Answered step by step

Verified Expert Solution

Question

1 Approved Answer

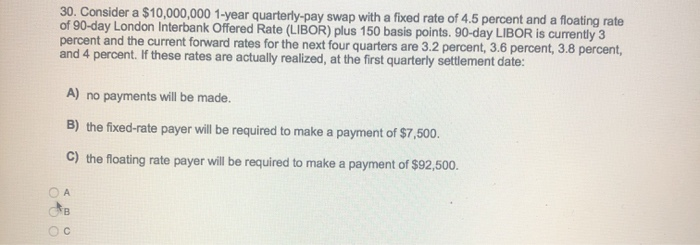

30. Consider a $10,000,000 1-year quarterly-pay swap with a fixed rate of 4.5 percent and a floating rate of 90-day London Interbank Offered Rate (LIBOR)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Do Not Blame The Shorts Why Short Sellers Are Always Blamed For Market Crashes And How History Is Repeating Itself

Authors: Robert Sloan

1st Edition

0071636862,0071636870