Answered step by step

Verified Expert Solution

Question

1 Approved Answer

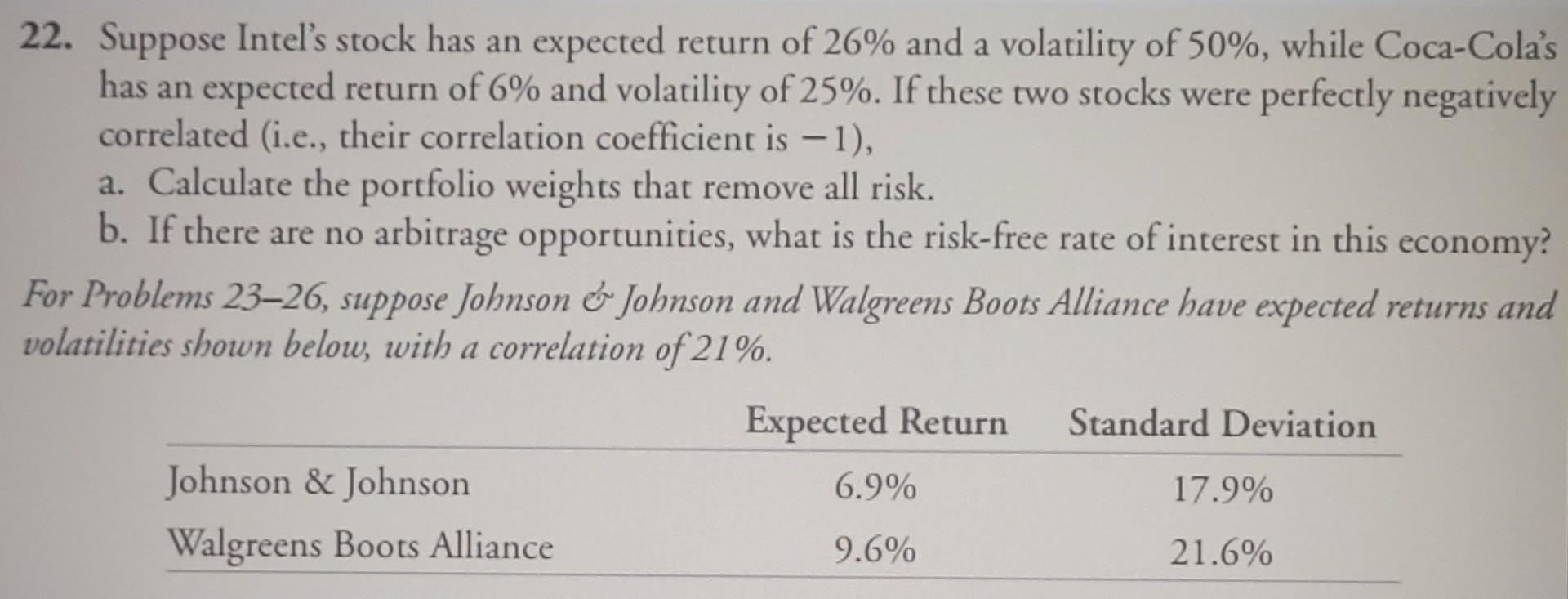

22. Suppose Intel's stock has an expected return of 26% and a volatility of 50%, while Coca-Cola's has an expected return of 6% and volatility

22. Suppose Intel's stock has an expected return of 26% and a volatility of 50%, while Coca-Cola's has an expected return of 6% and volatility of 25%. If these two stocks were perfectly negatively correlated (i.e., their correlation coefficient is -1), a. Calculate the portfolio weights that remove all risk. b. If there are no arbitrage opportunities, what is the risk-free rate of interest in this economy? For Problems 23-26, suppose Johnson & Johnson and Walgreens Boots Alliance have expected returns and volatilities shown below, with a correlation of 21%. Expected Return Standard Deviation Johnson & Johnson 6.9% 17.9% Walgreens Boots Alliance 9.6% 21.6%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Supernatural Provision Living In Financial Freedom

Authors: Joan Hunter, Sid Roth

1st Edition

1641238232, 978-1641238236