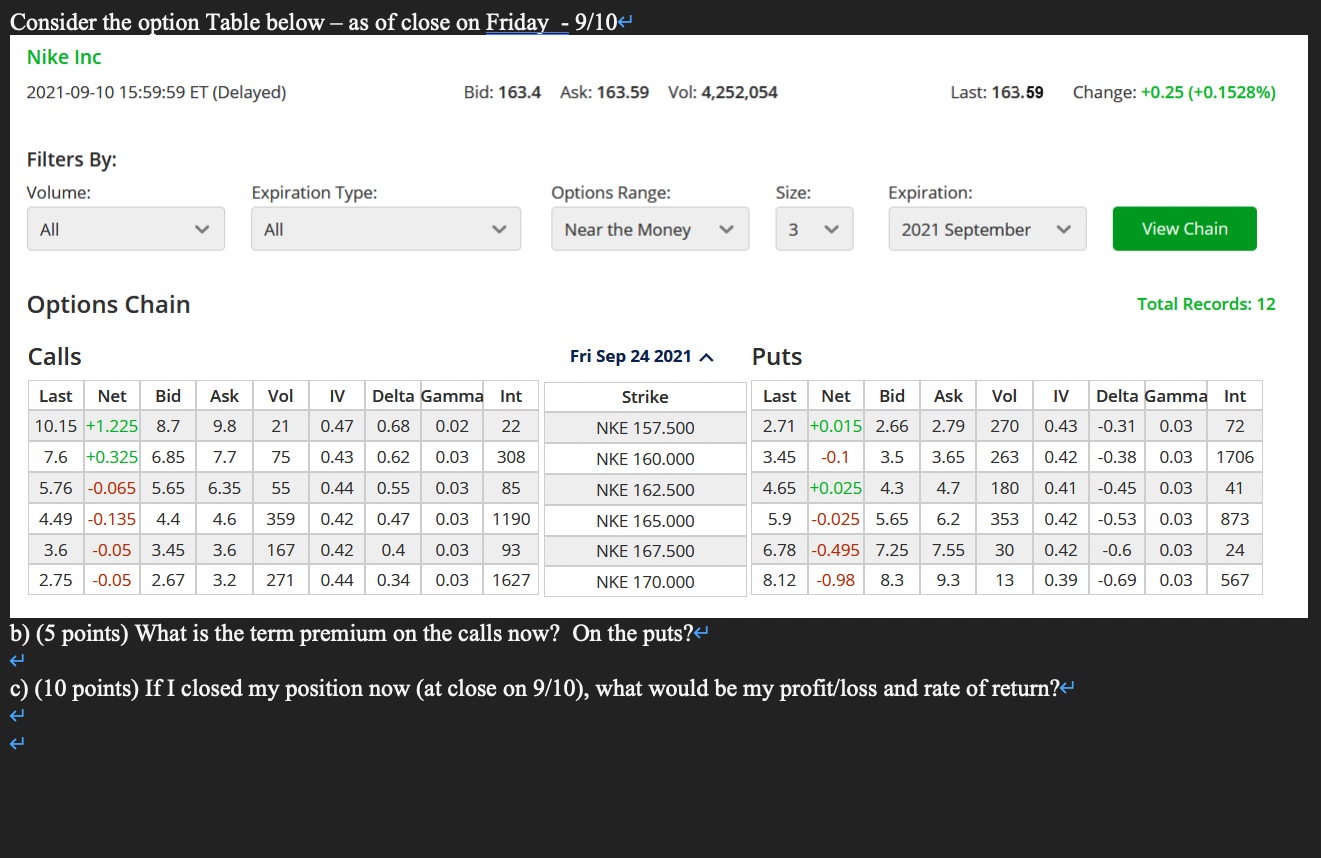

3) (55 points) On 9/8 I played a long straddle on NKE by buying 10 calls and 10 puts each with a strike price of $160 when the spot price was $160.81 (see graph below). + Market Summary > Nike Inc NYSE: NKE 163.59 USD +0.39 (0.24%) past 5 days Closed: Sep 10, 7:56 PM EDT - Disclaimer After hours 163.40 -0.19 (0.12%) 1 day 5 days 1 month 6 months YTD 1 year 5 years Max 166 160.81 USD Wed, Sep 8 12:30 PM 164 162 160 Sep 7 Sep 8 Sep 9 Sep 10 a) (5 points) What is the term premium on the calls? On the puts?- Consider the option Table below as of close on Friday - 9/104 Nike Inc 2021-09-10 15:59:59 ET (Delayed) Bid: 163.4 Ask: 163.59 Vol: 4,252,054 Last: 163.59 Change: +0.25 +0.1528%) Filters By: Volume: Expiration Type: Options Range: Size: Expiration: All All Near the Money 3 V 2021 September View Chain Options Chain Total Records: 12 Calls Fri Sep 24 2021 A Puts Last Net Bid Ask Vol IV Delta Gamma Int Strike Last Net Bid Ask Vol IV Delta Gamma Int 10.15 +1.225 8.7 9.8 21 0.47 0.68 0.02 22 NKE 157.500 2.71 +0.015 2.66 2.79 270 0.43 -0.31 0.03 72 7.6 +0.325 6.85 7.7 75 0.43 0.62 0.03 308 NKE 160.000 3.45 -0.1 3.5 3.65 263 0.42 -0.38 0.03 1706 5.76 -0.065 5.65 6.35 55 0.44 0.55 0.03 85 NKE 162.500 4.65 +0.025 4.3 4.7 180 0.41 -0.45 0.03 41 4.49 -0.135 4.4 4.6 359 0.42 0.47 0.03 1190 NKE 165.000 5.9 -0.025 5.65 6.2 353 0.42 -0.53 0.03 873 3.6 -0.05 3.45 3.6 167 0.42 0.4 0.03 93 NKE 167.500 6.78 -0.495 7.25 7.55 30 0.42 -0.6 0.03 24 2.75 -0.05 2.67 3.2 271 0.44 0.34 0.03 1627 NKE 170.000 8.12 -0.98 8.3 9.3 13 0.39 -0.69 0.03 567 b) (5 points) What is the term premium on the calls now? On the puts?- c) (10 points) If I closed my position now (at close on 9/10), what would be my profit/loss and rate of return? In the space below, draw the profit function(s) of my long straddle on NKE that I opened up on 9/8. Add the profit functions of the player who played the corresponding short straddle. We now play pretend. Suppose we consider two spots (prices) at expiration. The first, label as point A where the options expire with NKE = $155 and the second, label as point B, where the options expire at $175. Note that there is 2 point A's and 2 point B's. e 15 points for correct and completely labeled graph d) (10 points) So you are trying to teach a friend the strategy behind playing either a long straddle or a short straddle. You tell your friend that time is your friend on one of the straddles and time is not your friend for the other straddle. Your friend says I don't understand. Explain to your friend so that they do. * e) (10 points) You also mention to your friend that one of the straddle bets is a high volatility bet and the other straddle bet is a low volatility bet. Explain in detail including in your answer what would be the best case scenario at expiration for the long straddle and what would be the best case scenario for the short straddle (at expiration). 3) (55 points) On 9/8 I played a long straddle on NKE by buying 10 calls and 10 puts each with a strike price of $160 when the spot price was $160.81 (see graph below). + Market Summary > Nike Inc NYSE: NKE 163.59 USD +0.39 (0.24%) past 5 days Closed: Sep 10, 7:56 PM EDT - Disclaimer After hours 163.40 -0.19 (0.12%) 1 day 5 days 1 month 6 months YTD 1 year 5 years Max 166 160.81 USD Wed, Sep 8 12:30 PM 164 162 160 Sep 7 Sep 8 Sep 9 Sep 10 a) (5 points) What is the term premium on the calls? On the puts?- Consider the option Table below as of close on Friday - 9/104 Nike Inc 2021-09-10 15:59:59 ET (Delayed) Bid: 163.4 Ask: 163.59 Vol: 4,252,054 Last: 163.59 Change: +0.25 +0.1528%) Filters By: Volume: Expiration Type: Options Range: Size: Expiration: All All Near the Money 3 V 2021 September View Chain Options Chain Total Records: 12 Calls Fri Sep 24 2021 A Puts Last Net Bid Ask Vol IV Delta Gamma Int Strike Last Net Bid Ask Vol IV Delta Gamma Int 10.15 +1.225 8.7 9.8 21 0.47 0.68 0.02 22 NKE 157.500 2.71 +0.015 2.66 2.79 270 0.43 -0.31 0.03 72 7.6 +0.325 6.85 7.7 75 0.43 0.62 0.03 308 NKE 160.000 3.45 -0.1 3.5 3.65 263 0.42 -0.38 0.03 1706 5.76 -0.065 5.65 6.35 55 0.44 0.55 0.03 85 NKE 162.500 4.65 +0.025 4.3 4.7 180 0.41 -0.45 0.03 41 4.49 -0.135 4.4 4.6 359 0.42 0.47 0.03 1190 NKE 165.000 5.9 -0.025 5.65 6.2 353 0.42 -0.53 0.03 873 3.6 -0.05 3.45 3.6 167 0.42 0.4 0.03 93 NKE 167.500 6.78 -0.495 7.25 7.55 30 0.42 -0.6 0.03 24 2.75 -0.05 2.67 3.2 271 0.44 0.34 0.03 1627 NKE 170.000 8.12 -0.98 8.3 9.3 13 0.39 -0.69 0.03 567 b) (5 points) What is the term premium on the calls now? On the puts?- c) (10 points) If I closed my position now (at close on 9/10), what would be my profit/loss and rate of return? In the space below, draw the profit function(s) of my long straddle on NKE that I opened up on 9/8. Add the profit functions of the player who played the corresponding short straddle. We now play pretend. Suppose we consider two spots (prices) at expiration. The first, label as point A where the options expire with NKE = $155 and the second, label as point B, where the options expire at $175. Note that there is 2 point A's and 2 point B's. e 15 points for correct and completely labeled graph d) (10 points) So you are trying to teach a friend the strategy behind playing either a long straddle or a short straddle. You tell your friend that time is your friend on one of the straddles and time is not your friend for the other straddle. Your friend says I don't understand. Explain to your friend so that they do. * e) (10 points) You also mention to your friend that one of the straddle bets is a high volatility bet and the other straddle bet is a low volatility bet. Explain in detail including in your answer what would be the best case scenario at expiration for the long straddle and what would be the best case scenario for the short straddle (at expiration)