Answered step by step

Verified Expert Solution

Question

1 Approved Answer

3. (10 marks) Consider a 3-year interest-rate swap with a counterparty initially rated B and a notional of $100 million. The following table shows the

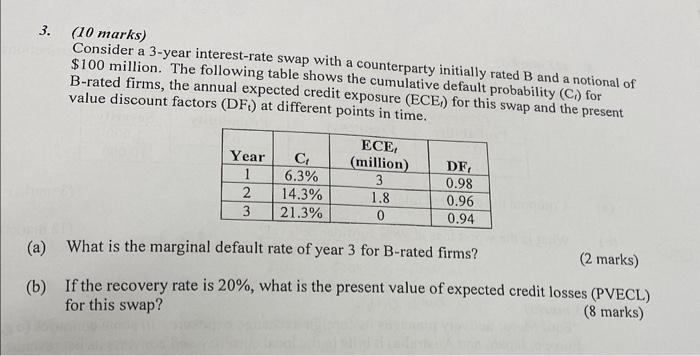

3. (10 marks) Consider a 3-year interest-rate swap with a counterparty initially rated B and a notional of $100 million. The following table shows the cumulative default probability (C1) for B-rated firms, the annual expected credit exposure (ECEt) for this swap and the present value discount factors (DFt) at different points in time. (a) What is the marginal default rate of year 3 for B-rated firms? ( 2 marks) (b) If the recovery rate is 20%, what is the present value of expected credit losses (PVECL) for this swap? (8 marks)

3. (10 marks) Consider a 3-year interest-rate swap with a counterparty initially rated B and a notional of $100 million. The following table shows the cumulative default probability (C1) for B-rated firms, the annual expected credit exposure (ECEt) for this swap and the present value discount factors (DFt) at different points in time. (a) What is the marginal default rate of year 3 for B-rated firms? ( 2 marks) (b) If the recovery rate is 20%, what is the present value of expected credit losses (PVECL) for this swap? (8 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

World Investment Report 2021 Investing In Sustainable Recovery

Authors: United Nations Publications

1st Edition

9211130174,9210054636