Answered step by step

Verified Expert Solution

Question

1 Approved Answer

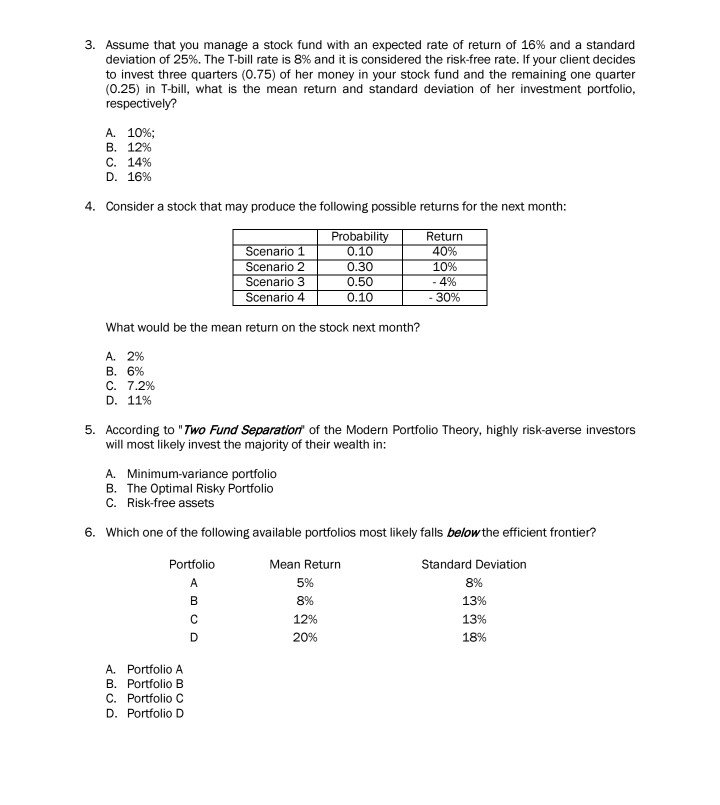

3. Assume that you manage a stock fund with an expected rate of return of 16% and a standard deviation of 25%. The T-bill rate

3. Assume that you manage a stock fund with an expected rate of return of 16% and a standard deviation of 25%. The T-bill rate is 8% and it is considered the risk-free rate. If your client decides to invest three quarters (0.75) of her money in your stock fund and the remaining one quarter (0.25) in T-bill, what is the mean return and standard deviation of her investment portfolio respectively? A. 10%; B. 1296 C. 14% D. 16% 4. Consider a stock that may produce the following possible returns for the next month: Probability Return rio Scenario 2 Scenario 3 0.30 0.50 0.10 10% 4% 30% What would be the mean return on the stock next month? A. 2% B. 6% C. 7.2% D. 11% 5. According to "Two Fund Separation of the Modern Portfolio Theory, highly risk-averse investors will most likely invest the majority of their wealth in: A. Minimum-variance portfolio B. The Optimal Risky Portfolio C. Risk-free assets 6. Which one of the following available portfolios most likely falls below the efficient frontier? Portfolio Mean Return 5% 8% 12% 20%, Standard Deviation 8% 13% 13% 18% A. Portfolio A B. Portfolio B C. Portfolio C D. Portfolio D

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Stock Markets And Corporate Finance A Primer

Authors: Michael Dempsey

1st Edition

1800611471,1800611498