#4 The black lines on the graph show the unit cost curves of a representative rm in a constant cost competitive industry. The black supply

#4

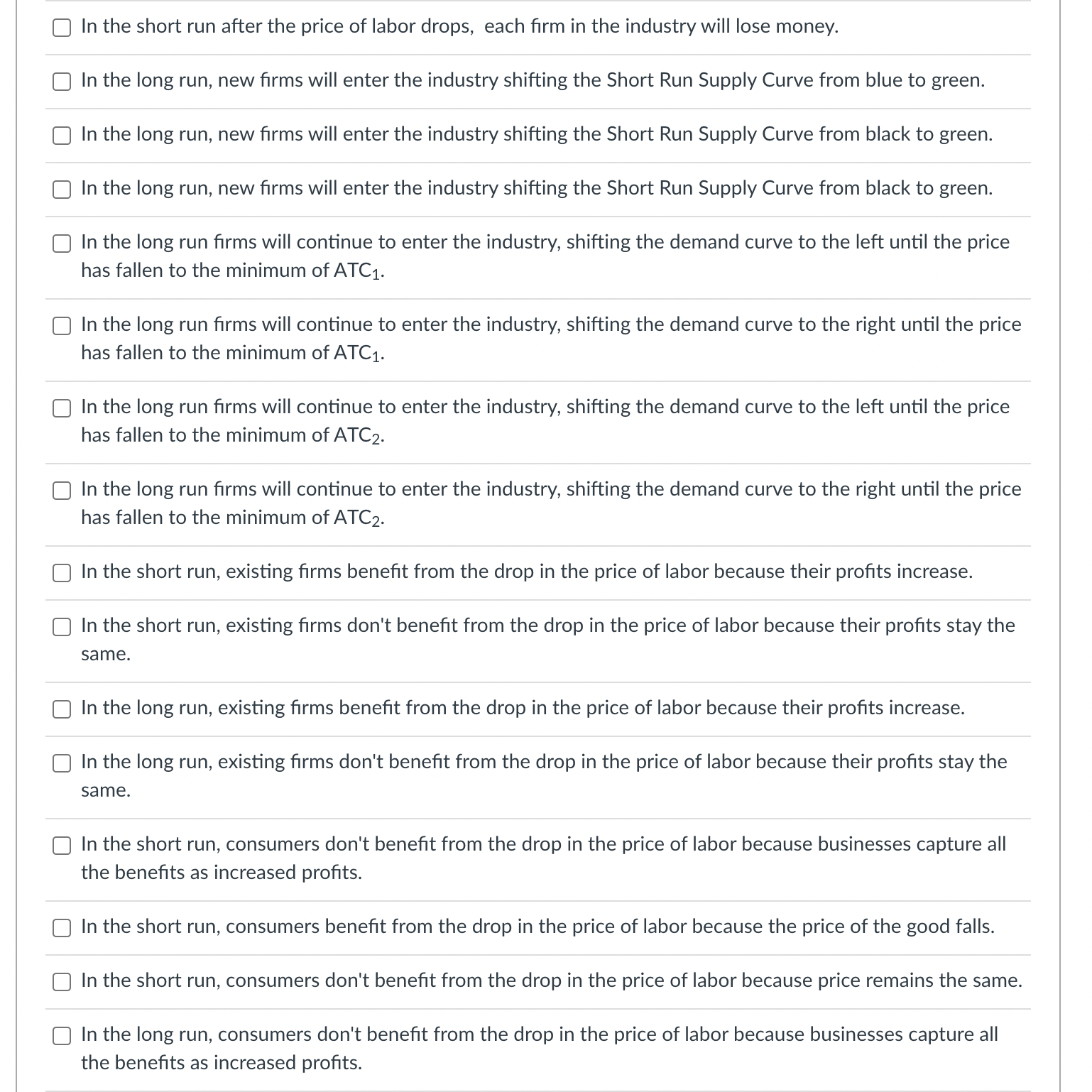

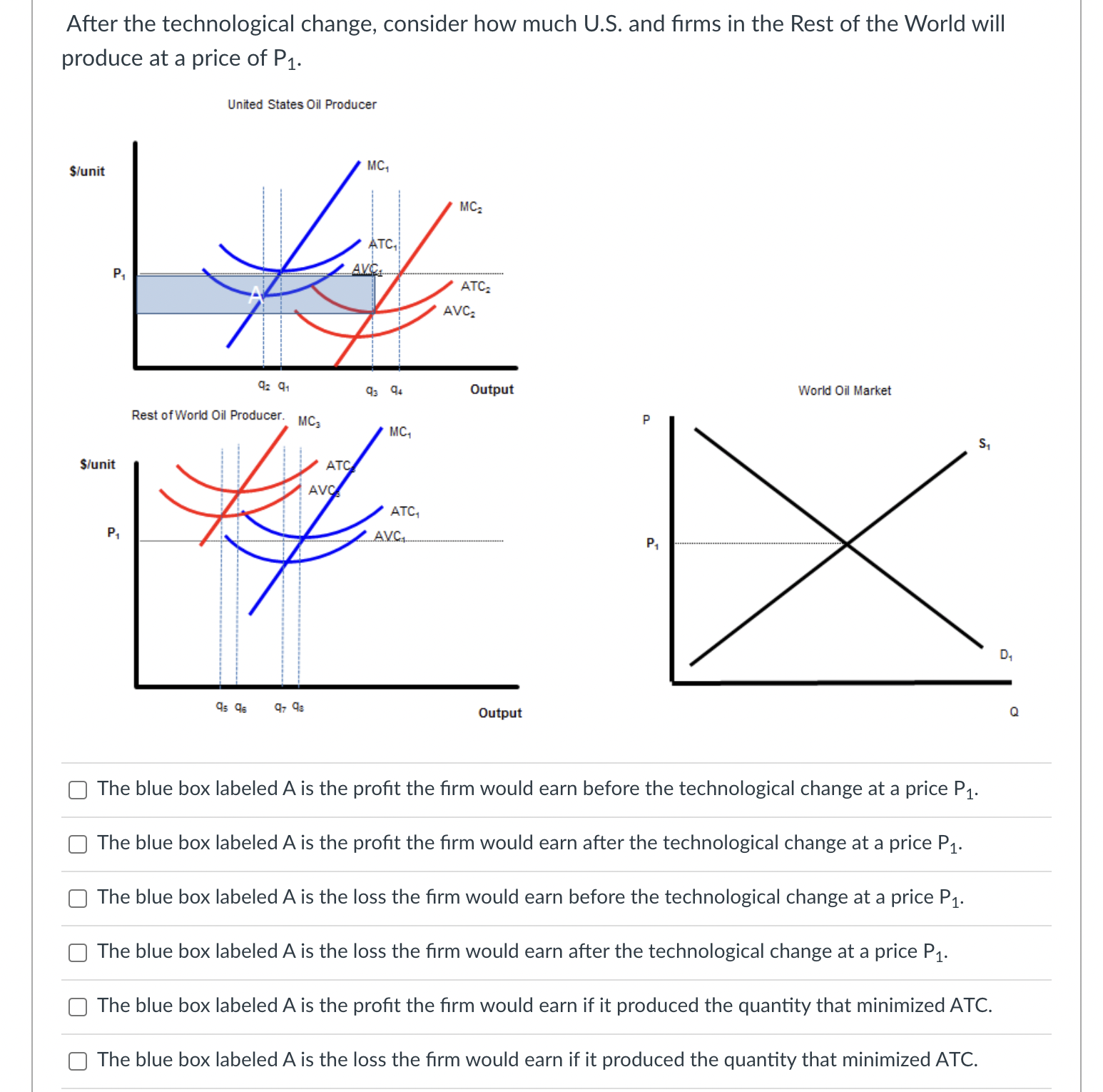

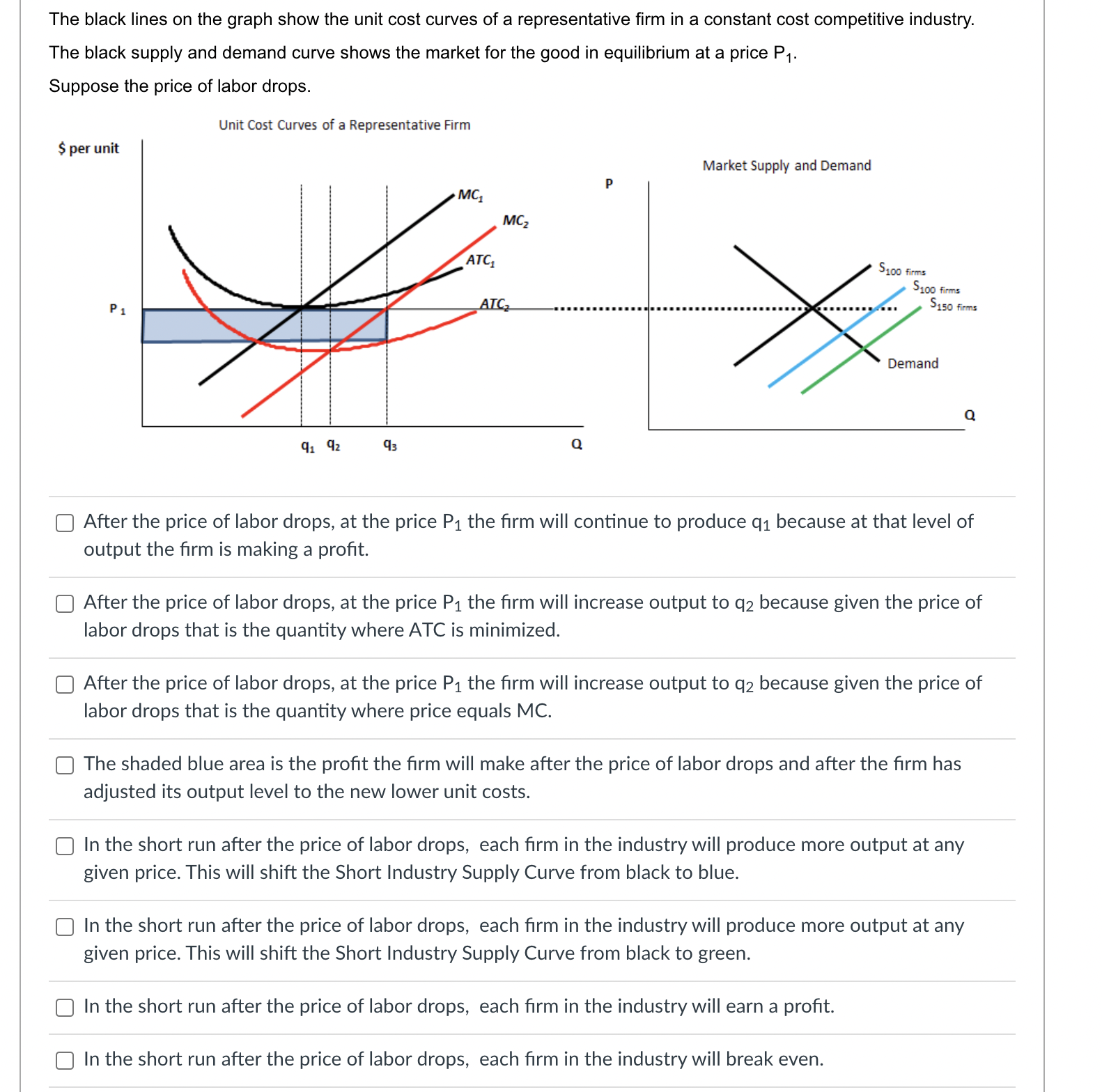

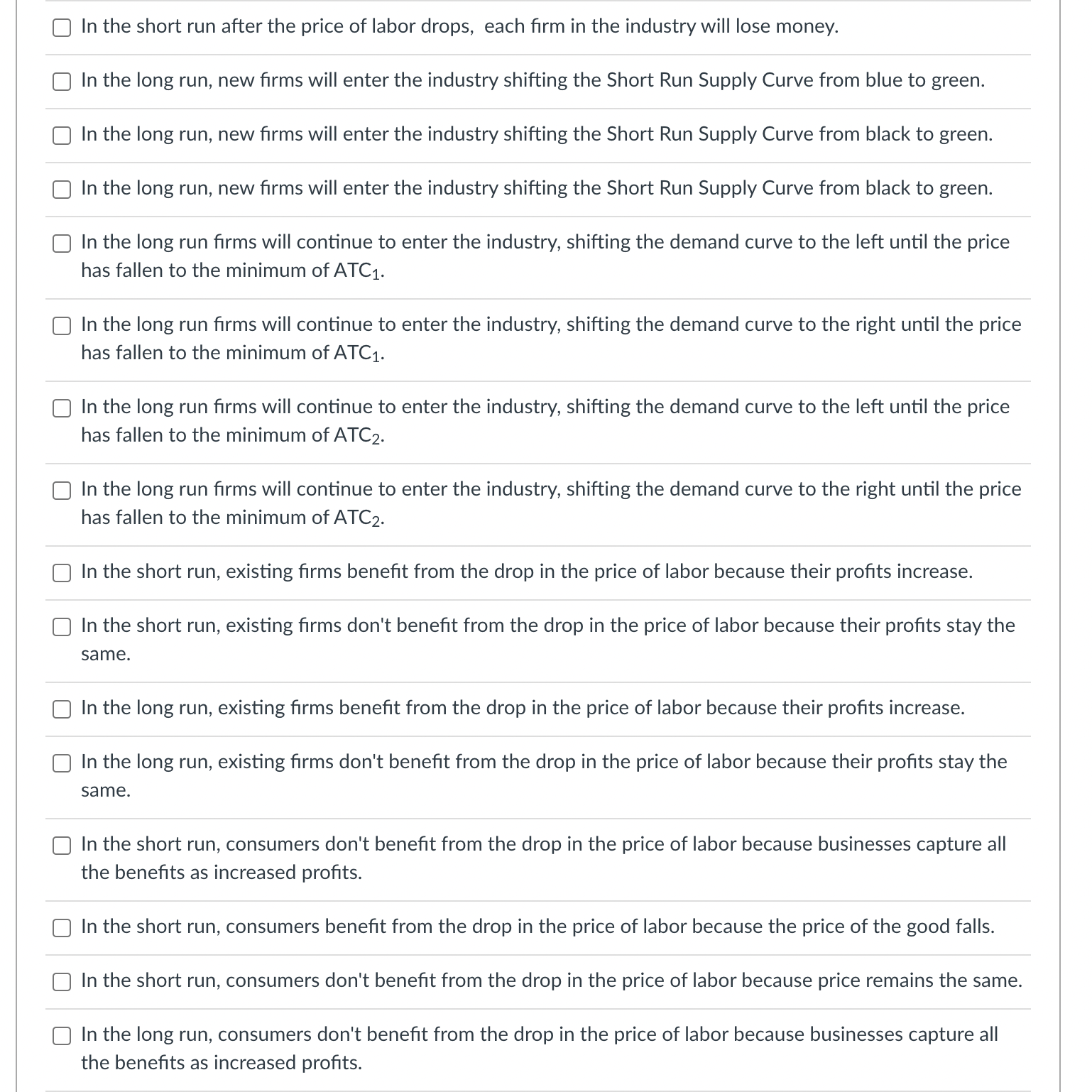

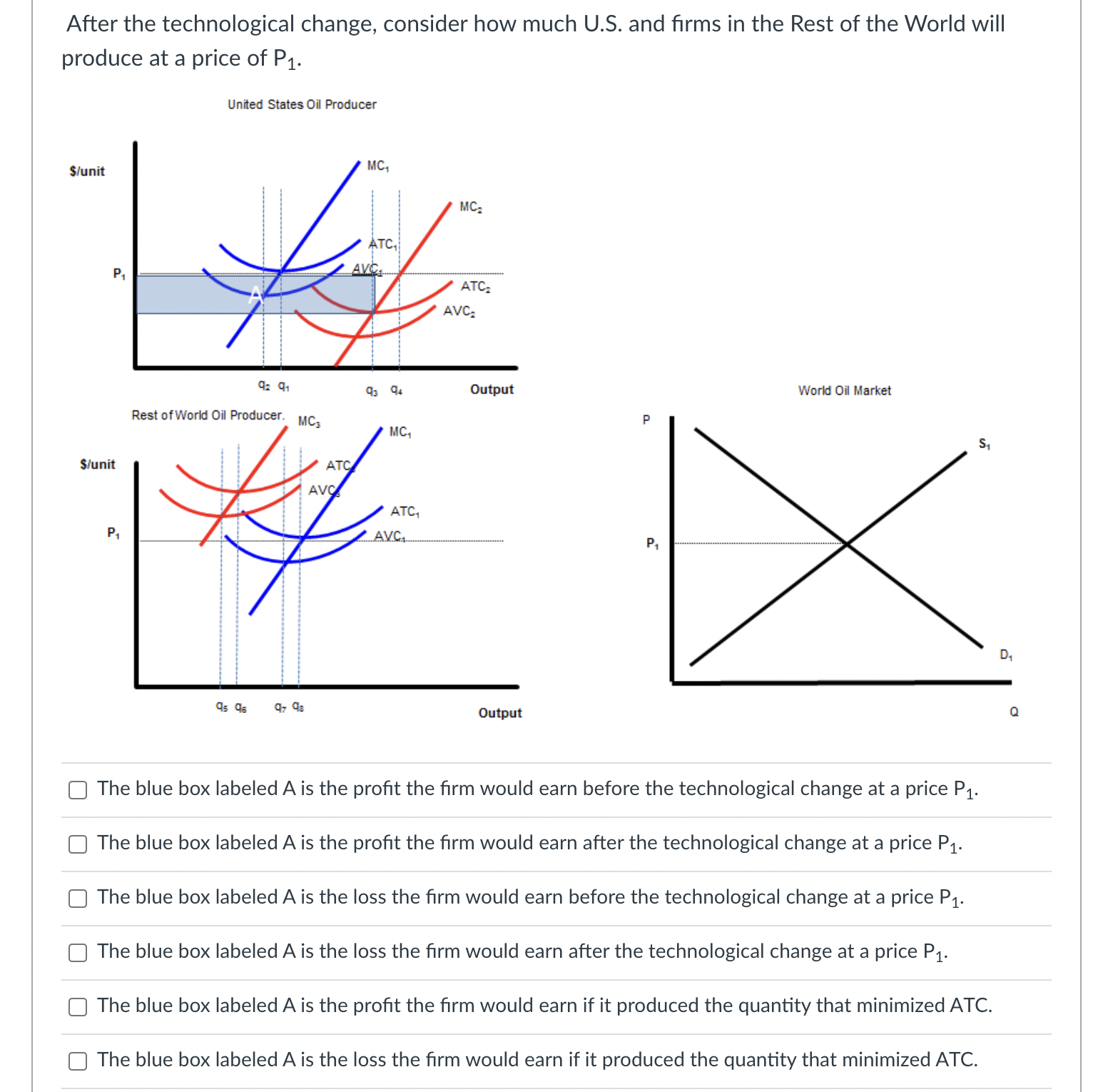

The black lines on the graph show the unit cost curves of a representative rm in a constant cost competitive industry. The black supply and demand curve shows the market for the good in equilibrium at a price P1. Suppose the price of labor drops. Unit Cost Curves of a Representative Firm S per unit Market Suppty and Demand C] After the price of labor drops, at the price P1 the rm will continue to produce q1 because at that level of output the rm is making a prot. C] After the price of labor drops, at the price P1 the rm will increase output to Cu because given the price of labor drops that is the quantity where ATC is minimized. C] After the price of labor drops, at the price P1 the rm will increase output to 12 because given the price of labor drops that is the quantity where price equals MC. [3 The shaded blue area is the prot the rm will make after the price of labor drops and after the rm has adjusted its output level to the new lower unit costs. C] In the short run after the price of labor drops, each rm in the industry will produce more output at any given price. This will shift the Short industry Supply Curve from black to blue. [3 In the short run after the price of labor drops, each rm in the industry will produce more output at any given price. This will shift the Short Industry Supply Curve from black to green. C] In the short run after the price of labor drops, each rm in the industry will earn a prot. [3 In the short run after the price of labor drops, each rm in the industry will break even. O In the short run after the price of labor drops, each firm in the industry will lose money. O In the long run, new firms will enter the industry shifting the Short Run Supply Curve from blue to green. O In the long run, new firms will enter the industry shifting the Short Run Supply Curve from black to green. In the long run, new firms will enter the industry shifting the Short Run Supply Curve from black to green. In the long run firms will continue to enter the industry, shifting the demand curve to the left until the price has fallen to the minimum of ATC1. O In the long run firms will continue to enter the industry, shifting the demand curve to the right until the price has fallen to the minimum of ATC1. O In the long run firms will continue to enter the industry, shifting the demand curve to the left until the price has fallen to the minimum of ATC2. O In the long run firms will continue to enter the industry, shifting the demand curve to the right until the price has fallen to the minimum of ATC2. O In the short run, existing firms benefit from the drop in the price of labor because their profits increase. O In the short run, existing firms don't benefit from the drop in the price of labor because their profits stay the same. O In the long run, existing firms benefit from the drop in the price of labor because their profits increase. O In the long run, existing firms don't benefit from the drop in the price of labor because their profits stay the same. O) In the short run, consumers don't benefit from the drop in the price of labor because businesses capture all the benefits as increased profits. O In the short run, consumers benefit from the drop in the price of labor because the price of the good falls. O In the short run, consumers don't benefit from the drop in the price of labor because price remains the same. O In the long run, consumers don't benefit from the drop in the price of labor because businesses capture all the benefits as increased profits.O In the long run, consumers benefit from the drop in the price of labor because the price of the good falls. () In the short run, consumers don't benefit from the drop in the price of labor because price remains the same.After the technological change, consider how much US. and rms in the Rest of the World will produce at a price of P1. tinned States Oil Producer Stunit Stunit \"5 q' q?\" Output 0 C The blue box labeled A is the prot the rm would earn before the technological change at a price P1. C The blue box labeled A is the prot the rm would earn after the technological change at a price P1. [: The blue box labeled A is the loss the rm would earn before the technological change at a price P1. C The blue box labeled A is the loss the rm would earn after the technological change at a price P1. C The blue box labeled A is the prot the rm would earn if it produced the quantity that minimized ATC. C The blue box labeled A is the loss the rm would earn if it produced the quantity that minimized ATC. C] If the rm produces the quantity where ATC is minimized it is maximizing prot or minimizing loss. C] If the rm produces the quantity where ATC is minimized it is not maximizing prot or minimizing loss

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance