Answered step by step

Verified Expert Solution

Question

1 Approved Answer

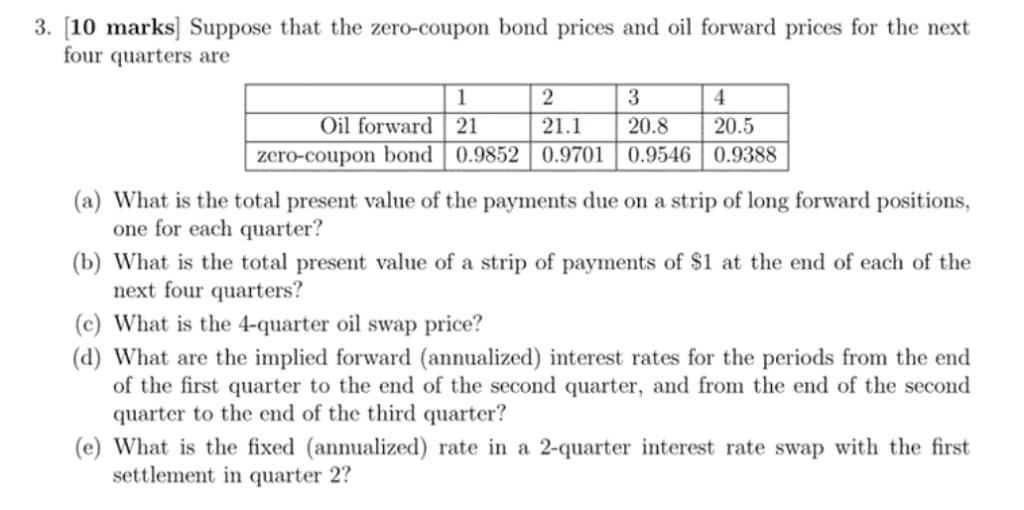

3. [10 marks] Suppose that the zero-coupon bond prices and oil forward prices for the next four quarters are 1 2 3 4 Oil

3. [10 marks] Suppose that the zero-coupon bond prices and oil forward prices for the next four quarters are 1 2 3 4 Oil forward 21 21.1 20.8 20.5 zero-coupon bond 0.9852 0.9701 0.9546 0.9388 (a) What is the total present value of the payments due on a strip of long forward positions, one for each quarter? (b) What is the total present value of a strip of payments of $1 at the end of each of the next four quarters? (c) What is the 4-quarter oil swap price? (d) What are the implied forward (annualized) interest rates for the periods from the end of the first quarter to the end of the second quarter, and from the end of the second quarter to the end of the third quarter? (e) What is the fixed (annualized) rate in a 2-quarter interest rate swap with the first settlement in quarter 2?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

a To calculate the total present value of the payments due on a strip of long forward positions one for each quarter we need to sum up the present val...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Applied Regression Analysis And Other Multivariable Methods

Authors: David G. Kleinbaum, Lawrence L. Kupper, Azhar Nizam, Eli S. Rosenberg

5th Edition

1285051084, 978-1285963754, 128596375X, 978-1285051086