Answered step by step

Verified Expert Solution

Question

1 Approved Answer

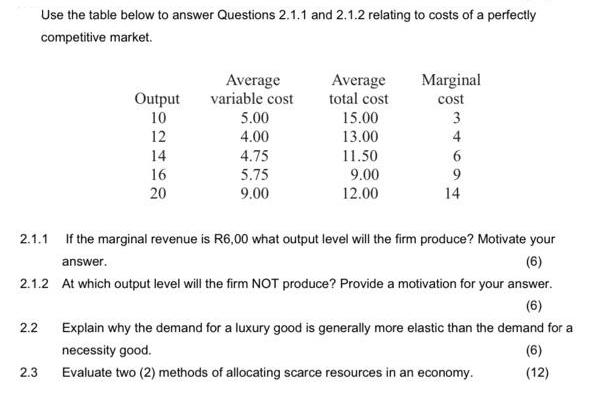

2.2 Use the table below to answer Questions 2.1.1 and 2.1.2 relating to costs of a perfectly competitive market. 2.3 Output 10 12 14

2.2 Use the table below to answer Questions 2.1.1 and 2.1.2 relating to costs of a perfectly competitive market. 2.3 Output 10 12 14 16 20 Average variable cost 5.00 4.00 4.75 5.75 9.00 Average total cost 15.00 13.00 11.50 9.00 12.00 Marginal cost 3 4 6 9 2.1.1 If the marginal revenue is R6,00 what output level will the firm produce? Motivate your answer. (6) 2.1.2 At which output level will the firm NOT produce? Provide a motivation for your answer. (6) 14 Explain why the demand for a luxury good is generally more elastic than the demand for a necessity good. Evaluate two (2) methods of allocating scarce resources in an economy. (6) (12)

Step by Step Solution

★★★★★

3.50 Rating (150 Votes )

There are 3 Steps involved in it

Step: 1

211 The firm will produce at an output level where marginal cost equals marginal revenue In this cas...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516