Answered step by step

Verified Expert Solution

Question

1 Approved Answer

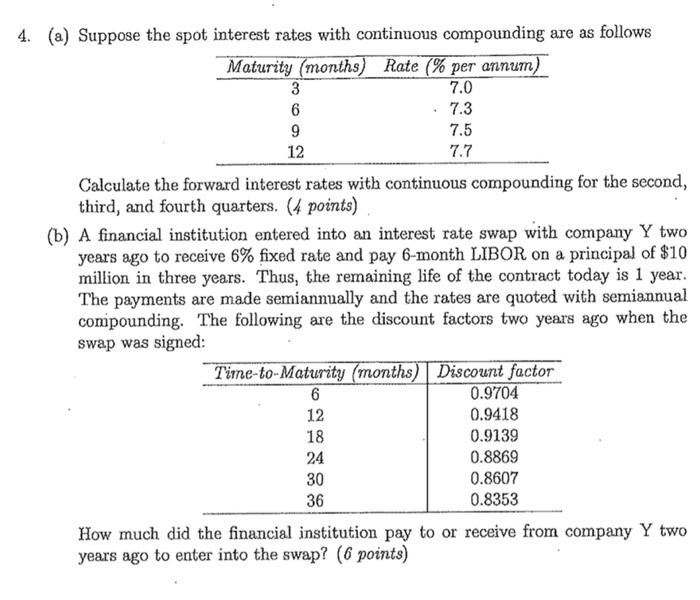

4. (a) Suppose the spot interest rates with continuous compounding are as follows Maturity (months) Rate (% per annum) 3 6 9 12 7.0

4. (a) Suppose the spot interest rates with continuous compounding are as follows Maturity (months) Rate (% per annum) 3 6 9 12 7.0 .. 7.3 7.5 7.7 Calculate the forward interest rates with continuous compounding for the second, third, and fourth quarters. (4 points). (b) A financial institution entered into an interest rate swap with company Y two years ago to receive 6% fixed rate and pay 6-month LIBOR on a principal of $10 million in three years. Thus, the remaining life of the contract today is 1 year. The payments are made semiannually and the rates are quoted with semiannual compounding. The following are the discount factors two years ago when the swap was signed: Time-to-Maturity (months) Discount factor 6 12 18 24 30 36 0.9704 0.9418 0.9139 0.8869 0.8607 0.8353 How much did the financial institution pay to or receive from company Y two years ago to enter into the swap? (6 points)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

College Accounting Chapters 1-27

Authors: James A. Heintz, Robert W. Parry

22nd Edition

130566616X, 978-1305666160