Answered step by step

Verified Expert Solution

Question

1 Approved Answer

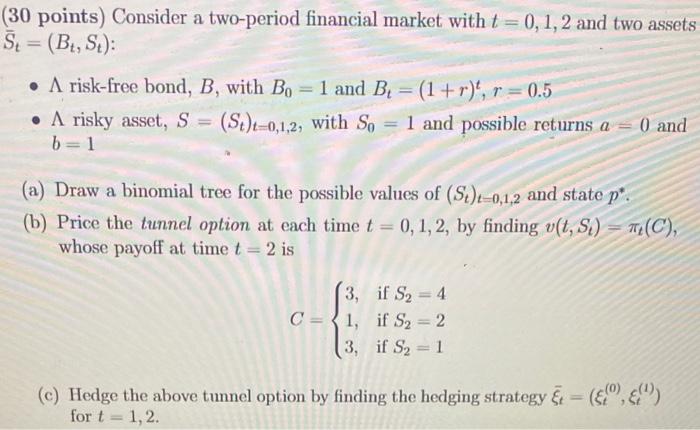

(30 points) Consider a two-period financial market with t=0,1,2 and two assets St=(Bt,St) - risk-free bond, B, with B0=1 and Bt=(1+r)t,r=0.5 - risky asset, S=(St)t=0,1,2,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Portfolio Performance Measurement And Benchmarking

Authors: Jon Christopherson, David Carino, Wayne Ferson

1st Edition

0071496653, 978-0071496650