Question: 3. Using the methodology outlined in Exhibit 13.11, forecast the operating items on the next five years of balance sheets for PartsCo. Forecast each balance

3. Using the methodology outlined in Exhibit 13.11, forecast the operating items on the next five years of balance sheets for PartsCo. Forecast each balance sheet item as a function of revenues, except inventory and accounts payable, which should be forecast as a function of cost of sales. Your forecast should be consistent with the revenues and cost of sales forecast in Question 2. (Note that Exhibit 13.11 converts figures to number of days. You do not need to go this extra step. You can just compute the historical ratios as a percentage of either revenues or cost of goods sold and use those ratios for the forecast.) 4. Using the methodology outlined in Exhibits 13.12 and 13.13, forecast the financing items on next year's balance sheet for PartsCo. Assume that short-term debt remains at $90 million, long-term debt remains at $210 million, no equity is raised, and the firm maintains the same dividend payout ratio as the current year. Use either newly issued debt or excess cash and marketable securities as the funding plug to balance the balance sheet. Your forecast should be consistent with the forecasts in Questions 2 and 3. 5. The chief financial officer of PartsCo has asked you to rerun the forecast of the company's income statement and balance sheet at a growth rate of 3 percent. If the company generates more cash than it needs, how could the balance sheet be adjusted to handle this? What alternatives exist to handle new cash? 6. The chief financial officer of PartsCo returns again and explains that there is a possibility of a huge contract being awarded to the company. If this occurs, then the company is expected to achieve 25 percent revenue growth annually for the next five years. How does this affect the pro forma balance sheet? Which accounts are notably different than in the prior situations?

A. Start with the terminal nodes that represent the last time step. At node Sou3, the expected asset value is $1,215 million. Since this is greater than $100 million, you would invest and realize a net payoff of $1,115 million ($1,215 million - $100 million). The option value at this node now would be $1,115 million. B. At node Soud2, the expected asset value is $0; therefore, no investment would be made, resulting in an option value of $0 at that node. C. Next, move on to the intermediate nodes, one step away from the last time step. Starting at the top, at node Sou2, calculate the expected asset value for keeping the option open. This is simply the discounted (at the risk-free rate) weighted average of potential future option values using the risk-neutral probability as weights: [p(Sou3) + (1 - p)(Sou2d)] * exp(-r?t) = [0.485($1,115 million) + (1 - 0.485)($251 million)] * exp(-0.05)(1) = $638 million The expected asset value at this node is $733 million. Exercising the option at this node will provide an option value of $633 million ($733 million - $100 million). Since the value of keeping the option open is larger than this, you would keep the option open and continue; therefore, the option value at Sou2 is $638 million. D. Similarly, at node Soud, the expected asset value for keeping the option open, taking into account the downstream optimal decisions, is: [0.485($251 million) + (1 - 0.485)($0 million)] * exp(-0.05)(1) = $116 million The expected asset value at this node is $162 million. Exercising the option at this node will provide an option value of $62 million ($162 million - $100 million). Since the value of keeping the option open is larger than this, you would keep the option open and continue; therefore, the option value at Soud is $116 million. E. Complete the option valuation binomial tree all the way to time = 0 using the approach outlined above. 6. Analyze the results The project NPV is calculated to be $0 million for a payoff of $600 million, assuming the total investment of $600 million ($500 million + $100 million)

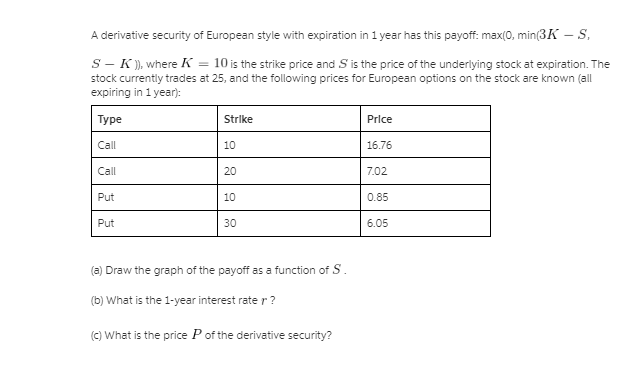

A derivative security of European style with expiration in 1 year has this payoff: max(0, min(3K - S, S-K)), where K = 10 is the strike price and S' is the price of the underlying stock at expiration. The stock currently trades at 25, and the following prices for European options on the stock are known (all expiring in 1 year): Strike Price Call 10 16.76 Call 20 7.02 Put 10 0.85 Put 30 6.05 (a) Draw the graph of the payoff as a function of S. (b) What is the 1-year interest rate r? (c) What is the price P of the derivative security?

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts