Answered step by step

Verified Expert Solution

Question

1 Approved Answer

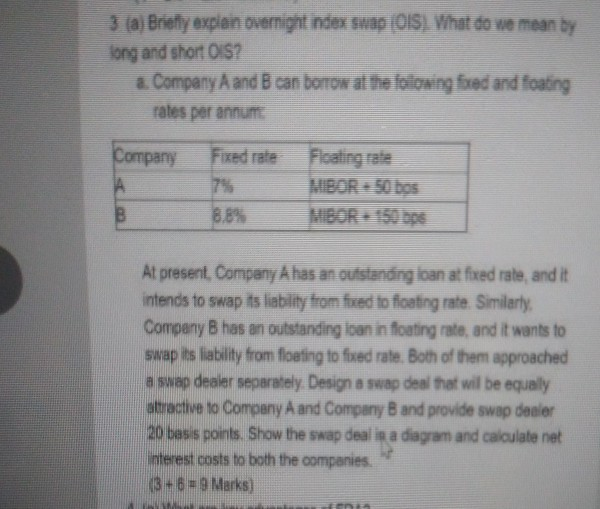

3 (a) Briefly explain overnight ndex swap (OIS) What do we mean by long and short OIS? a. Company A and B can borrow at

3 (a) Briefly explain overnight ndex swap (OIS) What do we mean by long and short OIS? a. Company A and B can borrow at the following fixed and foating rates per annum Fixed rate Company Floating rate WIBOR = 50 bos MBOR - 150 bps At present, Company A has an outstanng loan at fixed rate, and it intends to swap its liability from fired to floating rate. Similarly, Company B has an outstanding loan in foating rate, and it wants to swap its liability from floating to fixed rate. Both of the approached a swap dealer separately. Design a swap deal that will be equally attractive to Company A and Company B and provide swap dealer 20 basis points. Show the swap deal in a diagram and calculate net interest costs to both the companies. (8 + 8 = 9 Narks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Financial Accounting Lawrence S C Good Condition ISBN 08512

Authors: S.C. Lawrence

1st Edition

9780851215099