Answered step by step

Verified Expert Solution

Question

1 Approved Answer

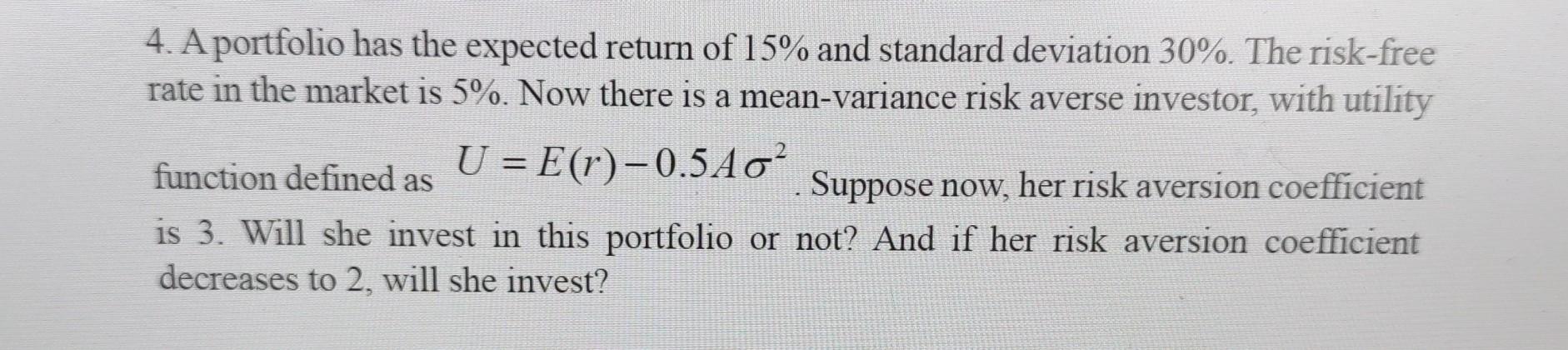

4. A portfolio has the expected return of 15% and standard deviation 30%. The risk-free rate in the market is 5%. Now there is a

4. A portfolio has the expected return of 15% and standard deviation 30%. The risk-free rate in the market is 5%. Now there is a mean-variance risk averse investor, with utility function defined as U=E(r)0.5A2. Suppose now, her risk aversion coefficient is 3. Will she invest in this portfolio or not? And if her risk aversion coefficient decreases to 2 , will she invest

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

All About Options

Authors: Thomas McCafferty

3rd Edition

0071484795, 978-0071484794