Answered step by step

Verified Expert Solution

Question

1 Approved Answer

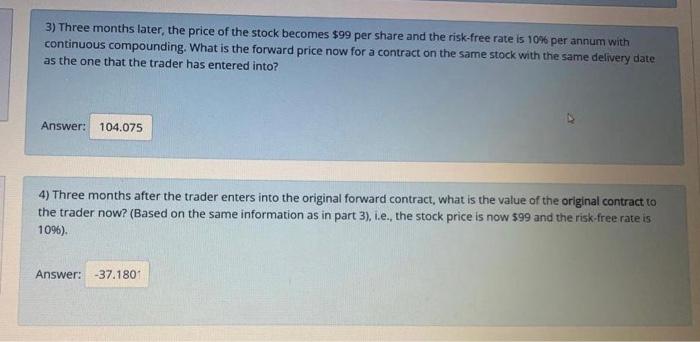

3) Three months later, the price of the stock becomes $99 per share and the risk-free rate is 10% per annum with continuous compounding. What

3) Three months later, the price of the stock becomes $99 per share and the risk-free rate is 10% per annum with continuous compounding. What is the forward price now for a contract on the same stock with the same delivery date as the one that the trader has entered into? Answer: 104.075 4) Three months after the trader enters into the original forward contract, what is the value of the original contract to the trader now? (Based on the same information as in part 3), i.e., the stock price is now $99 and the risk-free rate is 1096). Answer: 37.1807

3) Three months later, the price of the stock becomes $99 per share and the risk-free rate is 10% per annum with continuous compounding. What is the forward price now for a contract on the same stock with the same delivery date as the one that the trader has entered into? Answer: 104.075 4) Three months after the trader enters into the original forward contract, what is the value of the original contract to the trader now? (Based on the same information as in part 3), i.e., the stock price is now $99 and the risk-free rate is 1096). Answer: 37.1807

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Alpha Hunter Profiting From Option LEAPS

Authors: Jason Schwarz

1st Edition

0071634088