Answered step by step

Verified Expert Solution

Question

1 Approved Answer

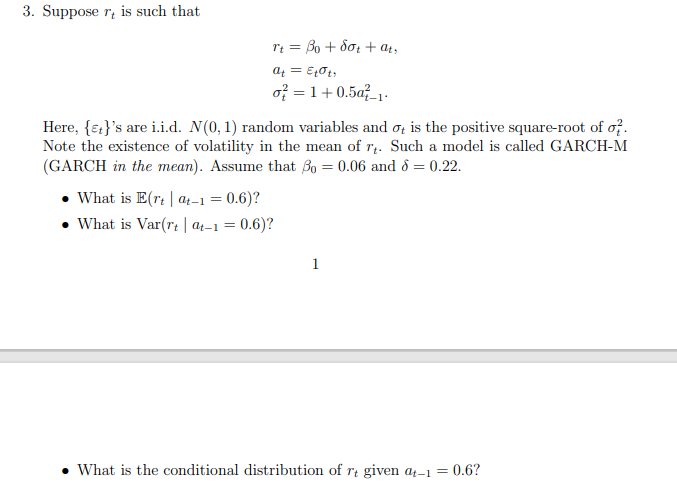

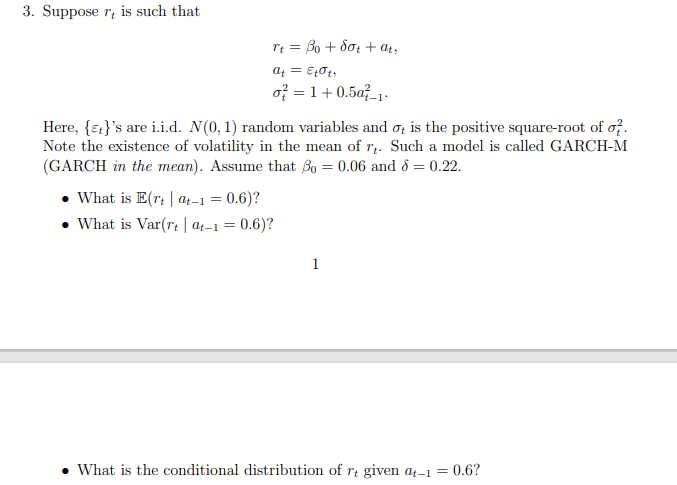

3. Suppose r, is such that It = Bo+ dot + at, of = 1 + 0.507-1. Here, {et}'s are i.i.d. N(0, 1) random variables

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Discrete Mathematics With Applications

Authors: Susanna S Epp, Robert Gatewood,

4th Edition

1133168663, 9781133168669