Answered step by step

Verified Expert Solution

Question

1 Approved Answer

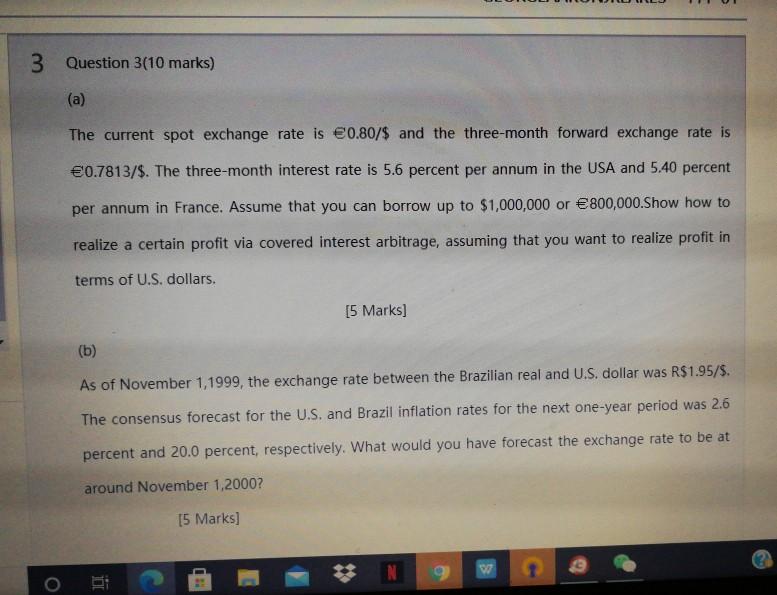

3 Question 3(10 marks) (a) The current spot exchange rate is 0.80/$ and the three-month forward exchange rate is 0.7813/$. The three-month interest rate is

3 Question 3(10 marks) (a) The current spot exchange rate is 0.80/$ and the three-month forward exchange rate is 0.7813/$. The three-month interest rate is 5.6 percent per annum in the USA and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or 800,000.Show how to realize a certain profit via covered interest arbitrage, assuming that you want to realize profit in terms of U.S. dollars. [5 Marks] (b) As of November 1,1999, the exchange rate between the Brazilian real and U.S. dollar was R$1.95/$. The consensus forecast for the U.S. and Brazil inflation rates for the next one-year period was 2.6 percent and 20.0 percent, respectively. What would you have forecast the exchange rate to be at around November 1,2000? [5 Marks) @ w o

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Finance Book

Authors: Stuart Warner, Si Hussain

1st Edition

1292123648, 978-1292123646