Answered step by step

Verified Expert Solution

Question

1 Approved Answer

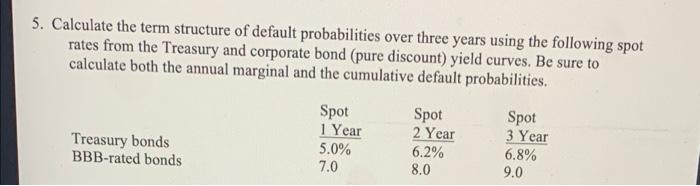

5. Calculate the term structure of default probabilities over three years using the following spot rates from the Treasury and corporate bond (pure discount) yield

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Terms Dictionary Investment Terminology Explained

Authors: Thomas Herold, Wesley Crowder

1st Edition

1521725764, 978-1521725764