Answered step by step

Verified Expert Solution

Question

1 Approved Answer

4. Both Bond A and Bond B have 6% coupons, make semiannual payments, and are priced at par value. Bond A has three years to

4. Both Bond A and Bond B have 6% coupons, make semiannual payments, and are priced at par value. Bond A has three years to maturity, whereas Bond B has 20 years to maturity. If the interest rates suddenly rise by 2 percent point to 8%, what is the percentage change in the price of Bond A and Bond B? If rates were to suddenly fall by 2 percent points to 4% instead, what would be the percentage change in the price of Bond A and Bond B then?

QUESTION #4

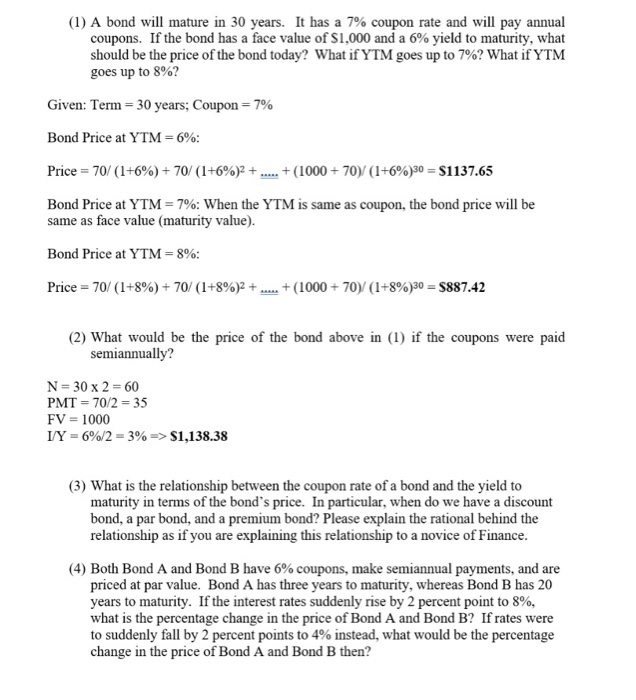

(1) A bond will mature in 30 years. It has a 7% coupon rate and will pay annual coupons. If the bond has a face value of $1,000 and a 6% yield to maturity, what should be the price of the bond today? What if YTM goes up to 7%? What if YTM goes up to 8%? Given: Term = 30 years; Coupon = 7% Bond Price at YTM=6%: Price = 70/(1+6%) +70/(1+6%)2 + ..... + (1000 + 70)/(1+6%)30 = $1137.65 Bond Price at YTM = 7%: When the YTM is same as coupon, the bond price will be same as face value (maturity value). Bond Price at YTM -8%: Price = 70/ (1+8%) +70/(1+8%)2 + ... + (1000 + 70)/(1+8%)30 = $887.42 (2) What would be the price of the bond above in (1) if the coupons were paid semiannually? N= 30 x 2 = 60 PMT = 70/2 = 35 FV = 1000 I/Y = 6%/2 = 3% => $1,138.38 (3) What is the relationship between the coupon rate of a bond and the yield to maturity in terms of the bond's price. In particular, when do we have a discount bond, a par bond, and a premium bond? Please explain the rational behind the relationship as if you are explaining this relationship to a novice of Finance. (4) Both Bond A and Bond B have 6% coupons, make semiannual payments, and are priced at par value. Bond A has three years to maturity, whereas Bond B has 20 years to maturity. If the interest rates suddenly rise by 2 percent point to 8%, what is the percentage change in the price of Bond A and Bond B? If rates were to suddenly fall by 2 percent points to 4% instead, what would be the percentage change in the price of Bond A and Bond B then Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Supply Chain Finance Solutions

Authors: Erik Hofmann, Oliver Belin

1st Edition

3642175651, 978-3642175657