Question

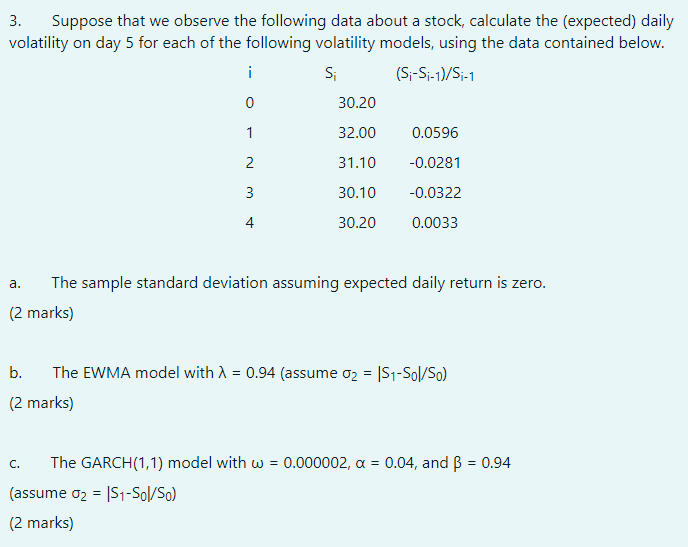

3. Suppose that we observe the following data about a stock, calculate the (expected) daily volatility on day 5 for each of the following volatility

3. Suppose that we observe the following data about a stock, calculate the (expected) daily volatility on day 5 for each of the following volatility models, using the data contained below.

| i | Si | (Si-Si-1)/Si-1 |

| 0 | 30.20 | |

| 1 | 32.00 | 0.0596 |

| 2 | 31.10 | -0.0281 |

| 3 | 30.10 | -0.0322 |

| 4 | 30.20 | 0.0033 |

a. The sample standard deviation assuming expected daily return is zero.

(2 marks)

b. The EWMA model with = 0.94 (assume 2 = |S1-S0|/S0)

(2 marks)

c. The GARCH(1,1) model with = 0.000002, = 0.04, and = 0.94

(assume 2 = |S1-S0|/S0)

(2 marks)

3. Suppose that we observe the following data about a stock, calculate the expected) daily volatility on day 5 for each of the following volatility models, using the data contained below. i Si (5:-S:-1)/S-1 0 30.20 1 32.00 0.0596 2 31.10 -0.0281 3 30.10 -0.0322 4 4 30.20 0.0033 a. The sample standard deviation assuming expected daily return is zero. (2 marks) b. The EWMA model with 1 = 0.94 (assume 02 = 1S1-Sol/So) (2 marks) C. The GARCH(1,1) model with w = 0.000002, a = 0.04, and B = 0.94 (assume 02 = 151-5ol/50) (2 marks) 3. Suppose that we observe the following data about a stock, calculate the expected) daily volatility on day 5 for each of the following volatility models, using the data contained below. i Si (5:-S:-1)/S-1 0 30.20 1 32.00 0.0596 2 31.10 -0.0281 3 30.10 -0.0322 4 4 30.20 0.0033 a. The sample standard deviation assuming expected daily return is zero. (2 marks) b. The EWMA model with 1 = 0.94 (assume 02 = 1S1-Sol/So) (2 marks) C. The GARCH(1,1) model with w = 0.000002, a = 0.04, and B = 0.94 (assume 02 = 151-5ol/50) (2 marks)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The House That Bogle Built How John Bogle And Vanguard Reinvented The Mutual Fund Industry

Authors: Lewis Braham

1st Edition

0071749063,0071751157