Answered step by step

Verified Expert Solution

Question

1 Approved Answer

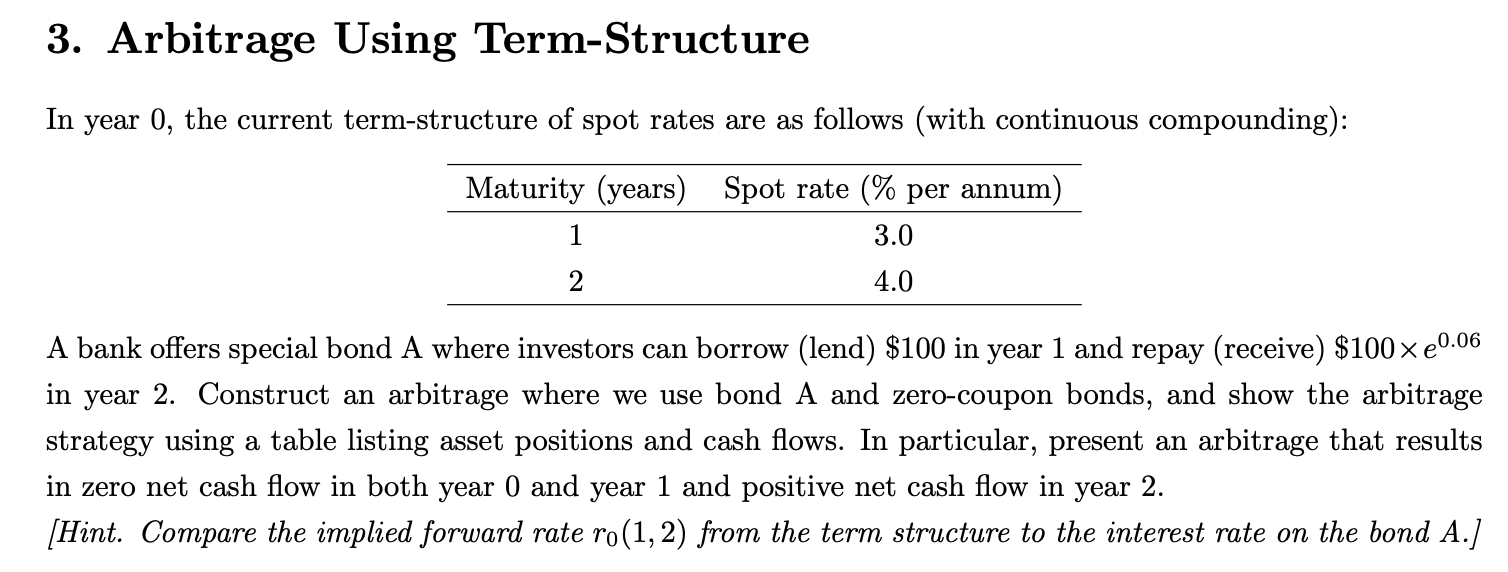

3. Arbitrage Using Term-Structure In year 0, the current term-structure of spot rates are as follows (with continuous compounding): Maturity (years) Spot rate (%

3. Arbitrage Using Term-Structure In year 0, the current term-structure of spot rates are as follows (with continuous compounding): Maturity (years) Spot rate (% per annum) 1 3.0 4.0 A bank offers special bond A where investors can borrow (lend) $100 in year 1 and repay (receive) $100 e0.06 in year 2. Construct an arbitrage where we use bond A and zero-coupon bonds, and show the arbitrage strategy using a table listing asset positions and cash flows. In particular, present an arbitrage that results in zero net cash flow in both year 0 and year 1 and positive net cash flow in year 2. [Hint. Compare the implied forward rate ro(1,2) from the term structure to the interest rate on the bond A.]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurial Finance

Authors: J . chris leach, Ronald w. melicher

4th edition

538478152, 978-0538478151