Answered step by step

Verified Expert Solution

Question

1 Approved Answer

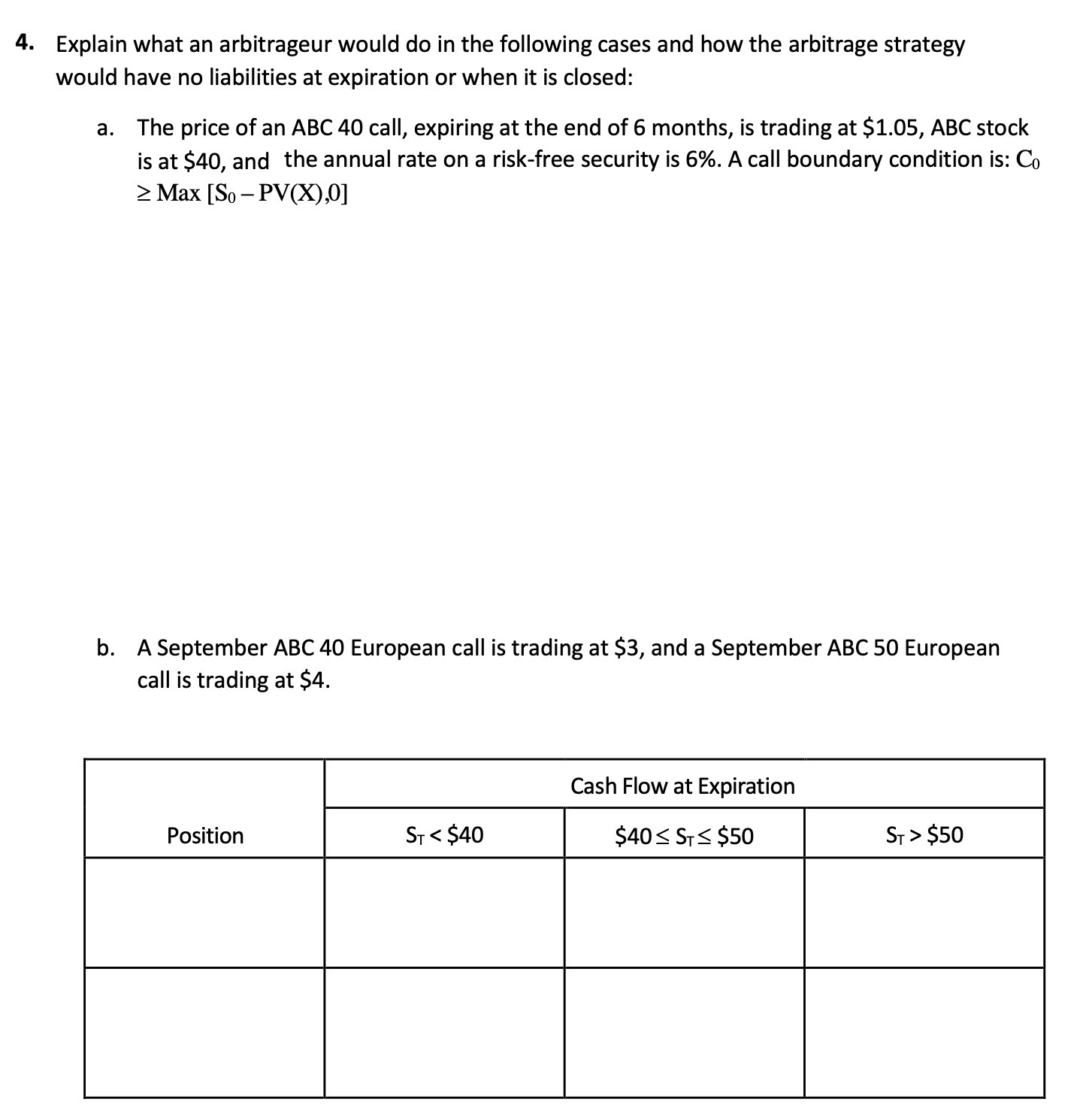

4. Explain what an arbitrageur would do in the following cases and how the arbitrage strategy would have no liabilities at expiration or when

4. Explain what an arbitrageur would do in the following cases and how the arbitrage strategy would have no liabilities at expiration or when it is closed: a. The price of an ABC 40 call, expiring at the end of 6 months, is trading at $1.05, ABC stock is at $40, and the annual rate on a risk-free security is 6%. A call boundary condition is: Co > Max [So - PV(X),0] b. A September ABC 40 European call is trading at $3, and a September ABC 50 European call is trading at $4. Cash Flow at Expiration Position ST < $40 $40 ST $50 ST > $50

Step by Step Solution

★★★★★

3.47 Rating (157 Votes )

There are 3 Steps involved in it

Step: 1

a In this case an arbitrageur would take advantage of the mispricing in the ABC 40 call options The ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Accounting

Authors: Joe Hoyle, Thomas Schaefer, Timothy Doupnik

10th edition

0-07-794127-6, 978-0-07-79412, 978-0077431808