Answered step by step

Verified Expert Solution

Question

1 Approved Answer

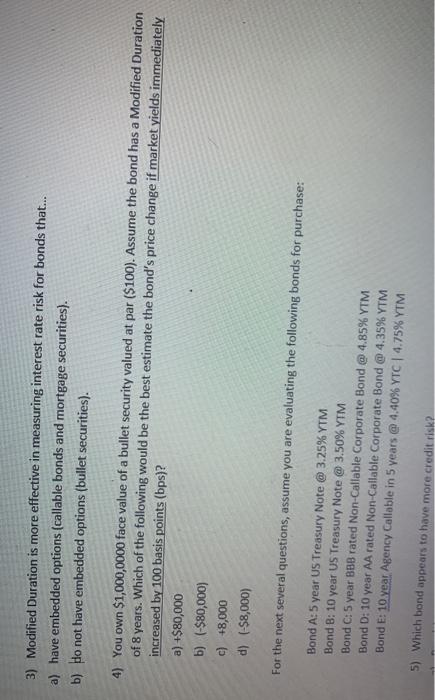

3) Modified Duration is more effective in measuring interest rate risk for bonds that... a) have embedded options (callable bonds and mortgage securities). b) Ho

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Elementary Statistics

Authors: Mario F. Triola

3rd Canadian Edition

032122597X, 978-0321225979