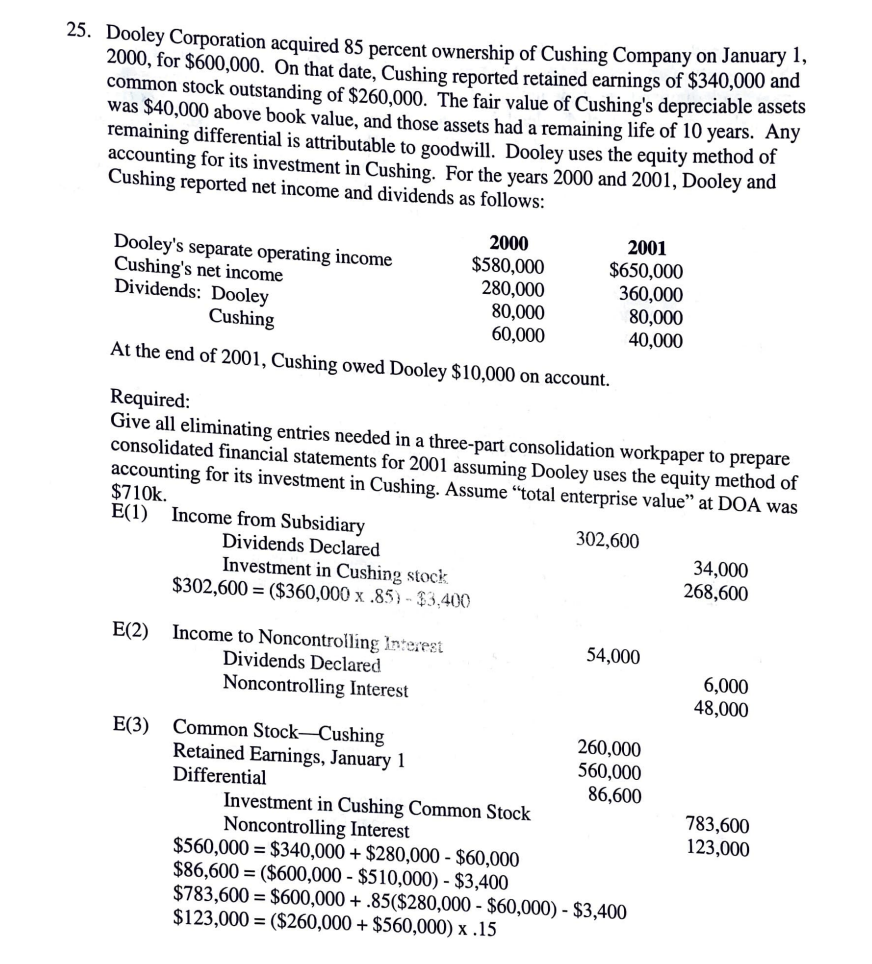

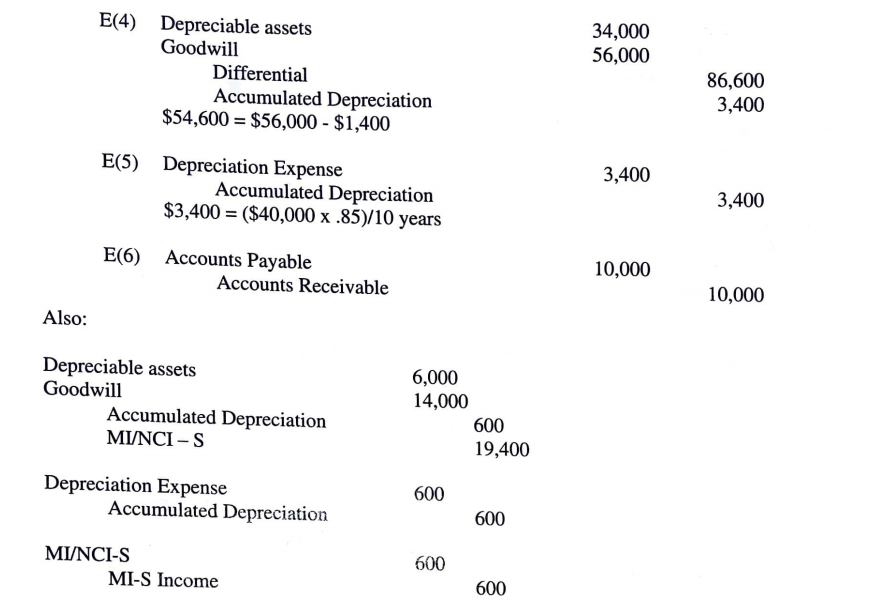

25. Dooley Corporation acquired 85 percent ownership of Cushing Company on January 1, 2000, for $600,000. On that date, Cushing reported retained earnings of $340,000 and common stock outstanding of $260,000. The fair value of Cushing's depreciable assets was $40,000 above book value, and those assets had a remaining life of 10 years. Any remaining differential is attributable to goodwill. Dooley uses the equity method of accounting for its investment in Cushing. For the years 2000 and 2001, Dooley and Cushing reported net income and dividends as follows: Dooley's separate operating income Cushing's net income Dividends: Dooley Cushing 2000 $580,000 280,000 80,000 60,000 2001 $650,000 360,000 80,000 40,000 At the end of 2001, Cushing owed Dooley $10,000 on account. Required: Give all eliminating entries needed in a three-part consolidation workpaper to prepare consolidated financial statements for 2001 assuming Dooley uses the equity method of accounting for its investment in Cushing. Assume total enterprise value at DOA was $710k. E(1) Income from Subsidiary 302,600 Dividends Declared 34,000 Investment in Cushing stock 268,600 $302,600 = ($360,000 x .85- $3,400 E(2) Income to Noncontrolling Interest Dividends Declared Noncontrolling Interest 54,000 6,000 48,000 E(3) Common Stock-Cushing 260,000 Retained Earnings, January 1 560,000 Differential 86,600 Investment in Cushing Common Stock Noncontrolling Interest $560,000 = $340,000+ $280,000 - $60,000 $86,600 = ($600,000 - $510,000) - $3,400 $783,600 = $600,000+.85($280,000 - $60,000) - $3,400 $123,000 = ($260,000+ $560,000) x.15 783,600 123,000 34,000 56,000 E(4) Depreciable assets Goodwill Differential Accumulated Depreciation $54,600 = $56,000 - $1,400 86,600 3,400 3,400 E(5) Depreciation Expense Accumulated Depreciation $3,400 = ($40,000 x .85)/10 years 3,400 E(6) Accounts Payable Accounts Receivable 10,000 10,000 Also: Depreciable assets Goodwill Accumulated Depreciation MI/NCI -S 6,000 14,000 600 19,400 Depreciation Expense Accumulated Depreciation 600 600 MI/NCI-S MI-S Income 600 600 25. Dooley Corporation acquired 85 percent ownership of Cushing Company on January 1, 2000, for $600,000. On that date, Cushing reported retained earnings of $340,000 and common stock outstanding of $260,000. The fair value of Cushing's depreciable assets was $40,000 above book value, and those assets had a remaining life of 10 years. Any remaining differential is attributable to goodwill. Dooley uses the equity method of accounting for its investment in Cushing. For the years 2000 and 2001, Dooley and Cushing reported net income and dividends as follows: Dooley's separate operating income Cushing's net income Dividends: Dooley Cushing 2000 $580,000 280,000 80,000 60,000 2001 $650,000 360,000 80,000 40,000 At the end of 2001, Cushing owed Dooley $10,000 on account. Required: Give all eliminating entries needed in a three-part consolidation workpaper to prepare consolidated financial statements for 2001 assuming Dooley uses the equity method of accounting for its investment in Cushing. Assume total enterprise value at DOA was $710k. E(1) Income from Subsidiary 302,600 Dividends Declared 34,000 Investment in Cushing stock 268,600 $302,600 = ($360,000 x .85- $3,400 E(2) Income to Noncontrolling Interest Dividends Declared Noncontrolling Interest 54,000 6,000 48,000 E(3) Common Stock-Cushing 260,000 Retained Earnings, January 1 560,000 Differential 86,600 Investment in Cushing Common Stock Noncontrolling Interest $560,000 = $340,000+ $280,000 - $60,000 $86,600 = ($600,000 - $510,000) - $3,400 $783,600 = $600,000+.85($280,000 - $60,000) - $3,400 $123,000 = ($260,000+ $560,000) x.15 783,600 123,000 34,000 56,000 E(4) Depreciable assets Goodwill Differential Accumulated Depreciation $54,600 = $56,000 - $1,400 86,600 3,400 3,400 E(5) Depreciation Expense Accumulated Depreciation $3,400 = ($40,000 x .85)/10 years 3,400 E(6) Accounts Payable Accounts Receivable 10,000 10,000 Also: Depreciable assets Goodwill Accumulated Depreciation MI/NCI -S 6,000 14,000 600 19,400 Depreciation Expense Accumulated Depreciation 600 600 MI/NCI-S MI-S Income 600 600