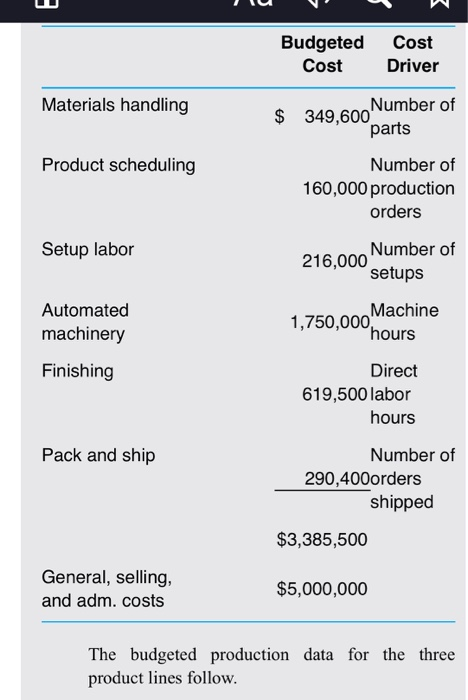

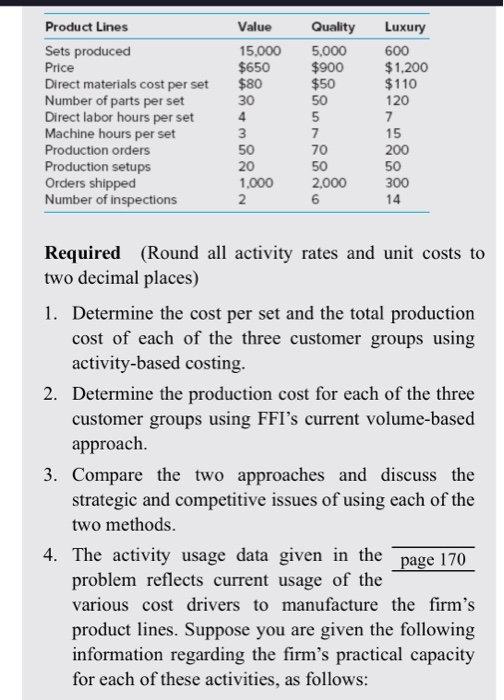

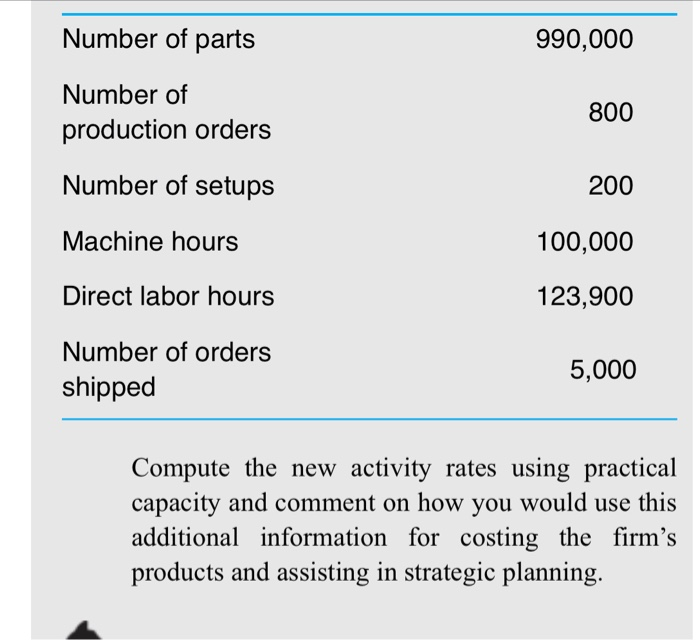

4:33 Aa QD 5-40 Activity-Based Costing; Customer Group Cost Analysis Franklin Furniture Inc. (FFI) manufactures bedroom furniture in sets (a set includes a dresser, two queen-size beds, and one bedside table) for use in motels and hotels. FFI has three customer groups, which it calls the value, quality, and luxury groups. The value products are targeted to low-price motels that are looking for simple furniture, while the luxury furniture is targeted to the very best hotels. The value line is attractive to a variety of hotels and motels that appreciate the combination of quality and value. Currently there has been a small increase in the quality and value lines, and an appreciable increase in demand in the luxury line, reflecting cyclical changes in the marketplace. Luxury hotels are now in more demand for business travel, while a few years ago, the value segment was the most popular for business travelers. FFI wants to be able to respond to the increased demand with increased production but worries about the increased production cost and about price setting as its mix of customers and production change. FFI has used a volume-based overhead allocation rate based on direct labor hours for some time. Direct labor cost is $15 per hour. Budgeted Cost cost Driver Materials handling $ 349,600 Number of 169 Reader Contents Notebook Bookmarks More 0 W Budgeted Cost Cost Driver Materials handling $ 349,600 Number of parts Product scheduling Number of 160,000 production orders Setup labor 216,000 Number of setups Machine Automated machinery 1,750,000 hours Finishing Direct 619,500 labor hours Pack and ship Number of 290,400orders shipped $3,385,500 General, selling, and adm. costs $5,000,000 The budgeted production data for the three product lines follow. Product Lines Sets produced Value 15.000 $650 $80 30 Quality 5.000 $900 $50 Price Luxury 600 $1,200 $110 120 Direct materials cost per set Number of parts per set Direct labor hours per set Machine hours per set Production orders Production setups Orders shipped Number of inspections 15 200 70 50 50 2000 300 14 Required (Round all activity rates and unit costs to two decimal places) 1. Determine the cost per set and the total production cost of each of the three customer groups using activity-based costing. 2. Determine the production cost for each of the three customer groups using FFI's current volume-based approach. 3. Compare the two approaches and discuss the strategic and competitive issues of using each of the two methods. 4. The activity usage data given in the page 170 problem reflects current usage of the various cost drivers to manufacture the firm's product lines. Suppose you are given the following information regarding the firm's practical capacity for each of these activities, as follows: Number of parts 990,000 Number of production orders 800 Number of setups 200 Machine hours 100,000 Direct labor hours 123,900 Number of orders shipped 5,000 Compute the new activity rates using practical capacity and comment on how you would use this additional information for costing the firm's products and assisting in strategic planning. 4:33 Aa QD 5-40 Activity-Based Costing; Customer Group Cost Analysis Franklin Furniture Inc. (FFI) manufactures bedroom furniture in sets (a set includes a dresser, two queen-size beds, and one bedside table) for use in motels and hotels. FFI has three customer groups, which it calls the value, quality, and luxury groups. The value products are targeted to low-price motels that are looking for simple furniture, while the luxury furniture is targeted to the very best hotels. The value line is attractive to a variety of hotels and motels that appreciate the combination of quality and value. Currently there has been a small increase in the quality and value lines, and an appreciable increase in demand in the luxury line, reflecting cyclical changes in the marketplace. Luxury hotels are now in more demand for business travel, while a few years ago, the value segment was the most popular for business travelers. FFI wants to be able to respond to the increased demand with increased production but worries about the increased production cost and about price setting as its mix of customers and production change. FFI has used a volume-based overhead allocation rate based on direct labor hours for some time. Direct labor cost is $15 per hour. Budgeted Cost cost Driver Materials handling $ 349,600 Number of 169 Reader Contents Notebook Bookmarks More 0 W Budgeted Cost Cost Driver Materials handling $ 349,600 Number of parts Product scheduling Number of 160,000 production orders Setup labor 216,000 Number of setups Machine Automated machinery 1,750,000 hours Finishing Direct 619,500 labor hours Pack and ship Number of 290,400orders shipped $3,385,500 General, selling, and adm. costs $5,000,000 The budgeted production data for the three product lines follow. Product Lines Sets produced Value 15.000 $650 $80 30 Quality 5.000 $900 $50 Price Luxury 600 $1,200 $110 120 Direct materials cost per set Number of parts per set Direct labor hours per set Machine hours per set Production orders Production setups Orders shipped Number of inspections 15 200 70 50 50 2000 300 14 Required (Round all activity rates and unit costs to two decimal places) 1. Determine the cost per set and the total production cost of each of the three customer groups using activity-based costing. 2. Determine the production cost for each of the three customer groups using FFI's current volume-based approach. 3. Compare the two approaches and discuss the strategic and competitive issues of using each of the two methods. 4. The activity usage data given in the page 170 problem reflects current usage of the various cost drivers to manufacture the firm's product lines. Suppose you are given the following information regarding the firm's practical capacity for each of these activities, as follows: Number of parts 990,000 Number of production orders 800 Number of setups 200 Machine hours 100,000 Direct labor hours 123,900 Number of orders shipped 5,000 Compute the new activity rates using practical capacity and comment on how you would use this additional information for costing the firm's products and assisting in strategic planning