Answered step by step

Verified Expert Solution

Question

1 Approved Answer

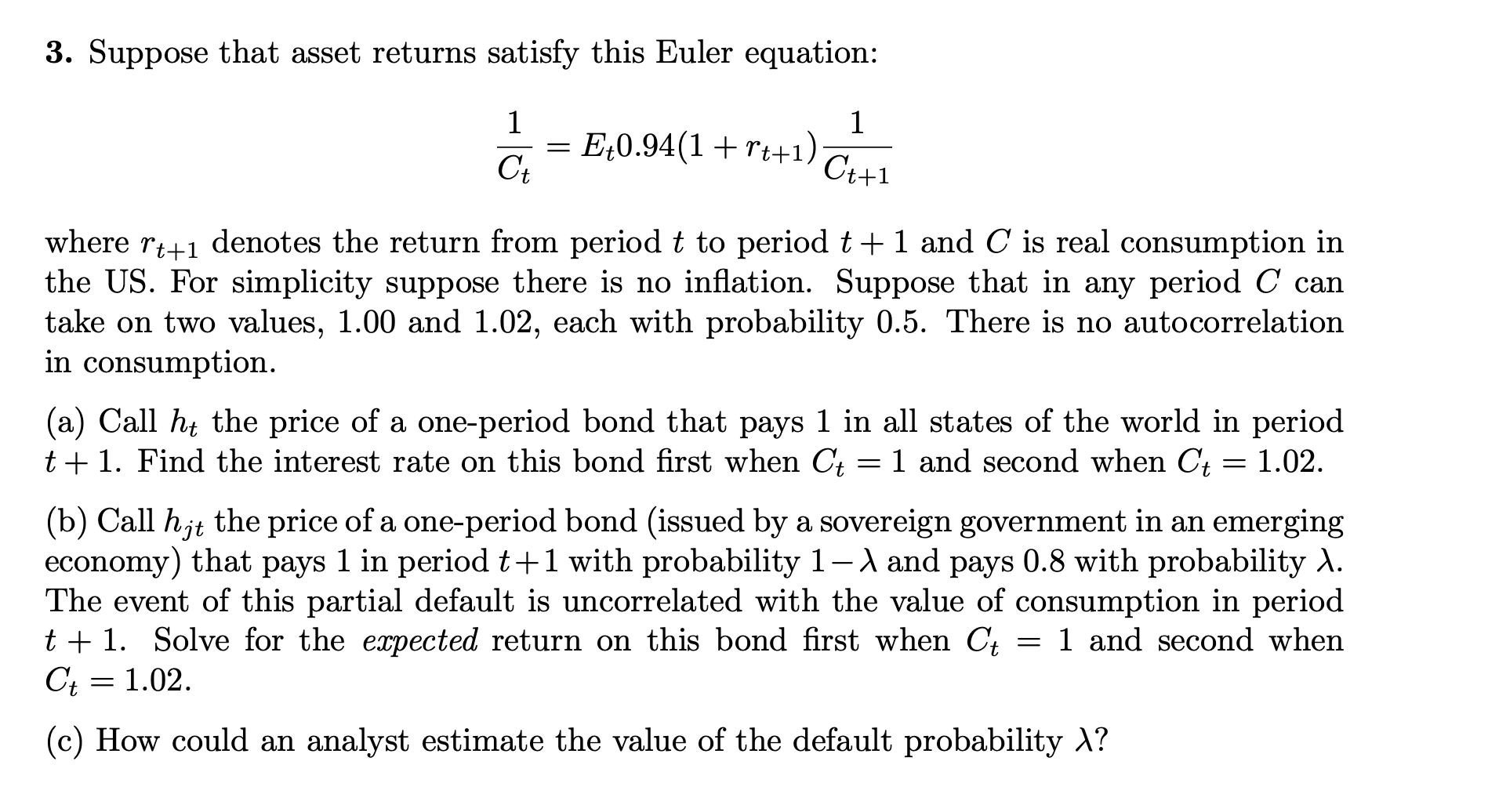

3. Suppose that asset returns satisfy this Euler equation: 1 1 =E+0.94(1+rt+1) Ct C++1 where t+1 denotes the return from period t to period

3. Suppose that asset returns satisfy this Euler equation: 1 1 =E+0.94(1+rt+1) Ct C++1 where t+1 denotes the return from period t to period t+1 and C is real consumption in the US. For simplicity suppose there is no inflation. Suppose that in any period C can take on two values, 1.00 and 1.02, each with probability 0.5. There is no autocorrelation in consumption. (a) Call ht the price of a one-period bond that pays 1 in all states of the world in period t+1. Find the interest rate on this bond first when C = 1 and second when Ct = 1.02. (b) Call hit the price of a one-period bond (issued by a sovereign government in an emerging economy) that pays 1 in period t+1 with probability 1- and pays 0.8 with probability . The event of this partial default is uncorrelated with the value of consumption in period t + 1. Solve for the expected return on this bond first when Ct = 1 and second when C = 1.02. (c) How could an analyst estimate the value of the default probability \?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Financial Management

Authors: Brigham, Daves

10th Edition

978-1439051764, 1111783659, 9780324594690, 1439051763, 9781111783655, 324594690, 978-1111021573