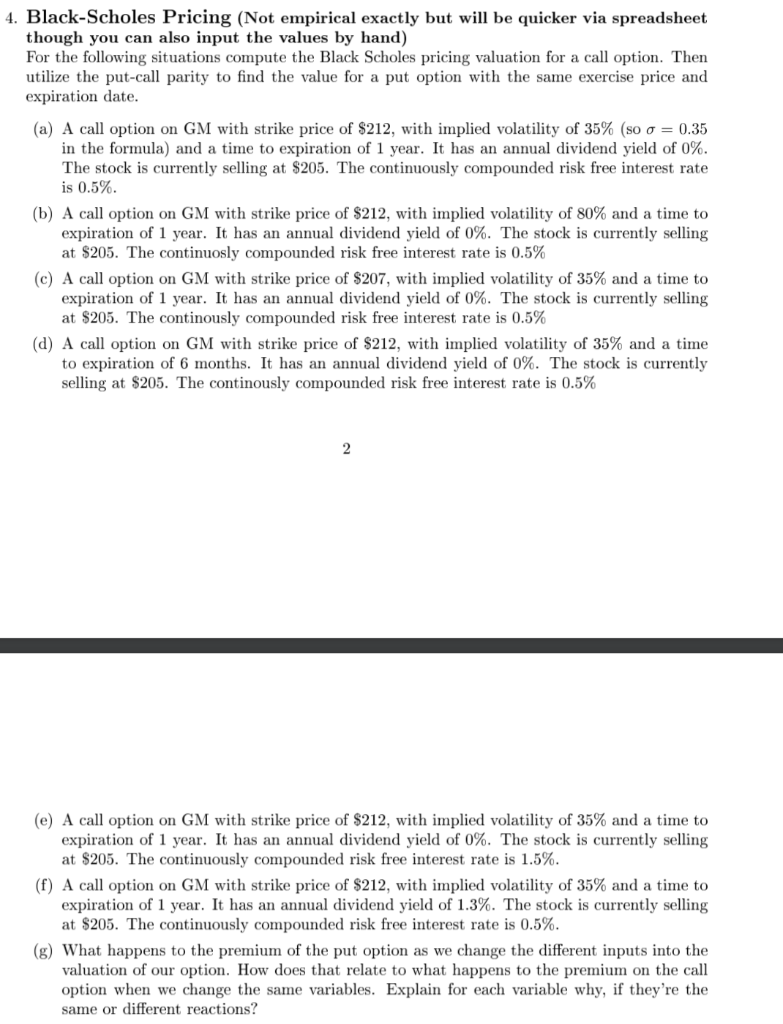

4. Black-Scholes Pricing (Not empirical exactly but will be quicker via spreadsheet though you can also input the values by hand) For the following situations compute the Black Scholes pricing valuation for a call option. Then utilize the put-call parity to find the value for a put option with the same exercise price and expiration date. (a) A call option on GM with strike price of $212, with implied volatility of 35% (so o = 0.35 in the formula) and a time to expiration of 1 year. It has an annual dividend yield of 0%. The stock is currently selling at $205. The continuously compounded risk free interest rate is 0.5% (b) A call option on GM with strike price of $212, with implied volatility of 80% and a time to expiration of 1 year. It has an annual dividend yield of 0%. The stock is currently selling at $205. The continuosly compounded risk free interest rate is 0.5% (c) A call option on GM with strike price of $207, with implied volatility of 35% and a time to expiration of 1 year. It has an annual dividend yield of 0%. The stock is currently selling at $205. The continously compounded risk free interest rate is 0.5% (d) A call option on GM with strike price of $212, with implied volatility of 35% and a time to expiration of 6 months. It has an annual dividend yield of 0%. The stock is currently selling at $205. The continously compounded risk free interest rate is 0.5% (e) A call option on GM with strike price of $212, with implied volatility of 35% and a time to expiration of 1 year. It has an annual dividend yield of 0%. The stock is currently selling at $205. The continuously compounded risk free interest rate is 1.5%. (f) A call option on GM with strike price of $212, with implied volatility of 35% and a time to expiration of 1 year. It has an annual dividend yield of 1.3%. The stock is currently selling at $205. The continuously compounded risk free interest rate is 0.5%. (g) What happens to the premium of the put option as we change the different inputs into the valuation of our option. How does that relate to what happens to the premium on the call option when we change the same variables. Explain for each variable why, if they're the same or different reactions? 4. Black-Scholes Pricing (Not empirical exactly but will be quicker via spreadsheet though you can also input the values by hand) For the following situations compute the Black Scholes pricing valuation for a call option. Then utilize the put-call parity to find the value for a put option with the same exercise price and expiration date. (a) A call option on GM with strike price of $212, with implied volatility of 35% (so o = 0.35 in the formula) and a time to expiration of 1 year. It has an annual dividend yield of 0%. The stock is currently selling at $205. The continuously compounded risk free interest rate is 0.5% (b) A call option on GM with strike price of $212, with implied volatility of 80% and a time to expiration of 1 year. It has an annual dividend yield of 0%. The stock is currently selling at $205. The continuosly compounded risk free interest rate is 0.5% (c) A call option on GM with strike price of $207, with implied volatility of 35% and a time to expiration of 1 year. It has an annual dividend yield of 0%. The stock is currently selling at $205. The continously compounded risk free interest rate is 0.5% (d) A call option on GM with strike price of $212, with implied volatility of 35% and a time to expiration of 6 months. It has an annual dividend yield of 0%. The stock is currently selling at $205. The continously compounded risk free interest rate is 0.5% (e) A call option on GM with strike price of $212, with implied volatility of 35% and a time to expiration of 1 year. It has an annual dividend yield of 0%. The stock is currently selling at $205. The continuously compounded risk free interest rate is 1.5%. (f) A call option on GM with strike price of $212, with implied volatility of 35% and a time to expiration of 1 year. It has an annual dividend yield of 1.3%. The stock is currently selling at $205. The continuously compounded risk free interest rate is 0.5%. (g) What happens to the premium of the put option as we change the different inputs into the valuation of our option. How does that relate to what happens to the premium on the call option when we change the same variables. Explain for each variable why, if they're the same or different reactions