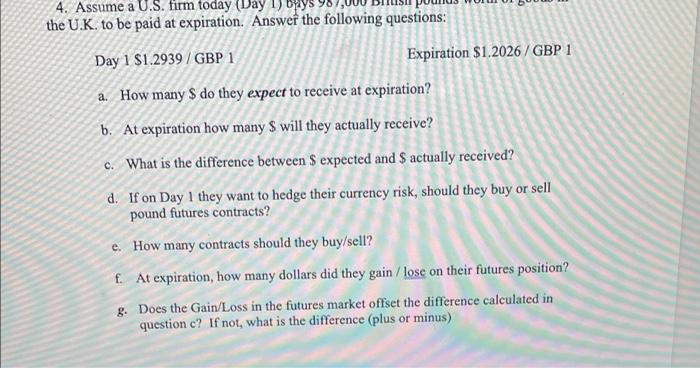

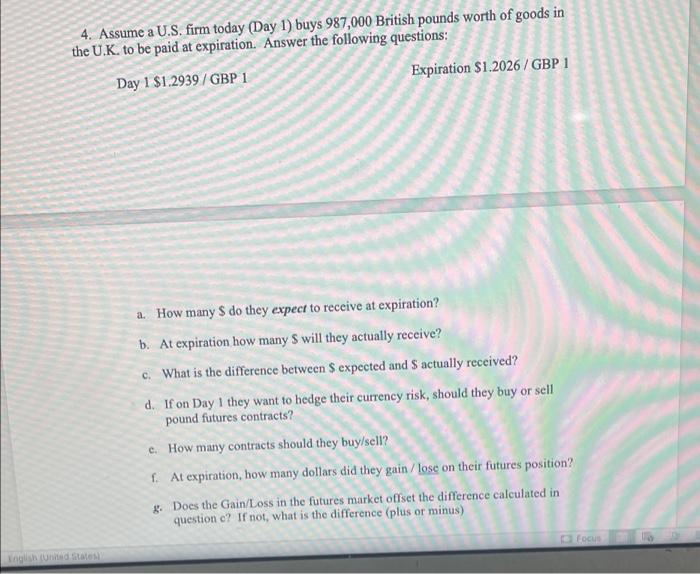

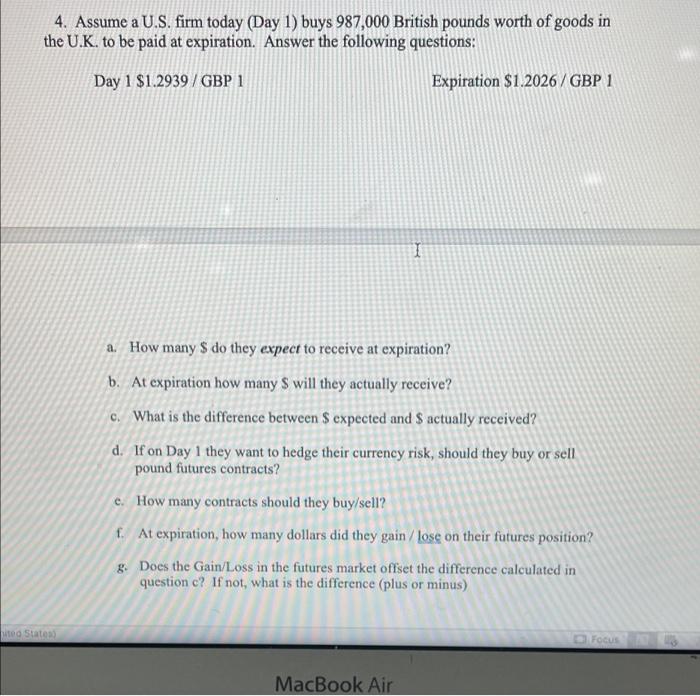

4. Assume a U.S. firm today (Day the U.K. to be paid at expiration. Answer the following questions: Day 1 $1.2939/GBP 1 a. How many S do they expect to receive at expiration? b. At expiration how many S will they actually receive? c. What is the difference between $ expected and $ actually received? d. If on Day 1 they want to hedge their currency risk, should they buy or sell pound futures contracts? e. How many contracts should they buy/sell? f. At expiration, how many dollars did they gain / lose on their futures position? g. Does the Gain/Loss in the futures market offset the difference calculated in question c? If not, what is the difference (plus or minus) Expiration $1.2026/GBP 1 4. Assume a U.S. firm today (Day 1) buys 987,000 British pounds worth of goods in the U.K. to be paid at expiration. Answer the following questions: Day 1 $1.2939/GBP 1 Expiration $1.2026/GBP 1 a. How many $ do they expect to receive at expiration? b. At expiration how many S will they actually receive? c. What is the difference between $ expected and S actually received? d. If on Day 1 they want to hedge their currency risk, should they buy or sell pound futures contracts? c. How many contracts should they buy/sell? f. At expiration, how many dollars did they gain/lose on their futures position? g. Does the Gain/Loss in the futures market offset the difference calculated in question c? If not, what is the difference (plus or minus) Focus 4. Assume a U.S. firm today (Day 1) buys 987,000 British pounds worth of goods in the U.K. to be paid at expiration. Answer the following questions: Day 1 $1.2939/GBP 1 Expiration $1.2026/GBP 1 a. How many $ do they expect to receive at expiration? b. At expiration how many $ will they actually receive? c. What is the difference between $ expected and $ actually received? d. If on Day 1 they want to hedge their currency risk, should they buy or sell pound futures contracts? e. How many contracts should they buy/sell? f. At expiration, how many dollars did they gain / lose on their futures position? g. Does the Gain/Loss in the futures market offset the difference calculated in question c? If not, what is the difference (plus or minus) MacBook Air ited States) FOCUS 4. Assume a U.S. firm today (Day the U.K. to be paid at expiration. Answer the following questions: Day 1 $1.2939/GBP 1 a. How many S do they expect to receive at expiration? b. At expiration how many S will they actually receive? c. What is the difference between $ expected and $ actually received? d. If on Day 1 they want to hedge their currency risk, should they buy or sell pound futures contracts? e. How many contracts should they buy/sell? f. At expiration, how many dollars did they gain / lose on their futures position? g. Does the Gain/Loss in the futures market offset the difference calculated in question c? If not, what is the difference (plus or minus) Expiration $1.2026/GBP 1 4. Assume a U.S. firm today (Day 1) buys 987,000 British pounds worth of goods in the U.K. to be paid at expiration. Answer the following questions: Day 1 $1.2939/GBP 1 Expiration $1.2026/GBP 1 a. How many $ do they expect to receive at expiration? b. At expiration how many S will they actually receive? c. What is the difference between $ expected and S actually received? d. If on Day 1 they want to hedge their currency risk, should they buy or sell pound futures contracts? c. How many contracts should they buy/sell? f. At expiration, how many dollars did they gain/lose on their futures position? g. Does the Gain/Loss in the futures market offset the difference calculated in question c? If not, what is the difference (plus or minus) Focus 4. Assume a U.S. firm today (Day 1) buys 987,000 British pounds worth of goods in the U.K. to be paid at expiration. Answer the following questions: Day 1 $1.2939/GBP 1 Expiration $1.2026/GBP 1 a. How many $ do they expect to receive at expiration? b. At expiration how many $ will they actually receive? c. What is the difference between $ expected and $ actually received? d. If on Day 1 they want to hedge their currency risk, should they buy or sell pound futures contracts? e. How many contracts should they buy/sell? f. At expiration, how many dollars did they gain / lose on their futures position? g. Does the Gain/Loss in the futures market offset the difference calculated in question c? If not, what is the difference (plus or minus) MacBook Air ited States) FOCUS