Answered step by step

Verified Expert Solution

Question

1 Approved Answer

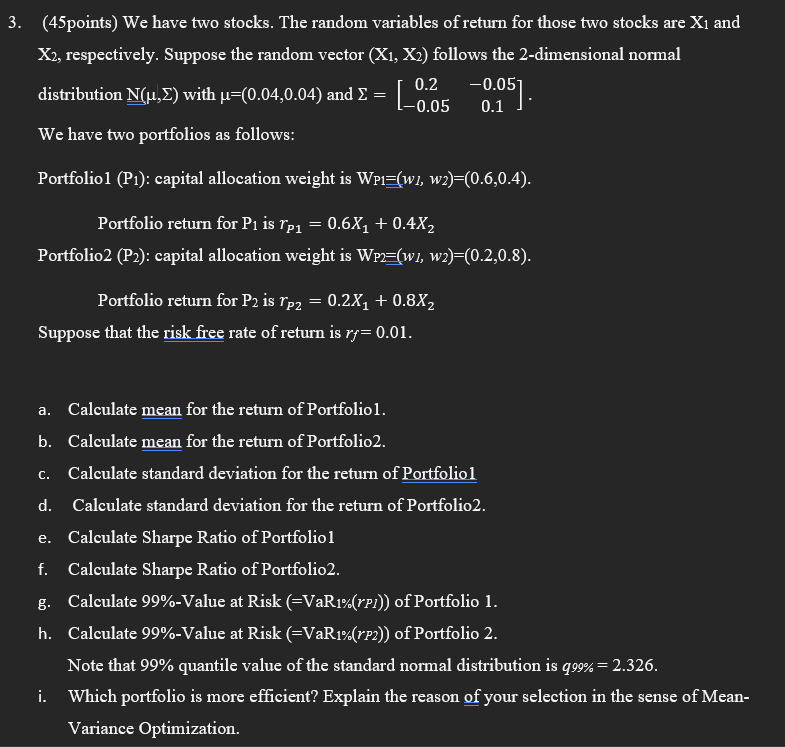

( 4 5 points ) We have two stocks. The random variables of return for those two stocks are x 1 and x 2 ,

points We have two stocks. The random variables of return for those two stocks are and

respectively. Suppose the random vector follows the dimensional normal

distribution with and

We have two portfolios as follows:

Portfolio : capital allocation weight is

Portfolio return for is

Portfolio : capital allocation weight is

Portfolio return for is

Suppose that the risk free rate of return is

a Calculate mean for the return of Portfolio

b Calculate mean for the return of Portfolio

c Calculate standard deviation for the return of Portfoliol

d Calculate standard deviation for the return of Portfolio

e Calculate Sharpe Ratio of Portfolio

f Calculate Sharpe Ratio of Portfolio

g Calculate Value at Risk of Portfolio

h Calculate Value at Risk VaR of Portfolio

Note that quantile value of the standard normal distribution is

i Which portfolio is more efficient? Explain the reason of your selection in the sense of Mean

Variance Optimization.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Futures And Other Derivatives

Authors: John C. Hull

3rd Edition

0131864793, 9780306457555