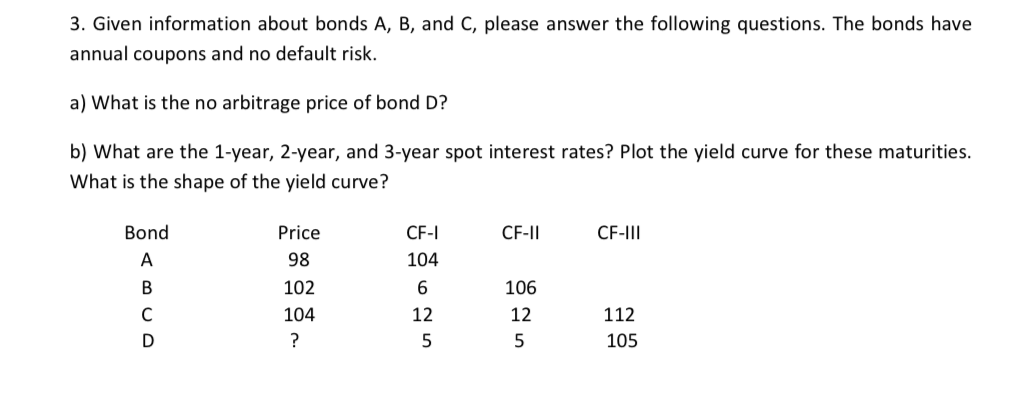

Question: 3. Given information about bonds A, B, and C, please answer the following questions. The bonds have annual coupons and no default risk. a) What

3. Given information about bonds A, B, and C, please answer the following questions. The bonds have annual coupons and no default risk. a) What is the no arbitrage price of bond D ? b) What are the 1-year, 2-year, and 3-year spot interest rates? Plot the yield curve for these maturities. What is the shape of the yield curve

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock