Answered step by step

Verified Expert Solution

Question

1 Approved Answer

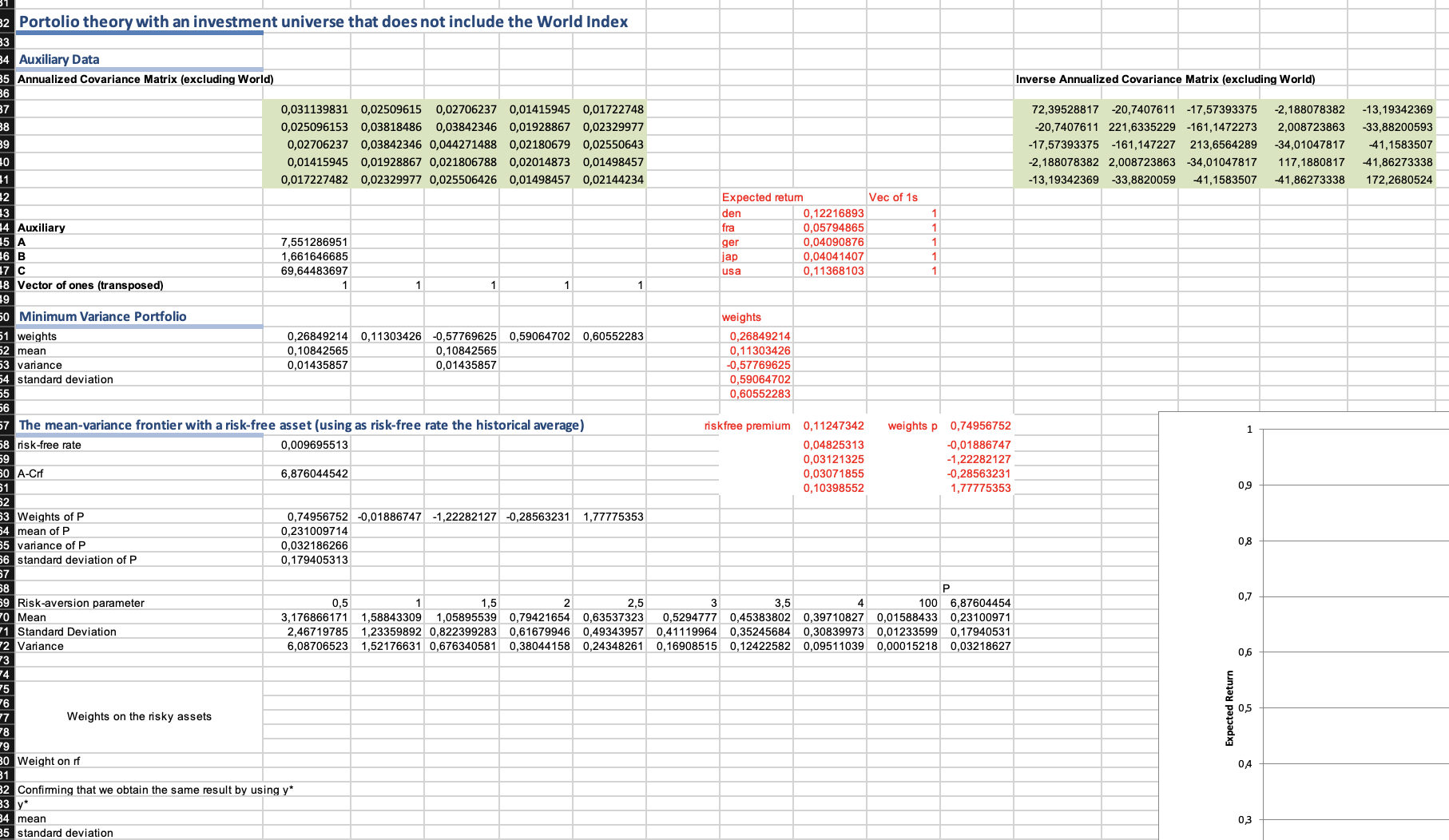

32 Portolio theory with an investment universe that does not include the World Index 83 34 Auxiliary Data 35 Annualized Covariance Matrix (excluding World)

32 Portolio theory with an investment universe that does not include the World Index 83 34 Auxiliary Data 35 Annualized Covariance Matrix (excluding World) 36 37 38 89 40 41 42 43 0,031139831 0,02509615 0,02706237 0,01415945 0,01722748 0,025096153 0,03818486 0,03842346 0,01928867 0,02329977 0,02706237 0,03842346 0,044271488 0,02180679 0,02550643 0,01415945 0,01928867 0,021806788 0,02014873 0,01498457 0,017227482 0,02329977 0,025506426 0,01498457 0,02144234 44 Auxiliary 45 A 46 B 47 C Expected return Vec of 1s den 0,12216893 1 fra 0,05794865 1 7,551286951 ger 0,04090876 1 1,661646685 jap 0,04041407 1 69,64483697 usa 0,11368103 1 1 1 1 1 1 48 Vector of ones (transposed) 49 50 Minimum Variance Portfolio 51 weights 52 mean 53 variance 0,26849214 0,11303426 -0,57769625 0,59064702 0,60552283 0,10842565 0,01435857 0,10842565 0,01435857 54 standard deviation 55 56 57 The mean-variance frontier with a risk-free asset (using as risk-free rate the historical average) 58 risk-free rate 59 50 A-Crf 0,009695513 6,876044542 51 52 63 Weights of P 64 mean of P 65 variance of P 0,032186266 66 standard deviation of P 0,179405313 57 58 69 Risk-aversion parameter 70 Mean 71 Standard Deviation 72 Variance 73 74 75 76 77 Weights on the risky assets. 78 79 0,74956752 -0,01886747 -1,22282127 -0,28563231 1,77775353 0,231009714 weights 0,26849214 0,11303426 -0,57769625 0,59064702 0,60552283 Inverse Annualized Covariance Matrix (excluding World) 72,39528817 -20,7407611 -17,57393375 -2,188078382 -13,19342369 -20,7407611 221,6335229 -161,1472273 2,008723863 -33,88200593 -34,01047817 -41,1583507 -41,86273338 -17,57393375 -161,147227 213,6564289 -2,188078382 2,008723863 -34,01047817 117,1880817 -13,19342369 -33,8820059 -41,1583507 -41,86273338 172,2680524 riskfree premium 0,11247342 weights p 0,04825313 0,03121325 0,03071855 0,74956752 -0,01886747 -1,22282127 -0,28563231 1 0,10398552 1,77775353 09 08 0,7 40 0,5 1 1,5 2 2.5 3 3,5 3,176866171 2,46719785 6,08706523 1,58843309 1,05895539 1,23359892 0,822399283 0,79421654 0,61679946 0,63537323 0,49343957 6,87604454 0,5294777 0,45383802 0,39710827 0,01588433 0,23100971 0,41119964 0,35245684 0,30839973 0,01233599 0,17940531 4 100 1,52176631 0,676340581 0,38044158 0,24348261 0,16908515 0,12422582 0,09511039 0,00015218 0,03218627 0,6 30 Weight on rf 31 32 Confirming that we obtain the same result by using y* 83 y* 34 mean 35 standard deviation Expected Return 0,5 04 0,3

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

9th Edition

73530700, 978-0073530703