Answered step by step

Verified Expert Solution

Question

1 Approved Answer

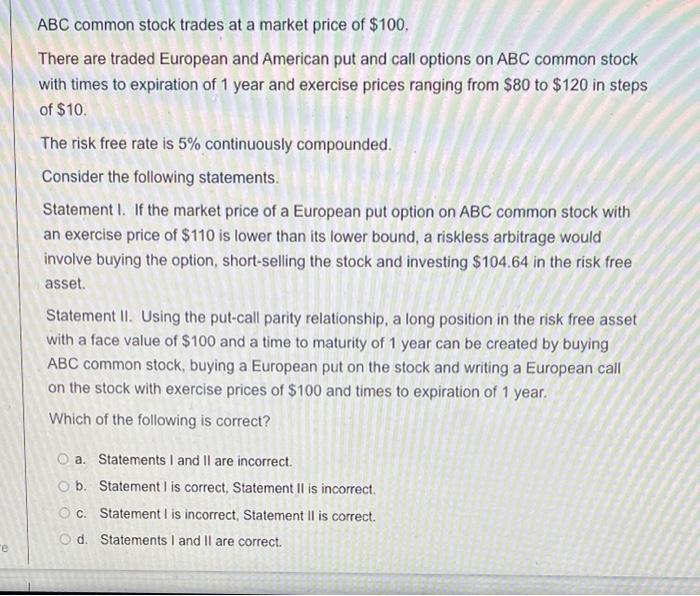

3. ABC common stock trades at a market price of $100, There are traded European and American put and call options on ABC common stock

3.

ABC common stock trades at a market price of $100, There are traded European and American put and call options on ABC common stock with times to expiration of 1 year and exercise prices ranging from $80 to $120 in steps of $10. The risk free rate is 5% continuously compounded. Consider the following statements. Statement I. If the market price of a European put option on ABC common stock with an exercise price of $110 is lower than its lower bound, a riskless arbitrage would involve buying the option, short-selling the stock and investing $104,64 in the risk free asset. Statement II. Using the put-call parity relationship, a long position in the risk free asset with a face value of $100 and a time to maturity of 1 year can be created by buying ABC common stock, buying a European put on the stock and writing a European call on the stock with exercise prices of $100 and times to expiration of 1 year. Which of the following is correct? a. Statements I and II are incorrect. b. Statement is correct, Statement II is incorrect c. Statement is incorrect, Statement II is correct. Od. Statements I and II are correct. e Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Future Of Pricing How Airline Ticket Pricing Has Inspired A Revolution

Authors: E. Boyd

1st Edition

0230600190,0230606903