Answered step by step

Verified Expert Solution

Question

1 Approved Answer

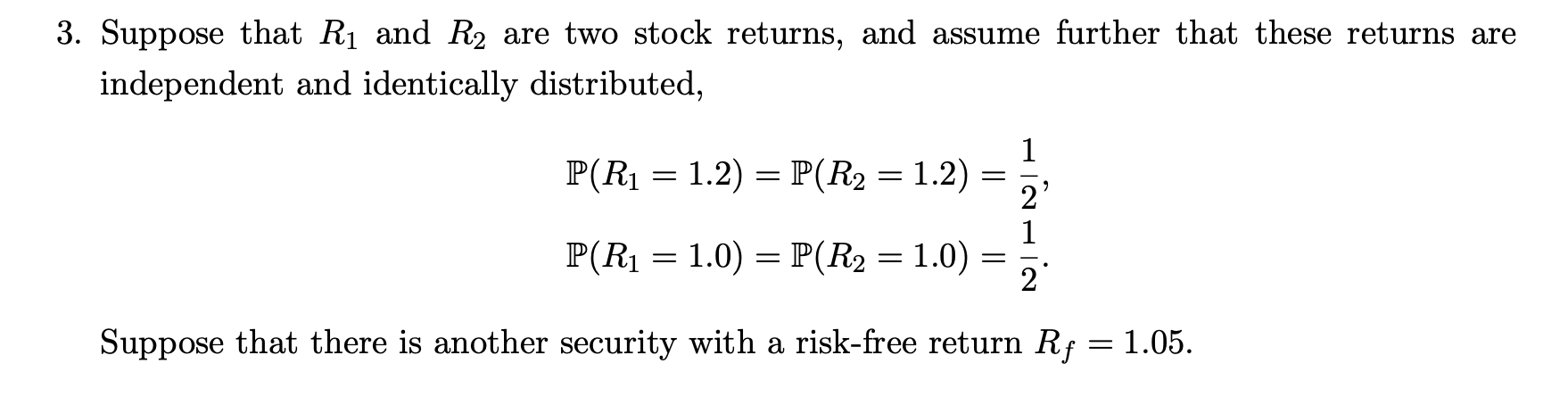

3. Suppose that R1 and R2 are two stock returns, and assume further that these returns are independent and identically distributed, P(R1=1.2)=P(R2=1.2)=21,P(R1=1.0)=P(R2=1.0)=21. Suppose that there

3. Suppose that R1 and R2 are two stock returns, and assume further that these returns are independent and identically distributed, P(R1=1.2)=P(R2=1.2)=21,P(R1=1.0)=P(R2=1.0)=21. Suppose that there is another security with a risk-free return Rf=1.05. (b) Taking the safe asset and the two risky securities as basis assets find the (range of) riskneutral probabilities in this model and decide whether there are arbitrage opportunities

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cash Flow Stock Investing

Authors: Randall Stewart

1st Edition

1980883300, 978-1980883302