3' preview File Edit View Go Tools Window Help 93' 9 Q Q 8 Sun13Mar 5:47PM [I] V lecture notes_Macro Ill.pdf Page 21 of 114

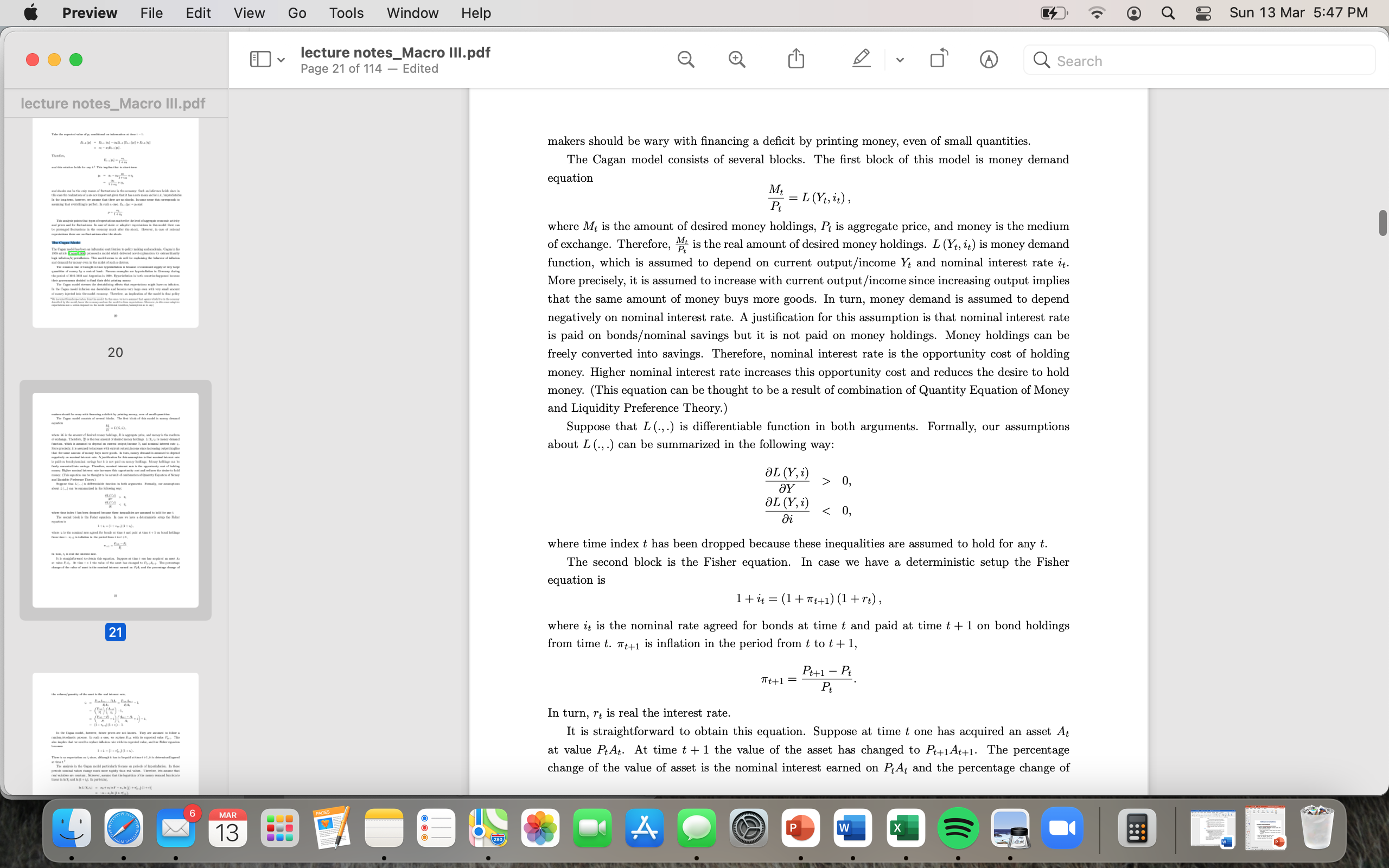

3' preview File Edit View Go Tools Window Help 93' "9 Q Q 8 Sun13Mar 5:47PM [I] V lecture notes_Macro Ill.pdf Page 21 of 114 Edited lecture notes_Macro Ill.pdf m 9 V d Q Search makers should be wry with nancing a decit by printing money, even of small quantities. ' The Cagan model consists of several blocks. The rst block of this model is money demand ' equation M . F: = L (n, u) , where M; is the amount of desired money holdings, P, is aggregate price, and money is the medium | of exchange. Therefore, %f is the real amount of desired money holdings, L (Yb 1") is money demand function, which is assumed to depend on current output/income Y, and nominal interest rate I", More precisely, it is assumed to increase with current output/income since increasing output implies that the same amount of money buys more goods, In turn, money demand is assumed to depend negatively on nominal interest rate A justication for this assumption is that nominal interest rate is paid on bondsominal savings but it is not paid on money holdings Money holdings can be freely converted into savings Therefore, nominal interest rate is the opportunity cost of holding money Higher nominal interest rate increases this opportunity cost and reduces the desire to hold money (This equation can be thought to be a result of combination of Quantity Equation of Money , and Liquidity Preference Theory.) ' Suppose that L(., r) is differentiable function in both arguments. Formally, our assumptions about L (i, r) can be summarized in the following way: sum) ' BY > 0, ' sum 0 a,- , where time index t has been dropped became these inequalities are assumed to hold for any t. The second block is the Fisher equation In case we have a deterministic setup the Fisher equation is 1 +11 =(1+1rr+1)(1 +11): where it is the nominal rate agreed for bonds at time t and paid at time t + 1 on bond holdings from time t. 7r+1 is ination in the period from t to t + 1, P+1 *Pe n+1 = . In turn, 1', is real the interest rate It is straightforward to obtain this equation. Suppose at time it one has acquired an asset A; at value PgAti At time t + 1 the value of the asset has changed to Pg+1Ag+L The percentage change of the value of asset is the nominal interest earned on HA; and the percentage change of Preview File View Go Tools Window Help 4 2 Q 2 Sun 13 Mar 5:47 PM lecture notes_Macro Ill.pdf Page 22 of 114 - Edited Q Search lecture notes_Macro Ill.pdf the volume/ quantity of the asset is the real interest rate, it = Pt+1At+1 - PtAt _ PttiAt+1 _ 1, P&At P&At Piti Atti ) - 1, 20 = = (Pt+1 - Pt + 1 (Anti - At + 1) - 1, Pt At = (1+ "t+1) (1 + rt) - 1. In the Cagan model, however, future prices are not known. They are assumed to follow a random/stochastic process. In such a case, we replace Pt+1 with its expected value Pre1. This also implies that we need to replace inflation rate with its expected value, and the Fisher equation becomes 1 tit = (1+ mi+1) (1 + rt) . There is no expectation on it since, although it has to be paid at time t + 1, it is determined/ agreed at time t.9 The analysis in the Cagan model particularly focuses on periods of hyperinflation. In these periods nominal values change much more rapidly than real values. Therefore, lets assume that real variables are constant. Moreover, assume that the logarithm of the money demand function is 21 linear in In Yt and In (1 + it). In particular, In L (Yt, it) = do + allnY - anIn [(1 + mi+1) (1+r)] = : a - an In (1+ mi+1) , where do, @1, and a, are positive constants and a = @ + aj In Y - a, In (1 + r). In such a case, combining money demand equation and the Fisher equation we have to have that In Mt - In Pt = a - ax (In Pe+1 - In Pt) . Denote z = In Z and rewrite the equation above in the following way mt - Pt = Q - ar (Pt+1 - Pt) , or Pt = - 7 1+a, 1+a, an piti , + 1+a, 22 This is a fairly interesting equation. It suggests that current price is function of current money supply and expected price level in future. Moreover, current price increases with money supply. This 6 MAR 13 4 WAssignment 2 - The Cagan Model Submit your assignment using Virtual Campus. You can perform this assignment in a group of maximum 3 people. 1. Assume that the supply of money (in logarithms) is equal to mt pt and the demand for money (in logarithms) depends solely on expected ination (1r;5 +1 2 pf +1 pi) and is equal to: mt '19: = '3 (pfH 'Pt) - Suppose that at time t = 0, 1 and 2, the nominal money stock (in logarithms) is equal to 100 (Le, m0 = m1 = m2 = 100) and the price index (in logarithms) is equal to 100 at time t = 0 and 1 (Le, p0 2 p1 = 100). At t = 1, the central bank announces that the nominal money stock will increase at t = 3 to m3 = 150 and remain at that level forever. (a) Use demand and supply of money to derive price level pt for any time t as a function of the nominal money stock mt and expected price level in the next period 303 +1. (b) Suppose that agents' have adaptive expectations of the following form: a 3 1 Pt = apt1 'l' apt2- Calculate the price level at time t = 2, 3, 4, and 5: 392,193, 114, p5

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance