Answered step by step

Verified Expert Solution

Question

1 Approved Answer

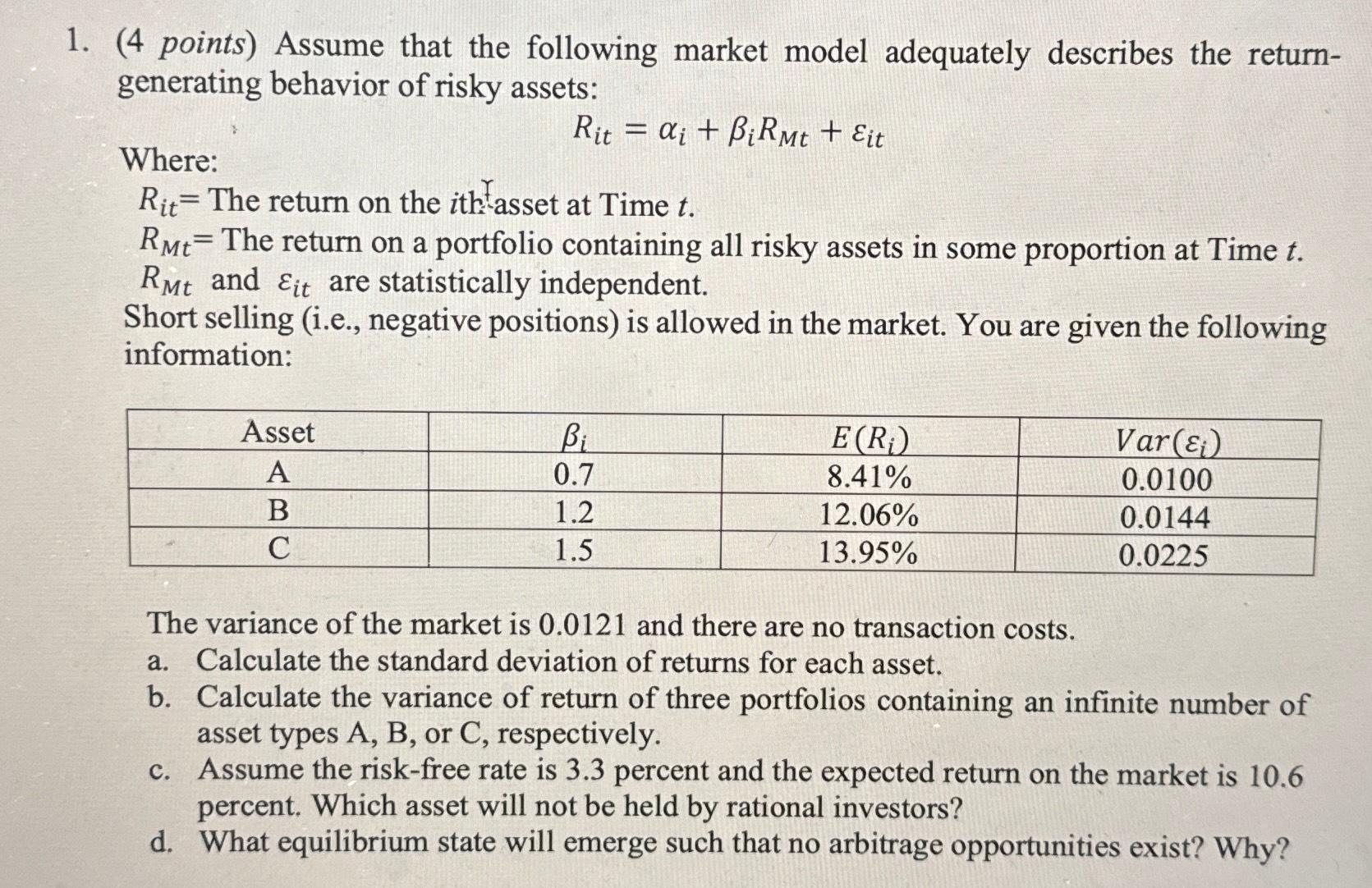

( 4 points ) Assume that the following market model adequately describes the returngenerating behavior of risky assets: Where: R i t = i +

points Assume that the following market model adequately describes the returngenerating behavior of risky assets:

Where:

The return on the i thtasset at Time

The return on a portfolio containing all risky assets in some proportion at Time and are statistically independent.

Short selling ie negative positions is allowed in the market. You are given the following information:

tableAssetVar

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essential Personal Finance A Practical Guide For Students

Authors: Lien Luu, Jonquil Lowe, Jason Butler, Tony Byrne

1st Edition

1138692956, 978-1138692954