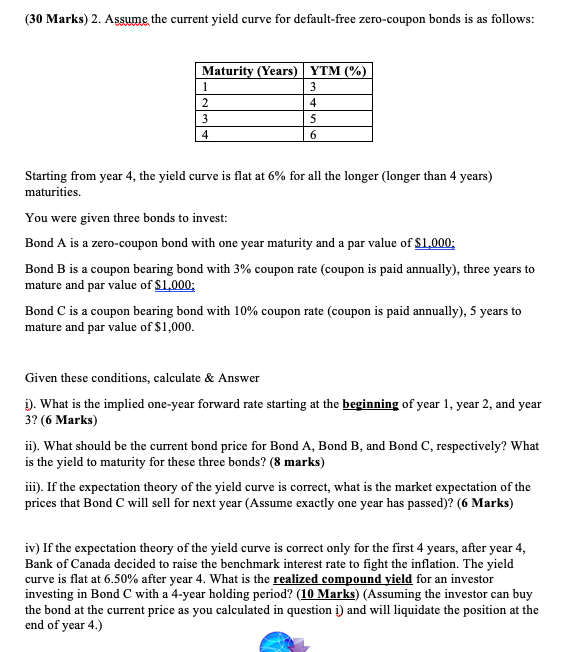

(30 Marks) 2. Assume the current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) YTM (%) 1 3 2 4 3 5 4 6 w Starting from year 4, the yield curve is flat at 6% for all the longer (longer than 4 years) maturities. You were given three bonds to invest: Bond A is a zero-coupon bond with one year maturity and a par value of $1,000; Bond B is a coupon bearing bond with 3% coupon rate (coupon is paid annually), three years to mature and par value of $1,000: Bond C is a coupon bearing bond with 10% coupon rate (coupon is paid annually), 5 years to mature and par value of $1,000. Given these conditions, calculate & Answer 1). What is the implied one-year forward rate starting at the beginning of year 1, year 2, and year 3? (6 Marks) ii). What should be the current bond price for Bond A, Bond B, and Bond C, respectively? What is the yield to maturity for these three bonds? (8 marks) iii). If the expectation theory of the yield curve is correct, what is the market expectation of the prices that Bond C will sell for next year (Assume exactly one year has passed)? (6 Marks) iv) If the expectation theory of the yield curve is correct only for the first 4 years, after year 4, Bank of Canada decided to raise the benchmark interest rate to fight the inflation. The yield curve is flat at 6.50% after year 4. What is the realized compound yield for an investor investing in Bond C with a 4-year holding period? (10 Marks) (Assuming the investor can buy the bond at the current price as you calculated in question i) and will liquidate the position at the end of year 4.) (30 Marks) 2. Assume the current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) YTM (%) 1 3 2 4 3 5 4 6 w Starting from year 4, the yield curve is flat at 6% for all the longer (longer than 4 years) maturities. You were given three bonds to invest: Bond A is a zero-coupon bond with one year maturity and a par value of $1,000; Bond B is a coupon bearing bond with 3% coupon rate (coupon is paid annually), three years to mature and par value of $1,000: Bond C is a coupon bearing bond with 10% coupon rate (coupon is paid annually), 5 years to mature and par value of $1,000. Given these conditions, calculate & Answer 1). What is the implied one-year forward rate starting at the beginning of year 1, year 2, and year 3? (6 Marks) ii). What should be the current bond price for Bond A, Bond B, and Bond C, respectively? What is the yield to maturity for these three bonds? (8 marks) iii). If the expectation theory of the yield curve is correct, what is the market expectation of the prices that Bond C will sell for next year (Assume exactly one year has passed)? (6 Marks) iv) If the expectation theory of the yield curve is correct only for the first 4 years, after year 4, Bank of Canada decided to raise the benchmark interest rate to fight the inflation. The yield curve is flat at 6.50% after year 4. What is the realized compound yield for an investor investing in Bond C with a 4-year holding period? (10 Marks) (Assuming the investor can buy the bond at the current price as you calculated in question i) and will liquidate the position at the end of year 4.)