Answered step by step

Verified Expert Solution

Question

1 Approved Answer

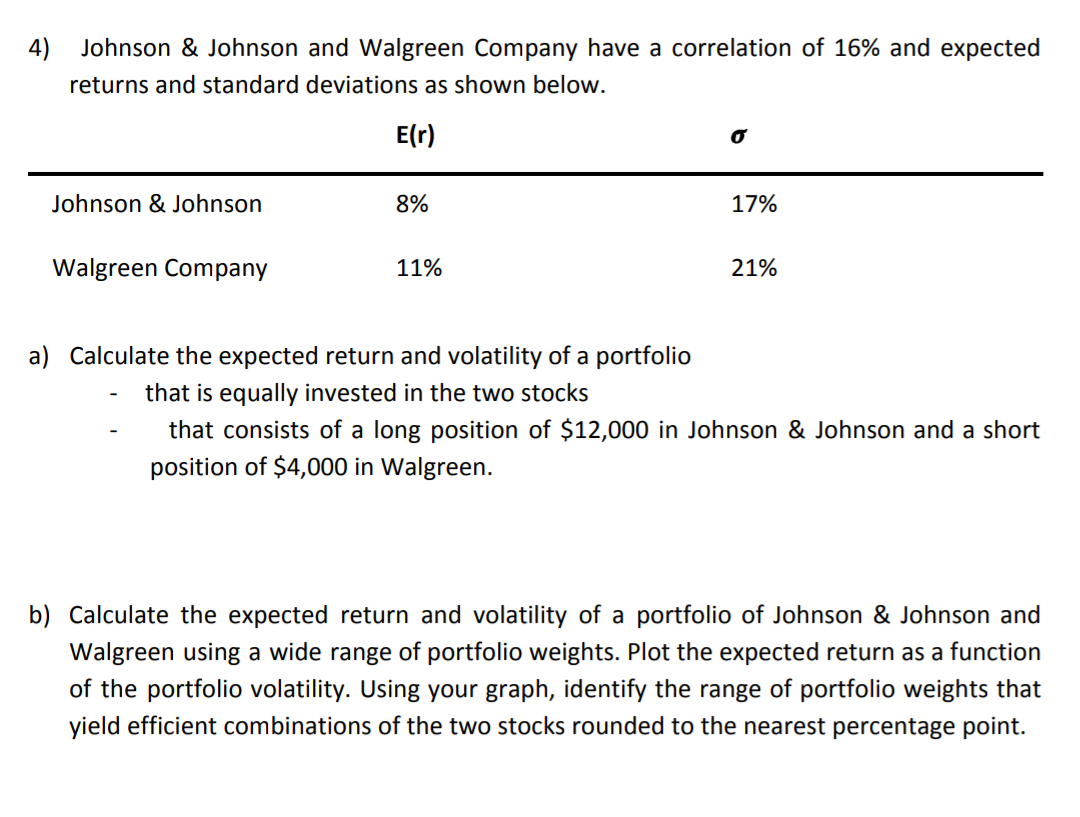

4) Johnson & Johnson and Walgreen Company have a correlation of 16% and expected returns and standard deviations as shown below. E(r) o Johnson &

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Economic Growth In Latin America And The Impact Of The Global Financial Crisis

Authors: Mauricio Garita

1st Edition

1522549811,152254982X