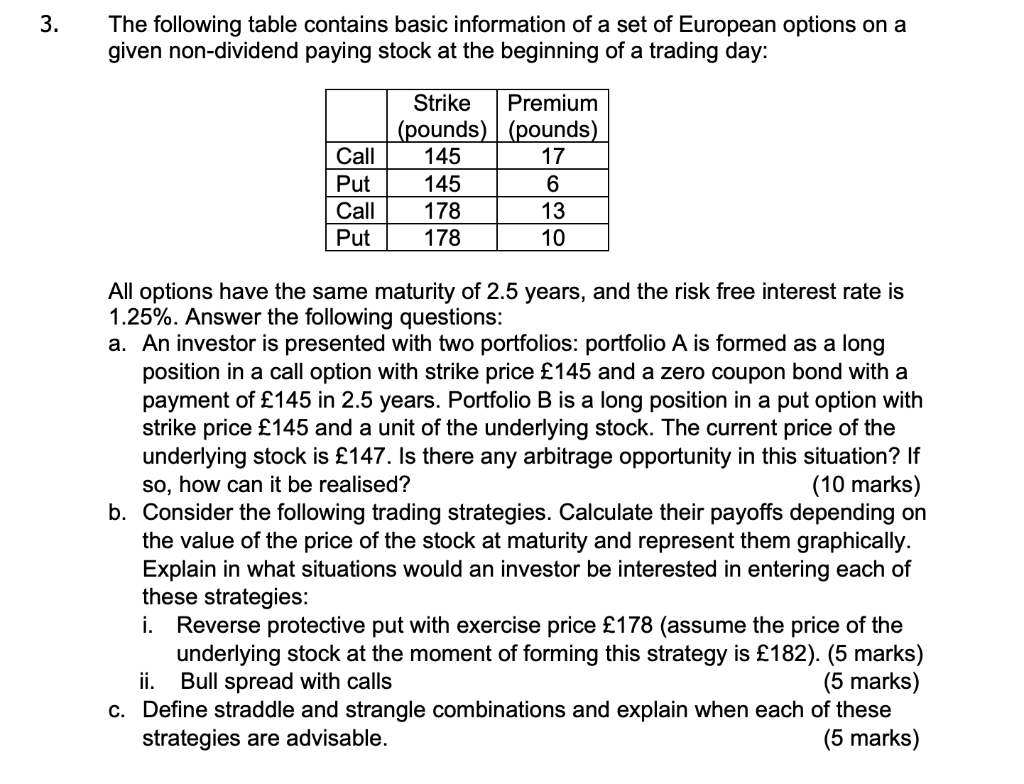

3. The following table contains basic information of a set of European options on a given non-dividend paying stock at the beginning of a trading day: Call Put Call Put Strike Premium (pounds) (pounds) 145 17 145 6 178 13 178 10 All options have the same maturity of 2.5 years, and the risk free interest rate is 1.25%. Answer the following questions: a. An investor is presented with two portfolios: portfolio A is formed as a long position in a call option with strike price 145 and a zero coupon bond with a payment of 145 in 2.5 years. Portfolio B is a long position in a put option with strike price 145 and a unit of the underlying stock. The current price of the underlying stock is 147. Is there any arbitrage opportunity in this situation? If So, how can it be realised? (10 marks) b. Consider the following trading strategies. Calculate their payoffs depending on the value of the price of the stock at maturity and represent them graphically. Explain in what situations would an investor be interested in entering each of these strategies: i. Reverse protective put with exercise price 178 (assume the price of the underlying stock at the moment of forming this strategy is 182). (5 marks) ii. Bull spread with calls (5 marks) c. Define straddle and strangle combinations and explain when each of these strategies are advisable. (5 marks) 3. The following table contains basic information of a set of European options on a given non-dividend paying stock at the beginning of a trading day: Call Put Call Put Strike Premium (pounds) (pounds) 145 17 145 6 178 13 178 10 All options have the same maturity of 2.5 years, and the risk free interest rate is 1.25%. Answer the following questions: a. An investor is presented with two portfolios: portfolio A is formed as a long position in a call option with strike price 145 and a zero coupon bond with a payment of 145 in 2.5 years. Portfolio B is a long position in a put option with strike price 145 and a unit of the underlying stock. The current price of the underlying stock is 147. Is there any arbitrage opportunity in this situation? If So, how can it be realised? (10 marks) b. Consider the following trading strategies. Calculate their payoffs depending on the value of the price of the stock at maturity and represent them graphically. Explain in what situations would an investor be interested in entering each of these strategies: i. Reverse protective put with exercise price 178 (assume the price of the underlying stock at the moment of forming this strategy is 182). (5 marks) ii. Bull spread with calls (5 marks) c. Define straddle and strangle combinations and explain when each of these strategies are advisable