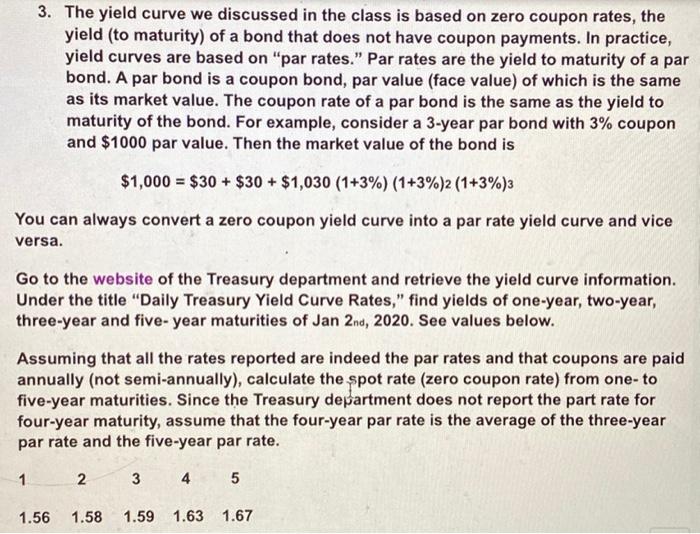

3. The yield curve we discussed in the class is based on zero coupon rates, the yield (to maturity) of a bond that does not have coupon payments. In practice, yield curves are based on "par rates." Par rates are the yield to maturity of a par bond. A par bond is a coupon bond, par value (face value) of which is the same as its market value. The coupon rate of a par bond is the same as the yield to maturity of the bond. For example, consider a 3-year par bond with 3% coupon and $1000 par value. Then the market value of the bond is $1,000 = $30 + $30 + $1,030 (1+3%) (1+3%)2 (1+3%)3 You can always convert a zero coupon yield curve into a par rate yield curve and vice versa. Go to the website of the Treasury department and retrieve the yield curve information. Under the title "Daily Treasury Yield Curve Rates," find yields of one-year, two-year, three-year and five-year maturities of Jan 2nd, 2020. See values below. Assuming that all the rates reported are indeed the par rates and that coupons are paid annually (not semi-annually), calculate the spot rate (zero coupon rate) from one-to five-year maturities. Since the Treasury department does not report the part rate for four-year maturity, assume that the four-year par rate is the average of the three-year par rate and the five-year par rate. 1 2 3 4 5 1.56 1.58 1.59 1.63 1.67 3. The yield curve we discussed in the class is based on zero coupon rates, the yield (to maturity) of a bond that does not have coupon payments. In practice, yield curves are based on "par rates." Par rates are the yield to maturity of a par bond. A par bond is a coupon bond, par value (face value) of which is the same as its market value. The coupon rate of a par bond is the same as the yield to maturity of the bond. For example, consider a 3-year par bond with 3% coupon and $1000 par value. Then the market value of the bond is $1,000 = $30 + $30 + $1,030 (1+3%) (1+3%)2 (1+3%)3 You can always convert a zero coupon yield curve into a par rate yield curve and vice versa. Go to the website of the Treasury department and retrieve the yield curve information. Under the title "Daily Treasury Yield Curve Rates," find yields of one-year, two-year, three-year and five-year maturities of Jan 2nd, 2020. See values below. Assuming that all the rates reported are indeed the par rates and that coupons are paid annually (not semi-annually), calculate the spot rate (zero coupon rate) from one-to five-year maturities. Since the Treasury department does not report the part rate for four-year maturity, assume that the four-year par rate is the average of the three-year par rate and the five-year par rate. 1 2 3 4 5 1.56 1.58 1.59 1.63 1.67