Answered step by step

Verified Expert Solution

Question

1 Approved Answer

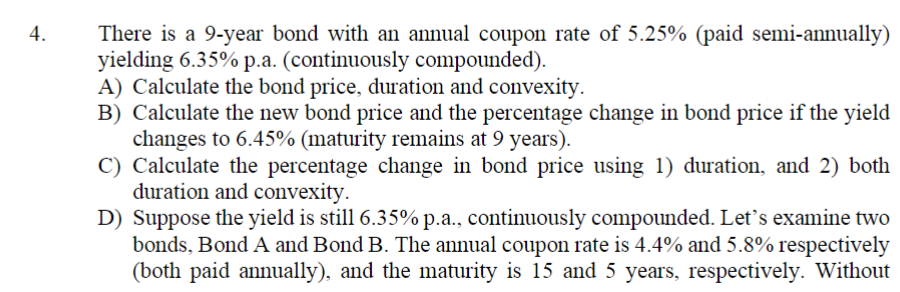

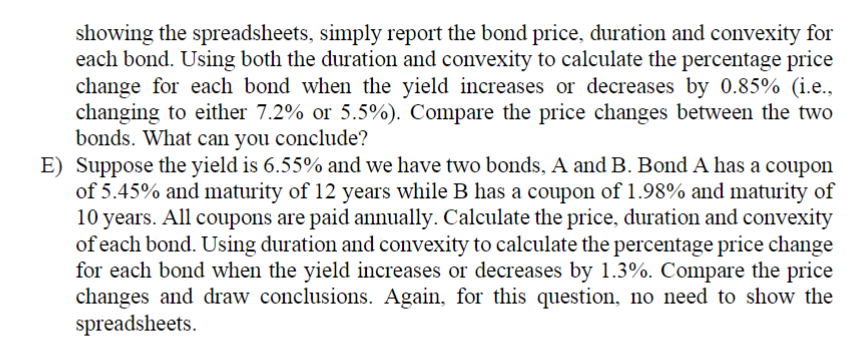

4. There is a 9-year bond with an annual coupon rate of 5.25% (paid semi-annually) yielding 6.35% p.a. (continuously compounded). A) Calculate the bond

4. There is a 9-year bond with an annual coupon rate of 5.25% (paid semi-annually) yielding 6.35% p.a. (continuously compounded). A) Calculate the bond price, duration and convexity. B) Calculate the new bond price and the percentage change in bond price if the yield changes to 6.45% (maturity remains at 9 years). C) Calculate the percentage change in bond price using 1) duration, and 2) both duration and convexity. D) Suppose the yield is still 6.35% p.a., continuously compounded. Let's examine two bonds, Bond A and Bond B. The annual coupon rate is 4.4% and 5.8% respectively (both paid annually), and the maturity is 15 and 5 years, respectively. Without showing the spreadsheets, simply report the bond price, duration and convexity for each bond. Using both the duration and convexity to calculate the percentage price change for each bond when the yield increases or decreases by 0.85% (i.e., changing to either 7.2% or 5.5%). Compare the price changes between the two bonds. What can you conclude? E) Suppose the yield is 6.55% and we have two bonds, A and B. Bond A has a coupon of 5.45% and maturity of 12 years while B has a coupon of 1.98% and maturity of 10 years. All coupons are paid annually. Calculate the price, duration and convexity of each bond. Using duration and convexity to calculate the percentage price change for each bond when the yield increases or decreases by 1.3%. Compare the price changes and draw conclusions. Again, for this question, no need to show the spreadsheets.

Step by Step Solution

★★★★★

3.42 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

Solution A To calculate the bond price duration and convexity we need to use the bond pricing formula duration formula and convexity formula Lets calculate each one step by step Bond Price The bond pr...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investment Analysis and Portfolio Management

Authors: Frank K. Reilly, Keith C. Brown

10th Edition

538482109, 1133711774, 538482389, 9780538482103, 9781133711773, 978-0538482387