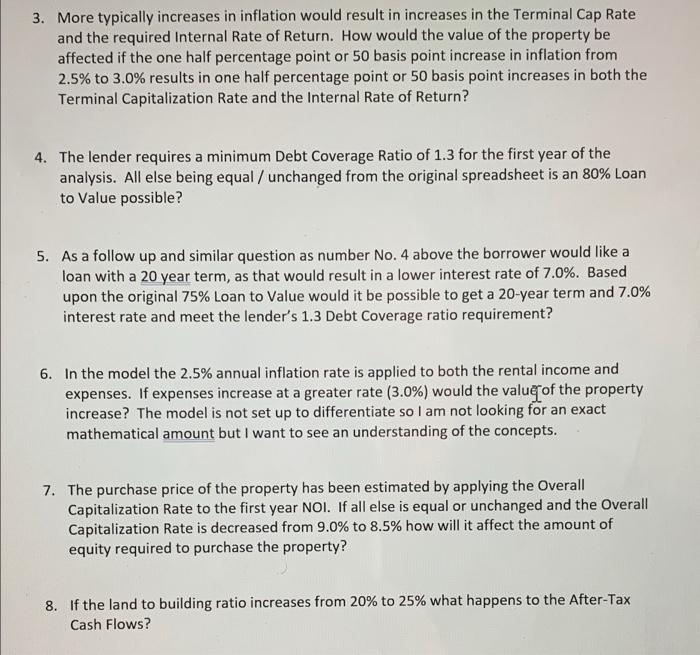

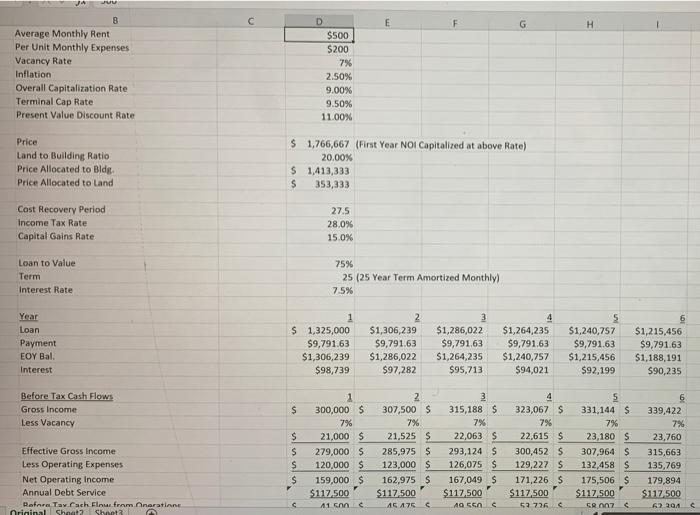

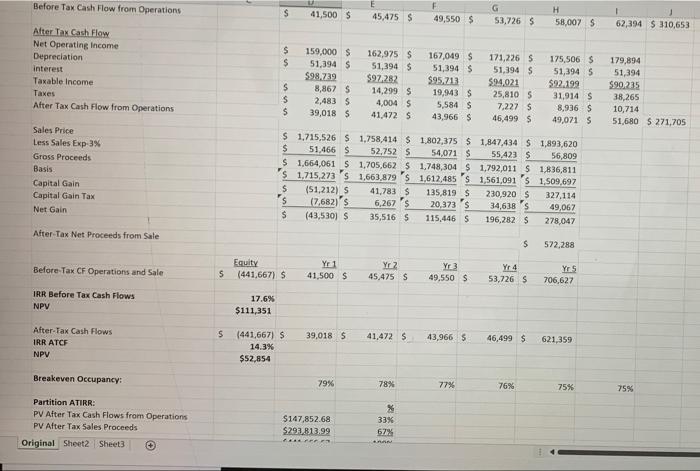

3. More typically increases in inflation would result in increases in the Terminal Cap Rate and the required Internal Rate of Return. How would the value of the property be affected if the one half percentage point or 50 basis point increase in inflation from 2.5% to 3.0% results in one half percentage point or 50 basis point increases in both the Terminal Capitalization Rate and the Internal Rate of Return? 4. The lender requires a minimum Debt Coverage Ratio of 1.3 for the first year of the analysis. All else being equal / unchanged from the original spreadsheet is an 80% Loan to Value possible? 5. As a follow up and similar question as number No. 4 above the borrower would like a loan with a 20 year term, as that would result in a lower interest rate of 7.0%. Based upon the original 75% Loan to Value would it be possible to get a 20-year term and 7.0% interest rate and meet the lender's 1.3 Debt Coverage ratio requirement? 6. In the model the 2.5% annual inflation rate is applied to both the rental income and expenses. If expenses increase at a greater rate (3.0%) would the value of the property increase? The model is not set up to differentiate so I am not looking for an exact mathematical amount but I want to see an understanding of the concepts. 7. The purchase price of the property has been estimated by applying the Overall Capitalization Rate to the first year NOI. If all else is equal or unchanged and the Overall Capitalization Rate is decreased from 9.0% to 8.5% how will it affect the amount of equity required to purchase the property? 8. If the land to building ratio increases from 20% to 25% what happens to the After-Tax Cash Flows? JA JUU E F H 8 Average Monthly Rent Per Unit Monthly Expenses Vacancy Rate Inflation Overall Capitalization Rate Terminal Cap Rate Present Value Discount Rate D $500 $200 7% 2.50% 9.00% 9.50% 11.00% Price Land to Building Ratio Price Allocated to Bldg. Price Allocated to Land $ 1,766,667 (First Year NOI Capitalized at above Rate) 20.00% $ 1,413,333 $ 353,333 Cost Recovery Period Income Tax Rate Capital Gains Rate 27.5 28.0% 15.0% Loan to Value Term Interest Rate 75% 25 (25 Year Term Amortized Monthly) 7.5% Year Loan Payment EOY Bal. Interest 1 $ 1,325,000 $9,791.63 $1,306,239 $98,739 2 $1,306,239 $9,791.63 $1,286,022 $97,282 3 $1,286,022 $9,791.63 $1,264,235 $95,713 4 $1,264,235 $9,791.63 $1,240,757 $94,021 5 $1,240,757 $9,791.63 $1,215,456 $92,199 $1,215,456 $9,791.63 $1,188,191 S90,235 Before Tax Cash Flows Gross Income Less Vacancy $ $ $ $ Effective Gross Income Less Operating Expenses Net Operating Income Annual Debt Service Rafnra Taxrach Flue from oneratione Criminal Shoot Shoot 1 300,000 $ 7% 21,000 $ 279,000 $ 120,000 $ 159,000 $ $117.500 11 2 307,500 $ 7% 21,525 $ 285,975 $ 123,000 $ 162,975 S $117.500 45 475 3 315,188 $ 7% 22,063 S 293,124 S 126,075 $ 167,049 $ $117.500 A 550 4 323,067 S 796 22,615$ 300,452 S 129,227 S 171,226 S $117.500 52726 5 331,144 $ 7% 23,180 S 307,964 $ 132,458 $ 175,506 $ $117.500 CR 007 339,422 7% 23,760 315,663 135,769 179,894 $117.500 6 104 $ Before Tax Cash Flow from Operations $ $ 41,500 $ 45,475 S 49,550 $ G 53.7265 H 58,007 S 1 62,394 $ 310,653 $ $ After Tax Cash Flow Net Operating Income Depreciation interest Taxable income Taxes After Tax Cash Flow from Operations 159,000 $ 51,394 $ $98.729 8,867 S 2,4835 39,018 5 S $ $ 162,975$ 51,394 $ $97282 14,299 $ 4,004 S 41.4725 167,049 $ 51,3945 $95.713 19,43 $ 5,584 S 43,966 $ 171,226 51,394 S 594,021 25,8105 7,2275 46,499 $ 175,506 S 51,3945 $92.199 31,914 $ 8,936 $ 49,071 S 179,894 51,394 $90.235 38,265 10,714 51,680 5 271,705 Sales Price Less Sales Exp-3% Gross Proceeds Basis Capital Gain Capital Gain Tax Net Gain $ 1,715,526 S 1,758,414 $ 1.802,375 $ 1,847,434 $ 1,893,620 $ 51,466 S 52,752 5 54,071 S 55,423 5 56,809 $ 1,664,061 $ 1,705,662 S 1.748,304 $1,792,011 S 1,836,811 $ 1,715,273 1,663.879'S 1,612,485'S 1.561,091's 1.509,697 $ (51,212) S 41,783 S 135,819 $ 230,920 S 327,114 $ (7,682)'s 6,267'S 20,373's 34,638'S 49,067 $ (43,530) $ 35,516 5 115,446 5 196,282 S 278,047 After Tax Net Proceeds from Sale 5 572,288 Before Tax CF Operations and Sale Equity (441,667) S S Yr 1 41,500 $ Yr 2 45,475 S YO 49.550 $ Yr 4 53,726 S YrS 706,627 IRR Before Tax Cash Flows NPV 17.6% $111,351 5 39,018 5 41,472 $ 43,966 $ After Tax Cash Flows IRR ATCE NPV 46,499 $ 621,359 (441,667) S 14.3% $52,854 Breakeven Occupancy: 79% 78% 77% 76% 75% 75% Partition ATIRR: PV Alter Tax Cash Flows from Operations PV After Tax Sales Proceeds Original Sheet2 Sheet $147,852.68 $293.813.99 % 33% 62% PER 3. More typically increases in inflation would result in increases in the Terminal Cap Rate and the required Internal Rate of Return. How would the value of the property be affected if the one half percentage point or 50 basis point increase in inflation from 2.5% to 3.0% results in one half percentage point or 50 basis point increases in both the Terminal Capitalization Rate and the Internal Rate of Return? 4. The lender requires a minimum Debt Coverage Ratio of 1.3 for the first year of the analysis. All else being equal / unchanged from the original spreadsheet is an 80% Loan to Value possible? 5. As a follow up and similar question as number No. 4 above the borrower would like a loan with a 20 year term, as that would result in a lower interest rate of 7.0%. Based upon the original 75% Loan to Value would it be possible to get a 20-year term and 7.0% interest rate and meet the lender's 1.3 Debt Coverage ratio requirement? 6. In the model the 2.5% annual inflation rate is applied to both the rental income and expenses. If expenses increase at a greater rate (3.0%) would the value of the property increase? The model is not set up to differentiate so I am not looking for an exact mathematical amount but I want to see an understanding of the concepts. 7. The purchase price of the property has been estimated by applying the Overall Capitalization Rate to the first year NOI. If all else is equal or unchanged and the Overall Capitalization Rate is decreased from 9.0% to 8.5% how will it affect the amount of equity required to purchase the property? 8. If the land to building ratio increases from 20% to 25% what happens to the After-Tax Cash Flows? JA JUU E F H 8 Average Monthly Rent Per Unit Monthly Expenses Vacancy Rate Inflation Overall Capitalization Rate Terminal Cap Rate Present Value Discount Rate D $500 $200 7% 2.50% 9.00% 9.50% 11.00% Price Land to Building Ratio Price Allocated to Bldg. Price Allocated to Land $ 1,766,667 (First Year NOI Capitalized at above Rate) 20.00% $ 1,413,333 $ 353,333 Cost Recovery Period Income Tax Rate Capital Gains Rate 27.5 28.0% 15.0% Loan to Value Term Interest Rate 75% 25 (25 Year Term Amortized Monthly) 7.5% Year Loan Payment EOY Bal. Interest 1 $ 1,325,000 $9,791.63 $1,306,239 $98,739 2 $1,306,239 $9,791.63 $1,286,022 $97,282 3 $1,286,022 $9,791.63 $1,264,235 $95,713 4 $1,264,235 $9,791.63 $1,240,757 $94,021 5 $1,240,757 $9,791.63 $1,215,456 $92,199 $1,215,456 $9,791.63 $1,188,191 S90,235 Before Tax Cash Flows Gross Income Less Vacancy $ $ $ $ Effective Gross Income Less Operating Expenses Net Operating Income Annual Debt Service Rafnra Taxrach Flue from oneratione Criminal Shoot Shoot 1 300,000 $ 7% 21,000 $ 279,000 $ 120,000 $ 159,000 $ $117.500 11 2 307,500 $ 7% 21,525 $ 285,975 $ 123,000 $ 162,975 S $117.500 45 475 3 315,188 $ 7% 22,063 S 293,124 S 126,075 $ 167,049 $ $117.500 A 550 4 323,067 S 796 22,615$ 300,452 S 129,227 S 171,226 S $117.500 52726 5 331,144 $ 7% 23,180 S 307,964 $ 132,458 $ 175,506 $ $117.500 CR 007 339,422 7% 23,760 315,663 135,769 179,894 $117.500 6 104 $ Before Tax Cash Flow from Operations $ $ 41,500 $ 45,475 S 49,550 $ G 53.7265 H 58,007 S 1 62,394 $ 310,653 $ $ After Tax Cash Flow Net Operating Income Depreciation interest Taxable income Taxes After Tax Cash Flow from Operations 159,000 $ 51,394 $ $98.729 8,867 S 2,4835 39,018 5 S $ $ 162,975$ 51,394 $ $97282 14,299 $ 4,004 S 41.4725 167,049 $ 51,3945 $95.713 19,43 $ 5,584 S 43,966 $ 171,226 51,394 S 594,021 25,8105 7,2275 46,499 $ 175,506 S 51,3945 $92.199 31,914 $ 8,936 $ 49,071 S 179,894 51,394 $90.235 38,265 10,714 51,680 5 271,705 Sales Price Less Sales Exp-3% Gross Proceeds Basis Capital Gain Capital Gain Tax Net Gain $ 1,715,526 S 1,758,414 $ 1.802,375 $ 1,847,434 $ 1,893,620 $ 51,466 S 52,752 5 54,071 S 55,423 5 56,809 $ 1,664,061 $ 1,705,662 S 1.748,304 $1,792,011 S 1,836,811 $ 1,715,273 1,663.879'S 1,612,485'S 1.561,091's 1.509,697 $ (51,212) S 41,783 S 135,819 $ 230,920 S 327,114 $ (7,682)'s 6,267'S 20,373's 34,638'S 49,067 $ (43,530) $ 35,516 5 115,446 5 196,282 S 278,047 After Tax Net Proceeds from Sale 5 572,288 Before Tax CF Operations and Sale Equity (441,667) S S Yr 1 41,500 $ Yr 2 45,475 S YO 49.550 $ Yr 4 53,726 S YrS 706,627 IRR Before Tax Cash Flows NPV 17.6% $111,351 5 39,018 5 41,472 $ 43,966 $ After Tax Cash Flows IRR ATCE NPV 46,499 $ 621,359 (441,667) S 14.3% $52,854 Breakeven Occupancy: 79% 78% 77% 76% 75% 75% Partition ATIRR: PV Alter Tax Cash Flows from Operations PV After Tax Sales Proceeds Original Sheet2 Sheet $147,852.68 $293.813.99 % 33% 62% PER