley CIA Essentials Of Internal Auditing Exam Review 2022 Part 1

Authors: S. Rao Vallabhaneni

1st Edition

1119846285, 978-1119846284