Answered step by step

Verified Expert Solution

Question

1 Approved Answer

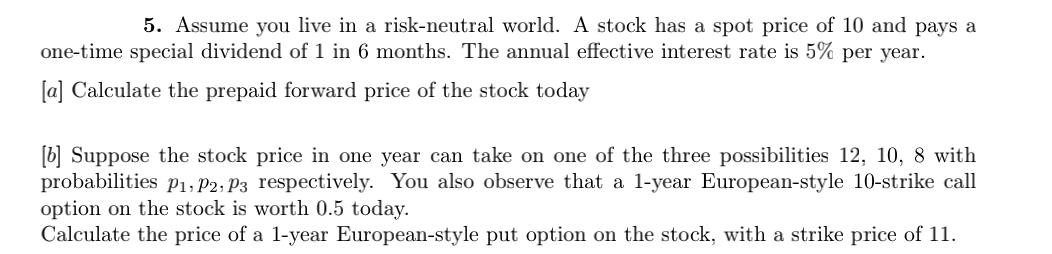

5. Assume you live in a risk-neutral world. A stock has a spot price of 10 and pays a one-time special dividend of 1

5. Assume you live in a risk-neutral world. A stock has a spot price of 10 and pays a one-time special dividend of 1 in 6 months. The annual effective interest rate is 5% per year. [a] Calculate the prepaid forward price of the stock today [b] Suppose the stock price in one year can take on one of the three possibilities 12, 10, 8 with probabilities P1, P2, P3 respectively. You also observe that a 1-year European-style 10-strike call option on the stock is worth 0.5 today. Calculate the price of a 1-year European-style put option on the stock, with a strike price of 11.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

a Prepaid forward price of the stock today Spot price ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Corporate Finance

Authors: Richard Brealey, Stewart Myers, Franklin Allen

12th edition

978-1259692178, 1259692175, 1259144380, 978-1259144387