Answered step by step

Verified Expert Solution

Question

1 Approved Answer

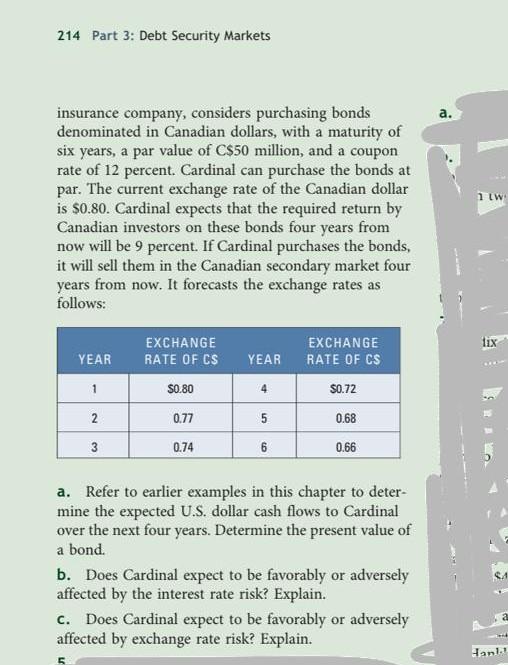

214 Part 3: Debt Security Markets insurance company, considers purchasing bonds denominated in Canadian dollars, with a maturity of six years, a par value of

214 Part 3: Debt Security Markets insurance company, considers purchasing bonds denominated in Canadian dollars, with a maturity of six years, a par value of C$50 million, and a coupon rate of 12 percent. Cardinal can purchase the bonds at par. The current exchange rate of the Canadian dollar is $0.80. Cardinal expects that the required return by Canadian investors on these bonds four years from now will be 9 percent. If Cardinal purchases the bonds, it will sell them in the Canadian secondary market four years from now. It forecasts the exchange rates as follows: EXCHANGE EXCHANGE RATE OF CS YEAR YEAR RATE OF CS 1 $0.80 4 $0.72 2 0.77 5 0.68 3 0.74 6 0.66 a. Refer to earlier examples in this chapter to deter- mine the expected U.S. dollar cash flows to Cardinal over the next four years. Determine the present value of a bond. b. Does Cardinal expect to be favorably or adversely affected by the interest rate risk? Explain. c. Does Cardinal expect to be favorably or adversely affected by exchange rate risk? Explain. 1 tw fix www S Hanl

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Housing Finance

Authors: Peter King

2nd Edition

0415432952, 978-0415432955