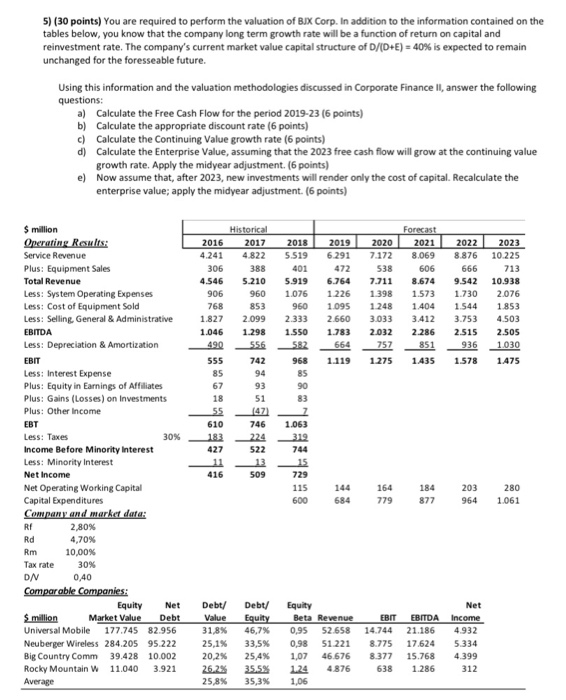

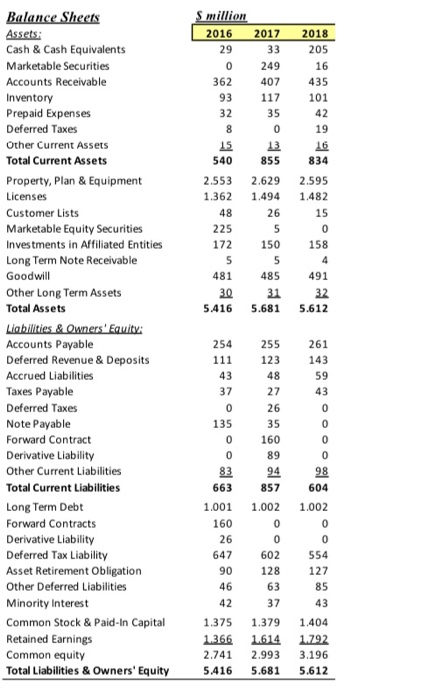

5) (30 points) You are required to perform the valuation of BJX Corp. In addition to the information contained on the tables below, you know that the company long term growth rate will be a function of return on capital and reinvestment rate. The company's current market value capital structure of D/(D+E) = 40% is expected to remain unchanged for the foresseable future. Using this information and the valuation methodologies discussed in Corporate Finance II, answer the following questions: a) Calculate the Free Cash Flow for the period 2019-23 (6 points) b) Calculate the appropriate discount rate (6 points) c) Calculate the Continuing Value growth rate (6 points) d) Calculate the Enterprise Value, assuming that the 2023 free cash flow will grow at the continuing value growth rate. Apply the midyear adjustment. (6 points) e) Now assume that, after 2023, new investments will render only the cost of capital. Recalculate the enterprise value; apply the midyear adjustment. (6 points) 2022 8.876 666 9.542 1.730 Forecast 2021 8.069 606 8.674 1.573 1.404 3.412 2.286 851 1.435 2019 6.291 472 6.764 1.226 1.095 2.660 1.783 664 1.119 2020 7.172 538 7.711 1.398 1.248 3.033 2032 757 1.275 Historical 2016 2017 2018 4.241 4.822 5.519 306 388 401 4.546 5.210 5.919 906 960 1.076 768 853 960 1.827 2.099 1.046 1.298 1.550 490 556 - 582 555 742 968 85 94 85 67 93 90 18 51 83 55 2 610 746 1.063 224 427 522 744 13 15 416 509 729 115 600 2023 10.225 713 10.938 2.076 1.853 4.503 2.505 1.030 1.475 2333 1.544 3.753 2.515 936 1.578 $ million Operating Results: Service Revenue Plus: Equipment Sales Total Revenue Less: System Operating Expenses Less: Cost of Equipment Sold Less: Selling General & Administrative EBITDA Less: Depreciation & Amortization EBIT Less: Interest Expense Plus: Equity in Earnings of Affiliates Plus: Gains (Losses) on Investments Plus: Other Income EBT Less: Taxes 30% Income Before Minority interest Less: Minority interest Net Income Net Operating Working Capital Capital Expenditures Company and market data: RE 2,80% Rd 4,70% Rm 10,00% Tax rate 30% DN 0,40 Comparable Companies: Equity Net Smillion Market Value Debt Universal Mobile 177.745 82.956 Neuberger Wireless 284.205 95.222 Big Country Comm 39.428 10.002 Rocky Mountain W 11.040 3.921 Average 1998 144 684 164 779 184 877 203 964 280 1.061 Debt/ Value 31,8% 25,1% 20,2% 26.2% 25,8% Debt/ Equity 46,7% 33,5% 25,4% 35,5% 35,3% Equity Beta Revenue 0,95 52.658 0,98 51.221 1,07 46.676 1.24 4876 1,06 EBIT 14.744 8.775 8.377 638 EBITDA 21.186 17.624 15.768 1.286 Net Income 4.932 5.334 4.399 312 S million 2016 2017 29 33 0 249 362 407 93 117 32 35 8 0 15 13 540 855 2.553 2.629 1.362 1.494 48 26 225 5 172 150 5 5 481 485 30 31 5.416 5.681 2018 205 16 435 101 42 19 16 834 2.595 1.482 15 0 158 4 491 32 5.612 Balance Sheets Assets: Cash & Cash Equivalents Marketable Securities Accounts Receivable Inventory Prepaid Expenses Deferred Taxes Other Current Assets Total Current Assets Property, Plan & Equipment Licenses Customer Lists Marketable Equity Securities Investments in Affiliated Entities Long Term Note Receivable Goodwill Other Long Term Assets Total Assets Liabilities & Owners' Equity Accounts Payable Deferred Revenue & Deposits Accrued Liabilities Taxes Payable Deferred Taxes Note Payable Forward Contract Derivative Liability Other Current Liabilities Total Current Liabilities Long Term Debt Forward Contracts Derivative Liability Deferred Tax Liability Asset Retirement Obligation Other Deferred Liabilities Minority Interest Common Stock & Paid-In Capital Retained Earnings Common equity Total Liabilities & Owners' Equity 254 255 111 123 43 48 37 27 0 26 135 35 0 160 0 89 83 94 857 1.0011.002 160 0 26 0 647 602 90 128 46 63 42 37 1.375 1.379 1.366 1.614 2.741 2.993 5.416 5.681 261 143 59 43 0 0 0 0 98 604 1.002 0 0 554 127 85 43 663 1.404 1.792 3.196 5.612 5) (30 points) You are required to perform the valuation of BJX Corp. In addition to the information contained on the tables below, you know that the company long term growth rate will be a function of return on capital and reinvestment rate. The company's current market value capital structure of D/(D+E) = 40% is expected to remain unchanged for the foresseable future. Using this information and the valuation methodologies discussed in Corporate Finance II, answer the following questions: a) Calculate the Free Cash Flow for the period 2019-23 (6 points) b) Calculate the appropriate discount rate (6 points) c) Calculate the Continuing Value growth rate (6 points) d) Calculate the Enterprise Value, assuming that the 2023 free cash flow will grow at the continuing value growth rate. Apply the midyear adjustment. (6 points) e) Now assume that, after 2023, new investments will render only the cost of capital. Recalculate the enterprise value; apply the midyear adjustment. (6 points) 2022 8.876 666 9.542 1.730 Forecast 2021 8.069 606 8.674 1.573 1.404 3.412 2.286 851 1.435 2019 6.291 472 6.764 1.226 1.095 2.660 1.783 664 1.119 2020 7.172 538 7.711 1.398 1.248 3.033 2032 757 1.275 Historical 2016 2017 2018 4.241 4.822 5.519 306 388 401 4.546 5.210 5.919 906 960 1.076 768 853 960 1.827 2.099 1.046 1.298 1.550 490 556 - 582 555 742 968 85 94 85 67 93 90 18 51 83 55 2 610 746 1.063 224 427 522 744 13 15 416 509 729 115 600 2023 10.225 713 10.938 2.076 1.853 4.503 2.505 1.030 1.475 2333 1.544 3.753 2.515 936 1.578 $ million Operating Results: Service Revenue Plus: Equipment Sales Total Revenue Less: System Operating Expenses Less: Cost of Equipment Sold Less: Selling General & Administrative EBITDA Less: Depreciation & Amortization EBIT Less: Interest Expense Plus: Equity in Earnings of Affiliates Plus: Gains (Losses) on Investments Plus: Other Income EBT Less: Taxes 30% Income Before Minority interest Less: Minority interest Net Income Net Operating Working Capital Capital Expenditures Company and market data: RE 2,80% Rd 4,70% Rm 10,00% Tax rate 30% DN 0,40 Comparable Companies: Equity Net Smillion Market Value Debt Universal Mobile 177.745 82.956 Neuberger Wireless 284.205 95.222 Big Country Comm 39.428 10.002 Rocky Mountain W 11.040 3.921 Average 1998 144 684 164 779 184 877 203 964 280 1.061 Debt/ Value 31,8% 25,1% 20,2% 26.2% 25,8% Debt/ Equity 46,7% 33,5% 25,4% 35,5% 35,3% Equity Beta Revenue 0,95 52.658 0,98 51.221 1,07 46.676 1.24 4876 1,06 EBIT 14.744 8.775 8.377 638 EBITDA 21.186 17.624 15.768 1.286 Net Income 4.932 5.334 4.399 312 S million 2016 2017 29 33 0 249 362 407 93 117 32 35 8 0 15 13 540 855 2.553 2.629 1.362 1.494 48 26 225 5 172 150 5 5 481 485 30 31 5.416 5.681 2018 205 16 435 101 42 19 16 834 2.595 1.482 15 0 158 4 491 32 5.612 Balance Sheets Assets: Cash & Cash Equivalents Marketable Securities Accounts Receivable Inventory Prepaid Expenses Deferred Taxes Other Current Assets Total Current Assets Property, Plan & Equipment Licenses Customer Lists Marketable Equity Securities Investments in Affiliated Entities Long Term Note Receivable Goodwill Other Long Term Assets Total Assets Liabilities & Owners' Equity Accounts Payable Deferred Revenue & Deposits Accrued Liabilities Taxes Payable Deferred Taxes Note Payable Forward Contract Derivative Liability Other Current Liabilities Total Current Liabilities Long Term Debt Forward Contracts Derivative Liability Deferred Tax Liability Asset Retirement Obligation Other Deferred Liabilities Minority Interest Common Stock & Paid-In Capital Retained Earnings Common equity Total Liabilities & Owners' Equity 254 255 111 123 43 48 37 27 0 26 135 35 0 160 0 89 83 94 857 1.0011.002 160 0 26 0 647 602 90 128 46 63 42 37 1.375 1.379 1.366 1.614 2.741 2.993 5.416 5.681 261 143 59 43 0 0 0 0 98 604 1.002 0 0 554 127 85 43 663 1.404 1.792 3.196 5.612