Answered step by step

Verified Expert Solution

Question

1 Approved Answer

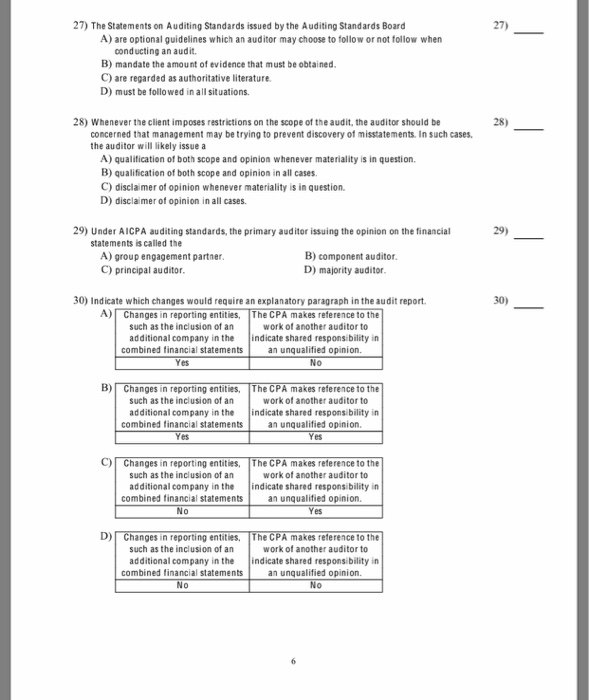

27) The Statements on Auditing Standards issued by the Auditing Standards Board A) are optional guidelines which an auditor may choose to follow or not

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Japanese Management Accounting A World Class Approach To Profit Management

Authors: Michiharu Sakurai, Yasuhiro Monden

1st Edition

091529950X, 978-0915299508